Personal Loan vs Credit Card

Choosing between a personal loan and a credit card is not just a question of which option gives you money faster. It affects your monthly budget, total interest cost, credit score, repayment discipline, and financial stress. A personal loan usually gives you one lump sum with a fixed repayment schedule, while a credit card gives you flexible revolving access to credit that can be reused as you repay it.

This guide is written for beginners, borrowers comparing debt options, people planning a major expense, and anyone trying to decide whether to consolidate credit card debt with a personal loan. It explains how each option works, when each one makes sense, what costs to watch, and how to avoid expensive mistakes.

1. Personal Loan vs Credit Card: Simple Definition

A personal loan is usually an installment loan: you borrow a fixed amount, receive it as a lump sum, and repay it through scheduled monthly payments over a set term. A credit card is revolving credit: you can borrow up to a limit, repay some or all of the balance, and borrow again as long as the account remains open and in good standing.

In general, a personal loan is often better for a large planned expense or debt consolidation when you need structure and predictable payments. A credit card is often better for smaller purchases, short-term borrowing you can repay quickly, emergency flexibility, purchase protections, and rewards when you pay the balance in full.

| Best Choice | Usually Better When... | Be Careful Because... |

|---|---|---|

| Personal loan | You need a lump sum, fixed payment, fixed payoff date, or a disciplined debt consolidation plan. | You may pay origination fees, commit to a long term, and owe interest even if you no longer need the money. |

| Credit card | You need flexible access, can repay quickly, want convenience, or can benefit from a grace period and rewards. | Carrying a balance can become expensive, and minimum payments can keep you in debt longer. |

2. What Is a Personal Loan?

A personal loan is borrowed money that you repay in fixed installments. Most personal loans are unsecured, meaning you do not pledge collateral such as a car or home. Lenders usually review your credit history, income, existing debt, and ability to repay before approving the loan. The loan may be used for debt consolidation, medical bills, home repairs, moving costs, major purchases, or emergencies, depending on lender rules.

3. What Is a Credit Card?

A credit card is a revolving credit account. The card issuer gives you a credit limit. You can make purchases, cash advances, or balance transfers, then repay the balance later. If you pay the statement balance in full by the due date, purchases often avoid interest because of the grace period. If you carry a balance, interest is usually calculated on an ongoing basis, often daily.

Reader Advice: The Consumer Financial Protection Bureau explains that credit card interest is the cost of borrowing and that many issuers calculate it daily; paying sooner can reduce interest. The Federal Reserve publishes APR data for credit cards and personal loans under consumer credit reporting. The FTC provides consumer guidance on credit, loans, and debt management.

4. How Personal Loans Work

- You apply with a lender, bank, credit union, or online lending platform.

- The lender checks your credit, income, debt obligations, identity, and repayment capacity.

- If approved, you receive a fixed loan amount as a lump sum.

- You repay the loan through monthly installments over a set term, such as two to seven years depending on the lender and loan type.

- Each payment typically includes principal and interest; some loans also include fees such as origination fees.

- When the last payment is made, the loan is closed.

5. How Credit Cards Work

- You apply for a card and receive a credit limit if approved.

- You use the card for purchases up to the available limit.

- Each billing cycle, the issuer sends a statement showing your balance, minimum payment, payment due date, and interest terms.

- If you pay the statement balance in full by the due date, purchases may not accrue interest.

- If you pay less than the full statement balance, the remaining balance usually accrues interest.

- As you repay, available credit becomes usable again.

6. Personal Loan vs Credit Card: Full Comparison Table

| Feature | Personal Loan | Credit Card |

|---|---|---|

| Credit type | Installment loan | Revolving credit |

| How you receive funds | Usually one lump sum | Reusable credit line up to a limit |

| Best for | Large planned expenses, consolidation, predictable payoff | Smaller purchases, short-term borrowing, flexible spending |

| Repayment | Fixed monthly payments over a set term | Minimum payment required; full payoff optional each cycle |

| Interest rate | Often fixed, though variable options exist | Often variable; interest may be charged daily on carried balances |

| Grace period | Usually no purchase grace period because interest begins according to loan terms | Purchases may have a grace period if the statement balance is paid in full |

| Fees | Possible origination, late, returned payment, prepayment fees depending on lender | Possible annual fee, late fee, balance transfer fee, cash advance fee, foreign transaction fee |

| Credit score impact | Can diversify credit mix but adds a new loan and hard inquiry | Affects utilization strongly; high balances can hurt scores |

| Discipline level needed | Repayment structure helps force payoff | Requires discipline because you can keep reusing credit |

| Risk of long-term debt | Lower if payments are affordable and term is fixed | Higher if you carry balances and make only minimum payments |

7. Why the Choice Matters

The wrong borrowing tool can turn a manageable expense into a long-term debt problem. The right tool can lower total interest, improve cash flow, create a clear payoff plan, and protect your credit profile.

- Cost: The APR, fees, and repayment behavior determine how much borrowing really costs.

- Cash flow: A fixed loan payment may be easier to budget, while a credit card can fluctuate month to month.

- Debt behavior: Personal loans create a finish line. Credit cards offer flexibility but can encourage repeat borrowing.

- Credit score: Credit cards can affect credit utilization quickly; loans affect installment debt, payment history, and credit mix.

- Risk management: A personal loan can be safer for consolidation only if you stop adding new card debt.

8. Benefits of a Personal Loan

- Predictable monthly payments make budgeting easier.

- A fixed payoff date helps you know when the debt will end.

- A lump sum can cover a large one-time expense.

- Debt consolidation can simplify multiple payments into one.

- Some borrowers may qualify for a lower APR than their credit card APR, especially with strong credit and stable income.

9. Drawbacks of a Personal Loan

- You may pay an origination fee that reduces the amount you receive or increases the effective cost.

- You borrow the full amount upfront, even if you do not ultimately need all of it.

- Fixed payments can strain your budget if your income changes.

- A longer term may lower the monthly payment but increase total interest.

- Approval may be difficult with poor credit, unstable income, or high existing debt.

10. Benefits of a Credit Card

- Flexible borrowing for purchases as needed.

- Potential grace period on purchases when you pay the statement balance in full.

- Useful for emergencies when cash is temporarily short.

- Rewards, cash back, travel benefits, and purchase protections may add value when used responsibly.

- No interest on purchases if the full statement balance is paid on time and the account has a grace period.

11. Drawbacks of a Credit Card

- Carrying a balance can be expensive.

- Minimum payments can keep you in debt for a long time.

- High utilization can hurt your credit score.

- Late fees, penalty APRs, cash advance fees, and balance transfer fees can increase costs.

- The ability to reuse credit can make overspending easier.

12. Costs and Fees to Compare Before Borrowing

Do not compare only the monthly payment. Compare the APR, fees, repayment term, total interest, and what happens if you pay late or pay early.

| Cost or Fee | Personal Loan | Credit Card | What to Check |

|---|---|---|---|

| APR | Usually fixed, but lender terms vary | Often variable; may differ for purchases, transfers, and cash advances | Compare APRs using the same repayment timeline. |

| Origination fee | Common with some lenders | Not usually charged on purchases | Ask whether the fee is deducted from the loan proceeds. |

| Annual fee | Not typical | Common on some rewards cards | Rewards are only worthwhile if they exceed the fee and you avoid interest. |

| Late fee | Possible | Possible | Late payments can also hurt credit. |

| Balance transfer fee | Not applicable | Common for balance transfer offers | A 0% offer may still have an upfront transfer fee. |

| Cash advance fee | Not typical | Often charged, usually with no grace period | Avoid cash advances unless it is a true emergency. |

| Prepayment penalty | Uncommon but possible | Not applicable for normal card payments | Choose loans without prepayment penalties when possible. |

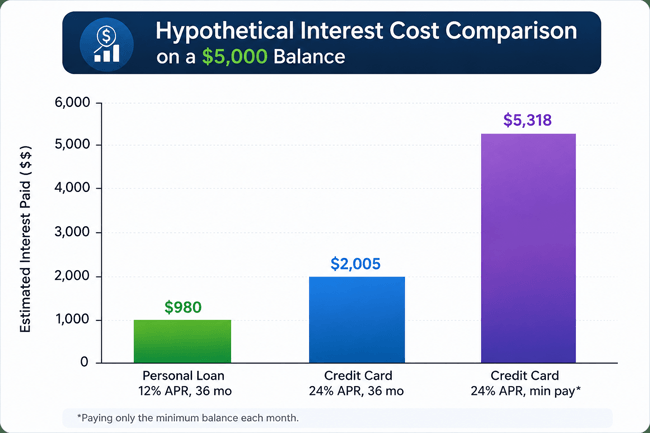

13. Example Cost Comparison Chart

The chart below uses a hypothetical $5,000 balance to show why repayment behavior matters. It is not a quote and should not be treated as a lender offer. Actual APRs, fees, and payment rules vary.

*Minimum-payment scenario is a simplified illustration. It assumes a prolonged payoff pattern and is included to show how slow repayment can raise total interest. Always use your issuer or lender disclosures for exact calculations.

14. Eligibility Requirements: What Lenders and Card Issuers Usually Review

Eligibility standards vary, but most lenders and card issuers want evidence that you can repay what you borrow. You may not need perfect credit, but better credit and stronger income often improve your options.

| Requirement | Personal Loan | Credit Card |

|---|---|---|

| Credit history | Important for approval and APR | Important for approval, limit, APR, and rewards tier |

| Income | Used to assess ability to repay | Used to assess ability to repay and assign a limit |

| Debt-to-income ratio | Often important | May be considered with other credit data |

| Employment or income stability | Often reviewed | May be reviewed |

| Identity and residency | Required | Required |

| Existing relationship | May help with banks/credit unions | May help with issuer offers |

15. Key Risks to Understand

15.1 Risk 1: Consolidating Debt but Creating New Debt

A personal loan can help pay off credit card balances, but it does not fix overspending by itself. If you pay off cards with a loan and then use the cards again, you may end up with both a loan payment and new card balances.

15.2 Risk 2: Focusing Only on Monthly Payment

A lower monthly payment can feel helpful, but a longer repayment period may increase total interest. Compare the full payoff cost, not only the monthly bill.

15.3 Risk 3: Using Credit Cards for Cash Advances

Credit card cash advances can be costly because they may include fees and may not receive the same grace period as purchases. They should generally be a last resort.

15.4 Risk 4: Missing Payments

Late or missed payments can lead to fees, higher borrowing costs, collection activity, and credit damage. Payment history is one of the most important parts of a credit profile.

16. When a Personal Loan May Be Better

- You have a large one-time expense and know the amount needed.

- You want fixed payments and a fixed payoff date.

- You can qualify for a lower APR than your credit card APR.

- You are consolidating high-interest card debt and have a plan to avoid new balances.

- You prefer structure because flexible credit makes overspending easier.

17. When a Credit Card May Be Better

- You can pay the statement balance in full by the due date.

- You need short-term convenience rather than long-term financing.

- The purchase is small or routine and fits your budget.

- You can use rewards or purchase protections without carrying debt.

- You qualify for a promotional 0% APR offer and have a realistic payoff plan before the promo period ends.

18. Step-by-Step Process: How to Decide Between a Personal Loan and a Credit Card

- Define the purpose. Is this a one-time expense, ongoing spending need, emergency, or debt consolidation?

- Calculate the amount. Borrow only what you need and can repay comfortably.

- Estimate repayment time. If you can repay within one billing cycle, a credit card may be cheaper. If repayment will take months or years, compare loan offers carefully.

- Compare APR and fees. Include origination fees, annual fees, balance transfer fees, late fees, and cash advance fees.

- Check monthly affordability. Make sure the payment fits your budget even if income or expenses change.

- Review credit impact. Consider hard inquiries, new accounts, utilization, and payment history.

- Read the disclosures. Look for APR, term, total payments, fees, grace period rules, and penalty terms.

- Choose the option with the lowest realistic total cost and lowest behavioral risk.

- Create a payoff plan before borrowing. Set autopay or reminders and decide what spending you will reduce.

- Track progress monthly. If the debt is not going down, adjust your budget quickly.

19. Real-World Examples

19.1 Example 1: Emergency Car Repair

Aisha needs $900 for a car repair. She gets paid in two weeks and can repay the full amount when her paycheck arrives. A credit card may be reasonable if she can pay the statement balance in full and avoid interest. A personal loan may be unnecessary because the amount is small and short term.

19.2 Example 2: Consolidating Credit Card Debt

Daniel owes balances on three credit cards and is making little progress because the payments feel scattered. He qualifies for a personal loan with a fixed payment and uses it to pay off the cards. This can work if he stops adding new card debt and the loan APR plus fees are lower than his current card costs. If he keeps using the cards, the strategy can backfire.

19.3 Example 3: Large Home Appliance Purchase

Maria needs a new refrigerator and cannot pay the full price this month. If a store credit card offers a 0% promotional period and she can repay before the promotion ends, the card may be cost-effective. If she needs a longer repayment period, a personal loan with fixed payments may be safer and more predictable.

19.4 Example 4: Vacation Spending

Omar wants to borrow for a vacation. Both a personal loan and a credit card can finance the trip, but borrowing for nonessential spending can create stress after the experience is over. A better option may be saving in advance, reducing the trip budget, or delaying the expense.

20. Alternatives to Personal Loans and Credit Cards

- Emergency savings: Cheapest option because there is no interest.

- Payment plan with a provider: Useful for medical, dental, or service bills if terms are fair and fees are low.

- 0% APR balance transfer card: May help with card debt if you qualify and repay before the promotional period ends.

- Credit union loan: May offer competitive terms and member-focused underwriting.

- Home equity loan or HELOC: May offer lower rates for homeowners, but your home can be at risk if the debt is secured by it.

- Borrowing from family or friends: Can reduce cost but should be documented clearly to protect the relationship.

- Budget adjustment or delayed purchase: Often the safest option for nonurgent expenses.

- Debt management plan through a reputable nonprofit credit counseling agency: May help if you are overwhelmed by unsecured debt.

21. Common Mistakes to Avoid

- Choosing the lowest monthly payment without checking total cost.

- Using a personal loan to pay off cards and then running up the cards again.

- Assuming rewards make a credit card worthwhile when you carry a balance.

- Ignoring fees such as origination fees, balance transfer fees, annual fees, and late fees.

- Taking a cash advance from a credit card without understanding the cost.

- Applying for too many loans or cards in a short time.

- Borrowing for wants when your budget is already under pressure.

- Skipping the fine print on promotional financing.

- Making only minimum payments without a payoff plan.

- Trusting “guaranteed approval” loan offers or paying upfront fees to questionable lenders.

22. Expert Tips for Choosing Wisely

- Use a personal loan when structure protects you from dragging out debt.

- Use a credit card only when you can repay quickly or when the card benefit clearly outweighs the cost.

- Compare total repayment cost, not just APR or monthly payment.

- Prequalify where available so you can compare estimated terms with less credit-score risk.

- For consolidation, close the behavior gap first: create a budget, pause card use, and set a payoff calendar.

- Build a small emergency fund alongside repayment so the next surprise expense does not go back on a card.

- Avoid borrowing the maximum amount offered. Approval does not mean the payment is comfortable.

- Read official disclosures and keep copies of your loan agreement or card terms.

23. Pros and Cons Summary

| Option | Pros | Cons |

|---|---|---|

| Personal loan | Fixed payment; fixed payoff date; useful for large expenses; can consolidate debt; may offer lower APR than cards for qualified borrowers. | May include fees; less flexible; interest starts according to loan terms; can encourage overborrowing; approval depends on credit and income. |

| Credit card | Flexible; convenient; possible grace period; rewards and protections; reusable credit line. | High cost if balance is carried; minimum payments can prolong debt; high utilization may hurt credit; fees can add up. |

24. Quick Action Checklist

- Write down the exact amount you need to borrow.

- Decide how many months you realistically need to repay it.

- Compare APR, fees, monthly payment, and total repayment cost.

- Check whether a credit card grace period or 0% APR offer applies.

- Check whether a personal loan has an origination fee or prepayment penalty.

- Make sure the monthly payment fits your budget.

- Avoid cash advances unless there is no safer option.

- Set autopay or payment reminders before the first due date.

- For debt consolidation, stop using the paid-off cards until your loan is under control.

- Keep emergency savings growing, even slowly.

25. Frequently Asked Questions About Personal Loans vs Credit Cards

25.1 Is a personal loan better than a credit card?

A personal loan is better when you need a fixed amount, predictable payments, and a clear payoff date. A credit card is better for short-term purchases you can repay in full or flexible spending you can manage responsibly.

25.2 Which is cheaper, a personal loan or a credit card?

The cheaper option depends on the APR, fees, repayment time, and your behavior. A credit card can be cheapest if you pay in full during the grace period. A personal loan may be cheaper for longer repayment if it has a lower APR and reasonable fees.

25.3 Should I use a personal loan to pay off credit card debt?

It can be smart if the loan lowers your total cost, gives you a fixed payoff plan, and you stop adding new card debt. It can be harmful if you pay off cards and then charge them up again.

25.4 Does a personal loan hurt your credit score?

A personal loan can cause a temporary dip because of a hard inquiry and new account. Over time, on-time payments may help your credit profile, while missed payments can hurt it.

25.5 Does a credit card hurt your credit score?

A credit card can help if you pay on time and keep balances low. It can hurt if you miss payments, carry high balances, or apply for too many cards.

25.6 Is it better to finance a large purchase with a credit card or personal loan?

For a large purchase you will repay over many months, compare a personal loan with any promotional card offer. A personal loan may be safer if you need fixed payments. A card may be better if you can repay within a 0% period or by the due date.

25.7 What is the main difference between a personal loan and a credit card?

A personal loan is a fixed installment debt. A credit card is revolving credit that can be reused as you repay it.

25.8 Can I get a personal loan with bad credit?

Possibly, but approval may be harder and costs may be higher. Compare lenders carefully, avoid upfront-fee scams, and consider credit unions or secured alternatives if appropriate.

25.9 Can I use a credit card instead of a loan?

Yes, for smaller or short-term expenses, especially if you can pay in full. For larger debts that need a long payoff period, a loan may provide more structure.

25.10 What is a balance transfer credit card?

A balance transfer card lets you move debt from another card, often with a promotional APR. It may charge a transfer fee, and the rate can increase after the promotional period.

25.11 Is a personal loan good for emergencies?

It can be useful for larger emergencies if you qualify quickly and can afford the payments. For smaller emergencies, savings or a card repaid quickly may cost less.

25.12 Should I close my credit card after paying it off with a personal loan?

Not always. Closing a card can reduce available credit and may affect utilization. A safer approach may be to keep it open but avoid using it until your budget is stable.

25.13 Why are minimum payments risky?

Minimum payments reduce immediate pressure but can extend repayment and increase total interest. Pay more than the minimum whenever possible.

25.14 Are personal loans secured or unsecured?

Many personal loans are unsecured, but some are secured by collateral. Secured loans may be easier to qualify for, but you risk losing the collateral if you default.

25.15 What should I compare before choosing?

Compare APR, fees, monthly payment, total repayment cost, repayment term, credit impact, and your own spending habits.

25.16 Sources Consulted

This article uses general consumer finance principles and aligns with guidance from authoritative consumer finance sources. Readers should always review current lender disclosures and local regulations before borrowing.

- Consumer Financial Protection Bureau (CFPB): consumer tools and explanations for credit cards, interest, repayment disclosures, and complaints.

- Federal Trade Commission (FTC): consumer guidance on credit, loans, debt, scams, and debt management.

- Federal Reserve Consumer Credit G.19: APR definitions and consumer credit interest-rate reporting for credit cards and personal loans.

- Official lender or card issuer disclosures: the final source for APR, fees, repayment terms, grace periods, promotional rules, and penalties.

26. Conclusion: Personal Loan or Credit Card?

A personal loan is usually the stronger choice when you need a fixed lump sum, a predictable monthly payment, and a clear end date. A credit card is usually the stronger choice when you need short-term flexibility, can pay in full, or can use a promotional offer responsibly.

The best decision is not simply the one with the lowest advertised APR. It is the option that gives you the lowest realistic total cost, the most manageable payment, and the lowest chance of falling deeper into debt. Before borrowing, compare costs, read the terms, check your budget, and create a payoff plan. Used carefully, both tools can be helpful. Used casually, either one can become expensive.

Practical next step: write down the amount, repayment timeline, and maximum monthly payment you can afford. Then compare a personal loan offer and a credit card repayment plan side by side before making a decision.

Reader Advice: This article is for general educational and informational purposes only and does not constitute individualized financial, legal, tax, accounting, or investment advice. Loan rates, APRs, fees, eligibility, underwriting standards, credit reporting practices, and applicable laws may vary by lender, loan type, borrower profile, location, and current regulations.

Always review the official loan agreement and disclosures, compare offers based on APR, fees, monthly payments, and total repayment cost, and verify current terms with the lender, loan servicer, StudentAid.gov, the SBA, or other relevant official sources when applicable.

If you need advice for your specific situation, especially involving debt disputes, lawsuits, foreclosure, wage garnishment, bankruptcy, or tax matters, consult a qualified financial professional, nonprofit credit counselor, tax adviser, accountant, consumer attorney, or legal aid organization.