Personal Loan Interest Rates Explained

Personal loan interest rates can feel confusing because lenders rarely show the full story in one simple number. You may see an advertised rate, a prequalified rate, an APR, an origination fee, a monthly payment, and a total repayment amount. Each number matters, but each answers a different question.

This topic matters because the interest rate on a personal loan directly affects how much you pay every month and how much the loan costs over time. A small rate difference can become a meaningful amount of money, especially on larger loans or longer repayment terms. For borrowers using a personal loan to consolidate debt, cover an emergency, pay medical bills, fund a home repair, or manage a major purchase, understanding the rate can prevent expensive mistakes.

This guide is written for beginners who want to borrow carefully. It explains what personal loan interest rates mean, how APR differs from the stated interest rate, why lenders offer different rates to different borrowers, how fees affect the true cost, and how to compare offers without being misled by a low payment or a tempting advertisement.

1. What Is a Personal Loan Interest Rate?

A personal loan interest rate is the price a lender charges you for borrowing money, expressed as a percentage of the loan balance. With most installment personal loans, interest is calculated on the remaining principal balance and paid through fixed monthly payments over a set term.

In plain English, the lender gives you money now, and you repay the original amount plus interest over time. The interest rate is one of the main ways the lender earns money and one of the biggest factors determining the cost of your loan.

For example, if you borrow $10,000 at a fixed interest rate, your monthly payment includes two parts: principal, which reduces the amount you borrowed, and interest, which pays the lender for extending credit. Early in the loan, more of each payment goes toward interest. Later, more goes toward principal.

1.1 Interest Rate vs APR: The Difference Beginners Must Understand

The interest rate is the cost of borrowing the principal. APR, or annual percentage rate, is broader. Under Regulation Z, the CFPB describes APR as a yearly measure of the cost of credit that relates the value received by the borrower to the payments made. In practice, APR is designed to help borrowers compare loan costs more fairly because it can include certain finance charges, not just the stated interest rate.

| Term | What It Means | Why It Matters |

|---|---|---|

| Interest rate | The percentage charged on the loan balance. | Helps estimate monthly interest cost, but may not include fees. |

| APR | The yearly cost of credit expressed as a rate, including certain finance charges. | Usually better for comparing loan offers. |

| Finance charge | The dollar cost of consumer credit, including charges imposed as a condition of credit. | Shows the actual cost in money, not just a percentage. |

| Monthly payment | The amount due each month. | Important for budgeting, but a low payment can hide a long expensive term. |

| Total repayment | All payments over the life of the loan. | Shows the full cost if you keep the loan to maturity. |

2. How Personal Loan Interest Rates Work

2.1 Most Personal Loans Use Simple Interest and Amortization

Many personal loans are installment loans with simple interest and amortization. This means interest is calculated on the outstanding balance, and the loan is repaid through scheduled payments. The payment is usually fixed when the loan has a fixed APR and fixed term.

Amortization simply means each payment is split between interest and principal. At the start, the balance is high, so interest takes a larger share of the payment. As the balance falls, the interest portion becomes smaller and the principal portion becomes larger.

2.2 The Basic Monthly Payment Formula

You do not need to memorize loan formulas to borrow wisely, but knowing the idea helps. A fixed-rate installment loan payment is based on the amount borrowed, the monthly interest rate, and the number of payments. The higher the APR or the longer the term, the more interest you usually pay overall.

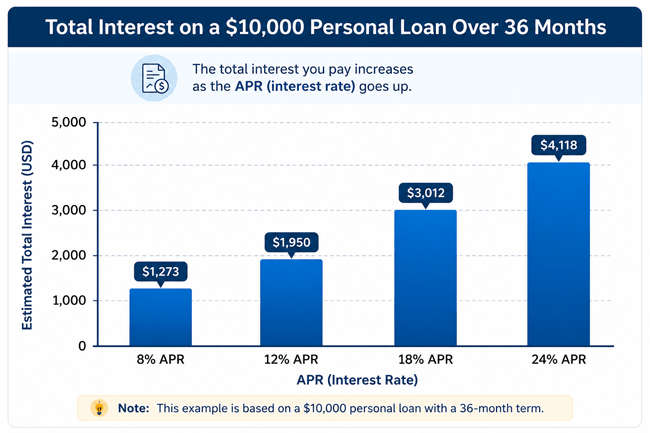

| Loan Amount | APR | Term | Estimated Monthly Payment | Estimated Total Interest |

|---|---|---|---|---|

| $10,000 | 8% | 36 months | $313 | $1,281 |

| $10,000 | 12% | 36 months | $332 | $1,957 |

| $10,000 | 18% | 36 months | $362 | $3,015 |

| $10,000 | 24% | 36 months | $392 | $4,114 |

These are simplified examples for education. Actual lender calculations can vary due to fees, payment timing, rounding, and state rules.

Chart takeaway: On the same $10,000 loan over the same 36-month term, a higher APR increases the total interest paid. The loan amount and term stay the same; the rate changes the cost.

3. What Affects Your Personal Loan Interest Rate?

Personal loan rates are risk-based. Lenders usually offer lower rates to applicants they believe are more likely to repay on time and higher rates to applicants who appear riskier. Different lenders use different underwriting models, so two lenders may quote different APRs for the same borrower.

3.1 Credit Score and Credit History

Your credit score is one of the biggest pricing factors. A stronger credit profile generally signals lower risk. Lenders may look at payment history, credit utilization, length of credit history, recent hard inquiries, delinquencies, collections, bankruptcies, and the mix of credit accounts.

3.2 Income and Employment Stability

Lenders want to know whether you have enough reliable income to repay the loan. Income does not guarantee a low rate, but stable income can support approval and may help you qualify for a better offer when combined with strong credit and manageable debt.

3.3 Debt-to-Income Ratio

Debt-to-income ratio compares your monthly debt obligations with your monthly income. A high ratio may suggest that a new loan payment could strain your budget. A lower ratio may help show that you can afford the loan.

3.4 Loan Amount and Loan Term

Larger loan amounts and longer terms can increase lender risk. A longer term may reduce the monthly payment, but it often increases total interest because you borrow for more months.

3.5 Secured vs Unsecured Loan

Most personal loans are unsecured, meaning they do not require collateral. Some lenders offer secured personal loans backed by a vehicle, savings account, certificate of deposit, or other asset. Secured loans may offer lower rates for some borrowers, but the risk is higher because you could lose the pledged asset if you default.

3.6 Market Interest Rates and Lender Funding Costs

Personal loan rates also move with broader credit conditions. The Federal Reserve reports personal loan rates as APRs under Regulation Z, and its G.19 release shows that commercial bank 24-month personal loan APRs have moved over time with changing market conditions. The rate you receive, however, still depends heavily on your individual profile and lender policies.

4. Why Personal Loan Interest Rates Matter

A personal loan rate affects more than the monthly payment. It affects affordability, total cost, debt payoff speed, and whether the loan actually improves your finances.

- Monthly budget impact: A higher rate usually means a higher payment for the same amount and term.

- Total borrowing cost: The APR helps you estimate how expensive the loan is over time.

- Debt consolidation results: A personal loan only helps if the new cost is meaningfully lower than the debt it replaces and you avoid adding new balances.

- Approval strategy: Understanding rate factors helps you decide whether to apply now, improve your profile first, add a co-borrower, or use an alternative.

- Risk control: Knowing the true cost helps prevent borrowing more than you can repay.

5. Benefits of Understanding Personal Loan Interest Rates

| Benefit | How It Helps You |

|---|---|

| Better comparison shopping | You can compare APR, fees, monthly payment, and total repayment instead of choosing the first offer. |

| Lower borrowing cost | Improving your credit, reducing debt, or shortening the term may help reduce the rate. |

| Smarter debt consolidation | You can calculate whether a consolidation loan actually saves money. |

| Fewer surprises | You can spot origination fees, late fees, prepayment rules, and optional add-ons. |

| More confidence | You understand what lenders are showing you and what questions to ask. |

6. Drawbacks and Limits of Personal Loan Interest Rates

Interest rates are useful, but they do not tell the entire story. A loan with the lowest advertised rate is not always the best loan for every borrower.

- Advertised rates may be reserved for highly qualified borrowers.

- Prequalification is not always a final approval or final APR.

- A lower monthly payment may come from a longer term, which can increase total interest.

- Fees can make a loan more expensive than the stated rate suggests.

- Some lenders use variable rates, which can make future payments less predictable.

- Borrowers with damaged credit may face high APRs that make the loan hard to justify.

7. Personal Loan Costs and Fees to Review

The interest rate is only one part of the cost. Before accepting a personal loan, review every fee and calculate how much money you will actually receive and repay.

| Cost or Fee | What It Means | Borrower Tip |

|---|---|---|

| Origination fee | A fee charged for processing or funding the loan. It may be deducted from loan proceeds or added to the cost. | Compare APR and net proceeds, not just the stated rate. |

| Late payment fee | A fee charged if you miss the due date or grace period. | Use autopay and calendar reminders. |

| Returned payment fee | A fee if your bank payment fails. | Keep enough money in the account before the due date. |

| Prepayment penalty | A fee for paying off the loan early. Less common on many personal loans, but still worth checking. | Avoid loans that punish early payoff unless the overall cost is still clearly better. |

| Optional insurance or add-ons | Products such as credit protection plans. | Do not buy unless you understand the cost, benefit, exclusions, and alternatives. |

| Application fee | Some lenders may charge application-related fees. | Be cautious if fees are required before approval or seem unusual. |

8. Fixed vs Variable Personal Loan Interest Rates

A fixed rate stays the same for the life of the loan, so the payment is predictable. A variable rate can change based on a benchmark or index, which means your payment and total cost may rise or fall.

| Feature | Fixed-Rate Personal Loan | Variable-Rate Personal Loan |

|---|---|---|

| Payment predictability | Usually high; payment stays the same. | Lower; payment can change. |

| Best for | Borrowers who want certainty and a clear payoff plan. | Borrowers comfortable with rate changes and potential payment increases. |

| Risk | May start higher than some variable offers. | Rate may rise, increasing cost. |

| Budgeting | Easier. | Requires more flexibility. |

| Beginner-friendly? | Usually yes. | Only if you fully understand the adjustment rules. |

9. Eligibility Requirements That Can Influence Your Rate

Eligibility requirements vary by lender, but most lenders evaluate several common factors. Meeting the minimum requirement may get you considered; exceeding the requirement may help you qualify for a better APR.

- Minimum credit score or acceptable credit profile.

- Verifiable income from employment, self-employment, benefits, retirement, or other eligible sources.

- Acceptable debt-to-income ratio.

- Valid identification and age of majority in your state or country.

- Bank account for funding and automatic payments.

- Credit history without severe recent negative events, depending on lender policy.

- Collateral, if applying for a secured personal loan.

10. Step-by-Step Process: How to Compare Personal Loan Rates

- Check your credit reports and correct errors before applying.

- Estimate how much you truly need to borrow. Avoid borrowing extra just because you qualify.

- Choose a realistic repayment term based on your budget and total interest cost.

- Prequalify with multiple lenders when possible. Prequalification often uses a soft credit check, but confirm before submitting.

- Compare APR, not just the interest rate or monthly payment.

- Review origination fees and calculate the net amount you will receive.

- Compare total repayment amount over the full term.

- Read late fee, autopay discount, prepayment, and default terms.

- Choose the lowest-cost loan you can comfortably repay, not simply the largest approved amount.

- After funding, make on-time payments and consider early payoff if there is no penalty and your emergency savings are adequate.

11. Real-World Examples

11.1 Example 1: Debt Consolidation

Maria has three credit cards with high balances and wants one predictable payment. She qualifies for a fixed-rate personal loan. Before accepting, she compares the APR against her current card APRs, checks the origination fee, and calculates whether the total repayment is lower. The loan helps only if she stops adding new card debt and uses the personal loan as part of a payoff plan.

11.2 Example 2: Emergency Home Repair

David needs $6,000 for an urgent plumbing repair. He compares a personal loan, a credit card, and a home equity option. The personal loan has a higher rate than a secured home equity product, but it funds faster and does not put his home at risk. He chooses a shorter term he can afford to reduce total interest.

11.3 Example 3: Fair Credit Borrower

Aisha has fair credit and receives several offers. One offer has a lower monthly payment, but the term is 60 months. Another has a slightly higher payment over 36 months and a lower total cost. She chooses the shorter loan after confirming the payment fits her budget.

12. How to Get a Lower Personal Loan Interest Rate

- Improve your credit before applying by paying bills on time and lowering revolving balances.

- Reduce your debt-to-income ratio by paying down existing debts or increasing reliable income.

- Compare banks, credit unions, and reputable online lenders.

- Use prequalification to shop without unnecessary hard inquiries, when available.

- Consider a co-borrower if the lender allows it and both people understand the shared responsibility.

- Choose a shorter term if the monthly payment is affordable.

- Set up autopay if the lender offers a legitimate rate discount.

- Avoid unnecessary add-ons that increase the effective cost.

- Borrow only what you need.

13. Personal Loan Alternatives

| Alternative | When It May Be Better | Main Risk |

|---|---|---|

| 0% balance transfer credit card | Short-term debt payoff when you can repay before the promo period ends. | High APR after the promotional period and possible transfer fee. |

| Home equity loan or HELOC | Large expenses for homeowners with equity. | Your home may be at risk if you cannot repay. |

| Credit union loan | Borrowers who want relationship-based underwriting or smaller loans. | Membership may be required. |

| Borrowing from savings | Small expenses when using savings will not create a bigger emergency. | Reduced emergency fund. |

| Payment plan with provider | Medical, dental, repair, or service bills. | Terms vary and may include fees. |

| Nonprofit credit counseling | Debt-management support for unsecured debts. | May not fit every debt type or urgency. |

| Family loan agreement | Trusted family support with written terms. | Relationship strain if repayment problems occur. |

14. Risks of Personal Loan Interest Rates

A personal loan can be useful, but it is still debt. The biggest risk is accepting a payment or APR that does not fit your real budget.

- High APR risk: A high-cost loan may worsen financial stress instead of solving it.

- Debt cycle risk: Consolidating credit cards and then using the cards again can leave you with more debt.

- Long-term cost risk: Longer terms can make payments feel affordable while increasing total interest.

- Default risk: Missed payments can lead to fees, credit damage, collections, or legal action depending on the agreement and law.

- Collateral risk: With secured loans, nonpayment can put the pledged asset at risk.

- Scam risk: Be cautious of lenders that guarantee approval, pressure you to act immediately, or demand unusual upfront payments.

15. Common Mistakes to Avoid

| Mistake | Why It Hurts | Better Approach |

|---|---|---|

| Comparing only monthly payments | Lower payments can hide longer terms and higher total interest. | Compare APR and total repayment. |

| Ignoring origination fees | You may receive less money than expected. | Calculate net proceeds after fees. |

| Assuming advertised rates apply to everyone | The best rates may require excellent credit and income. | Use prequalification and compare personalized offers. |

| Borrowing more than needed | Extra borrowing means extra interest. | Borrow only for the specific purpose. |

| Using consolidation without changing habits | Old balances can return while the new loan remains. | Close the spending leak and create a payoff plan. |

| Skipping the fine print | Late fees, autopay terms, and default clauses matter. | Read the loan agreement before signing. |

| Applying everywhere at once | Too many hard inquiries can hurt credit. | Use soft-check prequalification when possible. |

16. Expert Tips for Borrowers

- Treat APR as the starting point for comparison, not the only factor.

- Ask, “How much will I receive after fees?” and “How much will I repay in total?”

- For debt consolidation, compare the loan against your actual payoff timeline, not just the current card APR.

- Do not stretch the term just to make the payment look easy unless the extra total interest is worth it.

- Keep an emergency fund if possible, even while repaying debt, so you do not need another loan for the next unexpected expense.

- Check whether the lender reports payments to major credit bureaus. On-time payments can support credit building, while missed payments can damage it.

- Be skeptical of “no credit check” loans that carry very high costs or unclear terms.

17. Quick Action Checklist

- Know the exact loan purpose and amount needed.

- Check your credit reports and fix obvious errors.

- Estimate your affordable monthly payment before shopping.

- Compare at least three lenders when possible.

- Look at APR, origination fee, net proceeds, monthly payment, term, and total repayment.

- Avoid optional add-ons unless they clearly benefit you.

- Read the agreement before signing.

- Set up autopay or reminders before the first due date.

- Revisit your budget after funding so the payment stays manageable.

- Pay extra toward principal when allowed and financially safe.

18. Frequently Asked Questions

18.1 What is a personal loan interest rate?

A personal loan interest rate is the percentage a lender charges for borrowing money. It is applied to the loan balance and paid as part of your monthly payment.

18.2 What is APR on a personal loan?

APR is the annual cost of credit expressed as a percentage. It is often better than the stated interest rate for comparing loans because it may include certain fees and finance charges.

18.3 Is APR the same as the interest rate?

No. The interest rate reflects the cost of borrowing the principal. APR may include the interest rate plus certain loan costs, so it can be higher than the stated rate.

18.4 What is a good personal loan interest rate?

A good rate is one that is competitive for your credit profile, income, loan amount, term, and market conditions. Instead of relying on a single number, compare personalized APR offers from several reputable lenders.

18.5 Why is my personal loan interest rate so high?

Your rate may be high because of credit history, high debt-to-income ratio, unstable income, a longer term, an unsecured loan structure, or broader market conditions.

18.6 Can I negotiate a personal loan rate?

Sometimes. You may have more room with a bank or credit union where you have a relationship. Competing offers can help, but many online lenders use automated pricing models.

18.7 Does prequalification affect my credit score?

Prequalification often uses a soft credit check, which typically does not affect your score. Always confirm with the lender because a formal application may require a hard inquiry.

18.8 Do personal loans have fixed or variable rates?

Many personal loans have fixed rates, but some lenders offer variable-rate loans. Fixed rates are usually easier for beginners because the payment is predictable.

18.9 How do origination fees affect APR?

Origination fees can increase the APR and reduce the amount of money you receive. A loan with a lower interest rate but a high fee may cost more than it first appears.

18.10 Is it better to choose a shorter or longer term?

A shorter term usually costs less in total interest but has a higher monthly payment. A longer term may be easier monthly but can cost more overall.

18.11 Can paying off a personal loan early save interest?

Yes, paying early can reduce interest if the lender calculates interest on the remaining balance and does not charge a prepayment penalty. Check your agreement first.

18.12 Are personal loan rates lower than credit card rates?

They can be, especially for borrowers with strong credit. However, rates vary widely, so compare your actual APR offers against your current credit card APRs and payoff plan.

18.13 Can a secured personal loan get a lower rate?

Possibly. Collateral may reduce lender risk, but it also creates risk for you because the lender may be able to take the asset if you default.

18.14 Should I take a personal loan if the rate is high?

Only if the loan solves a necessary problem and the payment is affordable. For non-urgent borrowing, it may be better to improve your credit, reduce debt, or consider alternatives.

18.15 What documents do lenders need to set my rate?

Lenders may ask for identification, income proof, employment information, bank details, debt information, and permission to check credit. Requirements vary by lender.

19. Conclusion: Key Takeaways

Personal loan interest rates are not just technical numbers. They determine how much borrowing will cost, how manageable your monthly payment will be, and whether the loan helps or hurts your financial situation.

The most important best practice is to compare APR, fees, monthly payment, loan term, and total repayment together. Do not choose a loan only because the payment looks low or the advertisement mentions a low starting rate. Your actual offer depends on your credit, income, debt, loan amount, term, lender, and market conditions.

Used carefully, a personal loan can provide structure, predictable payments, and a clear payoff date. Used carelessly, it can become expensive debt. Take time to compare, read the terms, borrow only what you need, and choose a repayment plan that supports your financial stability.

19.1 Sources Consulted

Consumer Financial Protection Bureau, Regulation Z, 12 CFR 1026.22, “Determination of Annual Percentage Rate.” https://www.consumerfinance.gov/rules-policy/regulations/1026/22/

Consumer Financial Protection Bureau, Regulation Z, 12 CFR 1026.4, “Finance Charge.” https://www.consumerfinance.gov/rules-policy/regulations/1026/4/

Federal Reserve Board, Consumer Credit - G.19, current release. https://www.federalreserve.gov/releases/g19/current/default.htm

Federal Reserve Board, G.19 release notes, last update June 5, 2026. https://www.federalreserve.gov/releases/g19/

Reader Advice: This article is for general educational and informational purposes only and does not constitute individualized financial, legal, tax, accounting, or investment advice. Loan rates, APRs, fees, eligibility, underwriting standards, credit reporting practices, and applicable laws may vary by lender, loan type, borrower profile, location, and current regulations.

Always review the official loan agreement and disclosures, compare offers based on APR, fees, monthly payments, and total repayment cost, and verify current terms with the lender, loan servicer, StudentAid.gov, the SBA, or other relevant official sources when applicable.

If you need advice for your specific situation, especially involving debt disputes, lawsuits, foreclosure, wage garnishment, bankruptcy, or tax matters, consult a qualified financial professional, nonprofit credit counselor, tax adviser, accountant, consumer attorney, or legal aid organization.