How Much Personal Loan Can I Get?

When people ask, “How much personal loan can I get?” they are usually not asking only about a lender’s advertised maximum. They want to know what amount they may realistically qualify for, what monthly payment they can afford, and whether borrowing that amount is a wise financial decision.

This question matters because a personal loan can solve a short-term problem, such as consolidating high-interest debt, covering an urgent expense, or financing a necessary purchase. But the wrong loan amount can create years of pressure. Borrow too little and the loan may not solve the problem. Borrow too much and the monthly payment may strain your budget, increase your debt-to-income ratio, and make future borrowing harder.

This guide is written for beginners who want a practical, honest explanation before applying. You will learn how lenders estimate your loan amount, how income and credit affect approval, what costs reduce the money you actually receive, and how to decide the safest amount to borrow.

1. What Does “How Much Personal Loan Can I Get?” Mean?

The amount of personal loan you can get is the loan principal a lender is willing to approve based on your financial profile. It is not the same as the amount you want, the maximum amount advertised on a lender’s website, or the amount you can technically repay if you cut every other expense.

A personal loan is usually an installment loan. You receive a lump sum, repay it over a fixed term, and make scheduled monthly payments that include interest and sometimes fees. Most personal loans are unsecured, meaning they do not require collateral, although secured personal loans also exist.

| Term | Plain-English meaning |

|---|---|

| Loan principal | The amount you borrow before interest and fees. |

| APR | Annual percentage rate. It reflects the cost of borrowing, including interest and certain fees. |

| Term | The length of time you have to repay the loan. |

| Monthly payment | The amount due each month under the loan agreement. |

| Debt-to-income ratio | A comparison of your monthly debt payments to your monthly income. |

| Underwriting | The lender’s process for checking whether you can repay. |

2. Quick Answer: How Much Personal Loan Can You Get?

You may be able to get a personal loan amount that fits within the lender’s minimum and maximum limits and that your income, credit history, existing debts, employment stability, and repayment capacity can support. A strong borrower may qualify for a larger amount and better rate, while a borrower with lower income, high existing debt, unstable income, or weak credit may qualify for a smaller loan or may need a co-signer, collateral, or an alternative option.

3. How Lenders Decide Your Personal Loan Amount

Lenders do not approve personal loans by guessing. They look for evidence that you are likely to repay on time. The final amount is usually based on several factors working together.

3.1 Your Income and Repayment Capacity

Income is one of the first things lenders consider because it shows whether you have cash flow to make payments. Lenders may ask for pay slips, bank statements, tax returns, employment letters, or business income documents. Higher income can support a larger loan, but only if your other debts and living costs leave enough room for the new payment.

3.2 Your Debt-to-Income Ratio

Debt-to-income ratio, often called DTI, compares your monthly debt payments with your monthly income. A lower DTI generally suggests more room for a new loan payment. A high DTI may limit the amount you can borrow even if your income looks good on paper.

| DTI situation | What it may signal to a lender | Possible effect on loan amount |

|---|---|---|

| Low existing debt | You may have more room for a new payment. | Higher potential approval amount, depending on credit and income. |

| Moderate existing debt | You may still qualify, but the lender may be cautious. | Moderate loan amount or stricter terms. |

| High existing debt | Your budget may already be stretched. | Lower amount, higher rate, or possible denial. |

3.3 Your Credit Score and Credit History

Your credit score helps lenders estimate the likelihood that you will repay. The Consumer Financial Protection Bureau explains that a credit score is a prediction of credit behavior based on information in your credit reports. Lenders may use it to decide whether to offer credit and what terms to offer.

Credit history matters too. A person with a long record of on-time payments may qualify for a larger amount than someone with recent missed payments, defaults, collections, or very limited credit history.

3.4 Your Employment or Business Stability

Stable employment or consistent business income can improve confidence in your ability to repay. If your income is irregular, seasonal, commission-based, or self-employed, you may still qualify, but the lender may ask for more documents or approve a smaller amount.

3.5 The Loan Purpose

Some lenders ask why you need the loan. Debt consolidation, medical expenses, home repairs, education-related costs, or major purchases may be treated differently depending on the lender. The purpose may also affect whether the lender has restrictions on how funds can be used.

3.6 Lender Minimums, Maximums, and Policies

Every lender sets its own minimum and maximum personal loan amounts. Some lenders specialize in small loans; others offer larger loans to well-qualified borrowers. Your approved amount cannot exceed the lender’s product limits even if your income is high.

4. A Simple Way to Estimate How Much Personal Loan You Can Afford

A safe borrowing estimate starts with your budget, not the lender’s advertisement. Use this practical process:

- Write down your stable monthly take-home income.

- List all required monthly expenses, including rent, utilities, food, transport, insurance, minimum debt payments, and essential family obligations.

- Subtract those expenses from your income to see your monthly breathing room.

- Decide how much of that breathing room can safely go toward a loan payment without eliminating savings or emergency cash.

- Use that safe payment amount to estimate a loan amount based on the APR and repayment term.

A useful rule of thumb is to avoid taking the largest payment you can barely manage. A loan should fit your real life, including unexpected expenses, income delays, family needs, and emergencies.

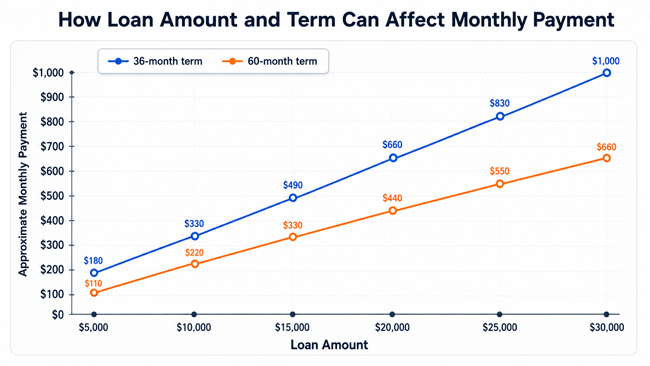

The chart below shows how the same loan amount can produce different monthly payments depending on the repayment term. It uses approximate payments at a 12% APR for illustration only. Actual payments depend on your lender, APR, fees, term, and payment schedule.

Chart note: A longer term usually lowers the monthly payment but can increase total interest paid over the life of the loan.

5. Real-World Examples: How Loan Amounts Can Change by Borrower

5.1 Example 1: Salaried borrower with manageable debt

Aisha earns a stable salary and already has a small car payment. She wants a personal loan for home repairs. Her lender reviews her income, bank statements, credit history, and existing debt. Because her debt load is manageable and her payment history is strong, she may qualify for a larger amount than someone with the same income but more debt.

Decision lesson: A lender does not look at income alone. Existing debt and payment history can strongly affect the approved amount.

5.2 Example 2: High income but high existing debt

Bilal earns more than many applicants, but he already has multiple credit card balances and a car loan. His income is high, but his monthly obligations are also high. A lender may approve only a smaller personal loan because the new payment would add pressure to his budget.

Decision lesson: High income does not automatically mean a high personal loan approval.

5.3 Example 3: Self-employed borrower with irregular income

Sara is self-employed and has good annual income, but her earnings fluctuate by month. The lender may ask for tax returns, bank statements, invoices, or business records. If the income looks consistent over time, she may qualify. If the income is unpredictable, the lender may approve a smaller amount or charge a higher rate.

Decision lesson: Documentation and consistency matter for self-employed borrowers.

6. Personal Loan Amount vs Monthly Payment: Example Table

The following table is for education only. It assumes an approximate 12% APR and does not include origination fees, late fees, optional insurance, or other costs.

| Loan amount | Approx. payment over 36 months | Approx. payment over 60 months | What to consider |

|---|---|---|---|

| $5,000 | $166 | $111 | Useful for a smaller urgent expense; still check fees. |

| $10,000 | $333 | $222 | Common for debt consolidation or repairs; compare total interest. |

| $20,000 | $665 | $445 | Requires stronger repayment capacity; avoid stretching the budget. |

| $30,000 | $998 | $667 | Large commitment; only consider if income is stable and purpose is important. |

7. Why Your Personal Loan Amount Matters

The amount you borrow affects your monthly payment, total interest, approval odds, credit profile, and financial flexibility. A personal loan can be helpful, but it is still debt. The goal is not to borrow the highest amount possible; the goal is to borrow the right amount for a clear purpose at a cost you can handle.

- A larger loan can solve a bigger problem but usually creates a larger payment.

- A longer term may reduce the monthly payment but can increase total interest.

- A smaller loan may be easier to approve and repay but may not fully cover the need.

- A loan that consolidates debt can help only if you avoid building new debt afterward.

- Missed payments can damage credit and lead to fees, collection activity, or legal consequences depending on local rules.

8. Common Personal Loan Eligibility Requirements

Eligibility rules vary by lender and country, but most personal loan applications involve similar checks.

| Requirement | Why lenders check it | Documents or evidence |

|---|---|---|

| Age and legal capacity | The borrower must legally enter a loan agreement. | Government ID or national identity document. |

| Income | Shows ability to repay. | Pay slips, bank statements, tax returns, pension statements, or business records. |

| Employment or business history | Shows income stability. | Employment letter, contract, business registration, invoices, or tax filings. |

| Credit history | Shows past borrowing behavior. | Credit report and credit score where available. |

| Existing debt | Shows current obligations. | Credit report, bank statements, loan statements, credit card statements. |

| Bank account | Used for disbursement and payments. | Bank statement or account details. |

| Residence information | Helps verify identity and stability. | Utility bill, lease, or address record if required. |

9. Benefits of Getting the Right Personal Loan Amount

- Predictable repayment: Fixed installment loans make budgeting easier because the monthly payment is known in advance.

- Debt consolidation potential: A personal loan may simplify multiple payments into one payment if the new loan has better terms.

- No collateral in many cases: Unsecured personal loans usually do not require pledging a home, vehicle, or savings account.

- Flexible use: Many personal loans can be used for practical needs such as repairs, emergencies, or planned expenses.

- Possible credit-building benefit: On-time payments may support a healthier credit profile over time.

10. Drawbacks of Borrowing Too Much

- Higher monthly payments can strain your budget.

- Longer repayment terms can increase total interest.

- Fees may reduce the amount of cash you actually receive.

- A new loan increases your total debt and may affect future borrowing.

- Missed payments can create credit, legal, and collection problems.

- Borrowing for nonessential spending can delay savings goals.

11. Costs and Fees That Affect How Much You Should Borrow

The approved loan amount is not the only number that matters. The total cost of the loan determines whether the loan is affordable.

| Cost or fee | What it means | Why it matters |

|---|---|---|

| Interest | The cost charged for borrowing money. | Higher interest increases monthly and total cost. |

| APR | A broader annual cost measure that includes interest and certain fees. | Useful for comparing offers more fairly. |

| Origination or processing fee | A fee charged to create or process the loan. | May be deducted from the loan amount or added to cost. |

| Late payment fee | Fee charged when payment is missed or late. | Can make a difficult situation worse. |

| Prepayment fee | Fee for paying early, if charged. | Can reduce the benefit of early payoff. |

| Optional insurance or add-ons | Products such as payment protection, where offered. | May increase cost and should be carefully reviewed. |

The U.S. Truth in Lending framework requires disclosure of key credit costs such as finance charges and APR in many consumer credit agreements. Even outside the U.S., the principle is useful: compare loans by total cost, not just monthly payment.

12. Step-by-Step Process: How to Find Out How Much Personal Loan You Can Get

- Define the exact purpose of the loan. Borrow for a real need, not just because approval is available.

- Calculate the amount you actually need. Include necessary costs but avoid padding the loan for unnecessary spending.

- Check your monthly budget. Identify a payment you can afford while still saving something for emergencies.

- Review your existing debts. If your current debt load is high, consider reducing debt before applying.

- Check your credit report where available. Correct errors and understand how lenders may view your profile.

- Estimate payments using several loan amounts and terms. Compare both monthly payment and total interest.

- Prequalify with multiple lenders if available. Prequalification can help estimate offers, though final approval may change after verification.

- Compare APR, fees, term, total repayment, payment date, and penalties.

- Choose the smallest loan that solves the problem safely.

- Read the agreement before signing. Make sure the payment, APR, fees, due date, and repayment term match what you understood.

13. Common Mistakes to Avoid

| Mistake | Why it hurts | Better choice |

|---|---|---|

| Applying for the maximum advertised amount | Advertised maximums are not personalized and may tempt overborrowing. | Estimate your safe payment first. |

| Focusing only on monthly payment | A low payment can hide a long term and higher total interest. | Compare total repayment cost. |

| Ignoring fees | Fees can reduce cash received or increase total cost. | Review APR and fee schedule. |

| Borrowing to cover lifestyle spending | Debt can become a habit instead of a solution. | Use loans for clear, necessary purposes. |

| Consolidating debt and then using credit cards again | This can double your debt burden. | Close the spending leak before consolidating. |

| Skipping lender verification | Scams often promise guaranteed approval or demand upfront payment. | Verify licensing, contact details, and disclosures. |

| Missing the first payment | Early missed payments can quickly harm your credit and trigger fees. | Set reminders or automatic payments if safe. |

14. Risks and Warning Signs

Personal loans can be useful, but they also carry risks. Be especially careful when you feel urgent pressure to borrow.

- Overborrowing risk: A loan that looks manageable today may become difficult if income drops or expenses rise.

- Interest-rate risk: Borrowers with weaker credit may receive higher rates under risk-based pricing.

- Fee risk: Processing, origination, late, or add-on fees can increase cost.

- Credit risk: Late or missed payments may hurt your credit profile.

- Scam risk: The Federal Trade Commission warns consumers about advance-fee loan scams, especially offers that promise approval after an upfront payment.

14.1 Red Flags of a Personal Loan Scam

- The lender guarantees approval before reviewing your application.

- You are told to pay an upfront fee before receiving the loan.

- The offer arrives unexpectedly by call, message, or email and creates pressure to act immediately.

- The lender avoids clear disclosure of APR, fees, repayment term, or company details.

- You are asked to pay by gift card, wire transfer, cryptocurrency, or another unusual method.

- The website looks insecure, copied, or difficult to verify.

15. Alternatives If You Cannot Qualify for Enough Personal Loan

| Alternative | Best for | Main caution |

|---|---|---|

| Save and delay the purchase | Non-urgent expenses. | May not work for emergencies. |

| Negotiate bills or payment plans | Medical bills, utilities, school fees, or service balances. | Get the agreement in writing. |

| Debt management plan through a reputable nonprofit counselor | Credit card debt that feels unmanageable. | Avoid high-fee debt settlement promises. |

| Secured loan | Borrowers who have acceptable collateral and need a larger amount. | You can lose the collateral if you default. |

| Co-signer or joint borrower | Borrowers with limited credit or income. | The other person becomes responsible if you do not pay. |

| Credit union or community lender | Borrowers seeking smaller, potentially lower-cost loans. | Membership or eligibility may be required. |

| Employer salary advance or hardship program | Short-term emergency cash need. | May reduce future paycheck or require employer approval. |

| Family loan with written terms | Trusted family support. | Can damage relationships if unclear or unpaid. |

16. Borrowing More vs Borrowing Less: Comparison

| Choice | Potential advantage | Potential downside | Best used when |

|---|---|---|---|

| Borrowing more | May fully solve the financial need at once. | Higher payment and more total interest. | The need is important, documented, and affordable. |

| Borrowing less | Lower payment and easier repayment. | May not fully solve the problem. | You can combine with savings, negotiation, or phased spending. |

| Longer term | Lower monthly payment. | More months of debt and possibly more interest. | Cash flow is tight but total cost is still acceptable. |

| Shorter term | Less time in debt and often less total interest. | Higher monthly payment. | You have strong, stable cash flow. |

17. Expert Tips for Choosing the Right Personal Loan Amount

- Start with the payment you can safely afford, then work backward to the loan amount.

- Compare at least a few offers when possible because APR, fees, and terms vary by lender.

- Do not treat prequalification as guaranteed approval. Final approval usually requires verification.

- Keep emergency savings separate from loan payments. A loan should not consume every spare dollar.

- For debt consolidation, stop using the paid-off credit cards until your budget is stable.

- Avoid borrowing for a depreciating or nonessential purchase unless you have a clear repayment plan.

- Read the loan agreement slowly. Check payment amount, due date, APR, fees, late policy, and prepayment terms.

- Use the smallest loan that solves the problem, not the largest amount offered.

18. Quick Action Checklist

- Write down the exact reason you need the loan.

- Calculate the minimum amount needed to solve the problem.

- Check your monthly income and essential expenses.

- Estimate a safe monthly loan payment.

- Review current debts and credit obligations.

- Check your credit report or credit profile where available.

- Estimate payments for different terms and APRs.

- Compare APR, fees, loan term, total repayment, and lender reputation.

- Watch for guaranteed approval and upfront-fee scams.

- Borrow only after you understand the full repayment commitment.

19. Frequently Asked Questions

19.1 How much personal loan can I get based on my salary?

It depends on your take-home income, existing debts, credit profile, repayment term, lender limits, and documentation. Salary helps, but lenders also check whether the new monthly payment fits your budget.

19.2 What is the maximum personal loan I can get?

The maximum depends on the lender’s product limit and your eligibility. Even if a lender advertises a high maximum, your approved amount may be lower after underwriting.

19.3 Can I get a personal loan with low income?

Possibly, but the amount may be smaller. A lender will want to see that you can repay the loan after essential expenses and existing debt payments.

19.4 Does my credit score affect how much personal loan I can get?

Yes. Credit score and credit history can affect approval, loan amount, APR, and fees. A stronger credit profile can improve your chances of receiving better terms.

19.5 Can I get a personal loan without a credit history?

It may be harder, but not always impossible. Some lenders may consider income, bank history, employment, collateral, or a co-signer. The approved amount may be limited.

19.6 Should I borrow the maximum amount offered?

Usually no. Borrow the amount that solves your need while keeping the payment affordable. The maximum offer may be more than your budget should handle.

19.7 How do lenders calculate personal loan eligibility?

Lenders commonly review income, employment, credit history, existing debt, payment behavior, bank activity, identity documents, and the requested loan amount.

19.8 Will a longer term help me qualify for more?

A longer term can reduce monthly payment, which may help affordability. However, it may also increase total interest, so compare the full cost before choosing.

19.9 Can I increase my personal loan amount after approval?

Some lenders allow you to request a higher amount before signing or apply for another loan later. Approval is not guaranteed and may require another review.

19.10 What if I need more than lenders will approve?

Consider reducing the amount, improving your credit, paying down existing debt, adding a qualified co-signer, using collateral, negotiating bills, or exploring nonprofit credit counseling.

19.11 Do personal loan fees reduce how much money I receive?

They can. Some origination or processing fees may be deducted from the loan proceeds, meaning you receive less cash than the approved principal.

19.12 Is a personal loan better than a credit card?

It depends. A personal loan may offer fixed payments and a clear payoff date. A credit card may be more flexible but can become expensive if you carry a balance.

19.13 Can I use a personal loan for debt consolidation?

Yes, many borrowers use personal loans to consolidate debt. It works best when the new loan lowers cost or simplifies repayment and you avoid taking on new debt.

19.14 What is the safest personal loan amount?

The safest amount is the smallest amount that meets a real need and creates a monthly payment you can afford even if your budget faces minor surprises.

19.15 Can applying for a personal loan affect my credit?

It can. A formal application may involve a hard credit inquiry where credit reporting systems are used. On-time repayment may help over time, while missed payments can hurt.

19.16 Sources Consulted

Consumer Financial Protection Bureau (CFPB): credit scores, risk-based pricing, and consumer credit education. Website: consumerfinance.gov

Federal Trade Commission (FTC): advance-fee loan scam warnings and consumer fraud reporting. Website: consumer.ftc.gov

State Bank of Pakistan prudential regulations for consumer financing: personal financing definitions and consumer finance principles. Website: sbp.org.pk

20. Conclusion: The Best Loan Amount Is the One You Can Repay Comfortably

The real answer to “How much personal loan can I get?” is not just a number. It is a decision based on eligibility, affordability, purpose, cost, and risk. A lender may tell you the amount you can be approved for, but only your budget can tell you whether that amount is safe.

Before applying, calculate the amount you truly need, estimate a comfortable monthly payment, compare APR and fees, and avoid lenders that pressure you or promise guaranteed approval for upfront payment. A personal loan can be a useful financial tool when it solves a real problem and fits your repayment capacity. The smartest borrowers do not chase the largest loan; they choose the loan that protects their future cash flow.

Reader Advice: Loan eligibility, maximum amounts, rates, fees, disclosures, and consumer protections vary by country, lender, and borrower profile. Readers should check local regulations and lender documents before signing any loan agreement.