Fixed vs Variable Interest Rate Personal Loans

Choosing between a fixed and variable interest rate personal loan can affect your monthly payment, total borrowing cost, and financial stress level for the entire life of the loan. Many borrowers focus only on the advertised interest rate, but the type of rate matters just as much. A fixed rate gives predictable payments. A variable rate may start lower, but it can change over time.

This decision matters because personal loans are often used during important financial moments: consolidating credit card debt, paying medical bills, covering emergency expenses, financing home repairs, or managing a large one-time purchase. When money is already tight, an unexpected payment increase can create real pressure. On the other hand, paying more for predictability may not always be necessary if the loan is short, affordable, and clearly understood.

This guide is written for beginners who want a plain-English explanation before they borrow. It explains how fixed and variable rates work, what lenders look at, what fees may apply, what risks to watch for, and how to compare offers responsibly. The goal is not to tell every borrower to choose the same option, but to help you choose the rate structure that fits your budget, risk tolerance, and repayment plan.

1. Fixed vs Variable Personal Loans: Concise Definition

| Rate Type | Plain-English Meaning | Best Known For |

|---|---|---|

| Fixed-rate personal loan | The interest rate stays the same for the full loan term, so the scheduled monthly payment usually stays the same. | Predictability and easier budgeting. |

| Variable-rate personal loan | The interest rate can rise or fall based on a benchmark rate or lender formula, so the monthly payment or total interest cost may change. | Potential savings if rates fall, but higher payment risk if rates rise. |

2. What Is a Fixed-Rate Personal Loan?

A fixed-rate personal loan is an installment loan with an interest rate that does not change during the repayment term. If you borrow a set amount for a set number of months, your payment schedule is usually established at the start and remains consistent until the loan is paid off, assuming you pay on time and do not modify the loan.

For example, if you take a three-year fixed-rate personal loan, the lender calculates your monthly payment using the loan amount, interest rate, and repayment term. The payment is designed to fully repay the loan by the end of the term. Your first payment and your last scheduled payment are generally the same amount.

2.1 How Fixed-Rate Personal Loans Work

The lender offers an interest rate based on factors such as your credit score, income, debt-to-income ratio, loan amount, loan term, and overall risk profile. Once you accept the offer and sign the agreement, the rate is locked for that loan.

Each payment usually includes both principal and interest. Early payments often include more interest because the outstanding balance is larger. Later payments usually include more principal as the balance declines. This repayment pattern is called amortization.

2.2 Benefits of Fixed-Rate Personal Loans

- Predictable monthly payments make budgeting easier.

- Protection from rising interest rates during the loan term.

- Easier comparison between loan offers because the payment schedule is stable.

- Helpful for borrowers with fixed income or limited room in their monthly budget.

- Useful for debt consolidation when the goal is a clear payoff date.

2.3 Drawbacks of Fixed-Rate Personal Loans

- The starting rate may be higher than a variable-rate offer from the same lender.

- You may not benefit automatically if market rates fall.

- Refinancing to get a lower rate may involve a new application, credit check, and possible fees.

- A fixed payment can still be unaffordable if the borrower chooses too large a loan or too short a term.

3. What Is a Variable-Rate Personal Loan?

A variable-rate personal loan is an installment loan with an interest rate that can change during the repayment term. The rate is usually tied to a benchmark or index plus a lender margin. When the benchmark changes, your loan rate may change according to the loan agreement.

Variable-rate personal loans are less common than fixed-rate personal loans in some markets, but they exist. They may be offered by banks, credit unions, online lenders, or specialized lenders. The key point is that the advertised starting rate is not necessarily the rate you will pay for the entire loan.

3.1 How Variable-Rate Personal Loans Work

A variable rate is often expressed as an index plus a margin. The index is a benchmark rate that moves with broader financial conditions. The margin is the lender’s added percentage based on its pricing model and your risk profile.

For example, a loan could be priced as a benchmark rate plus a lender margin. If the benchmark rises, the loan rate may rise. If the benchmark falls, the loan rate may fall. The agreement should explain how often the rate can adjust, whether there is a minimum or maximum rate, and how payment changes are handled.

Some variable loans change the monthly payment when the rate changes. Others keep the payment more stable but adjust how quickly the loan pays down. Borrowers should read the agreement carefully because these details affect risk.

3.2 Benefits of Variable-Rate Personal Loans

- The starting interest rate may be lower than a comparable fixed-rate loan.

- Borrowers may benefit if benchmark rates fall.

- A short-term borrower may pay less interest if rates do not rise much before payoff.

- It may be useful for borrowers who plan to repay early and can handle payment changes.

3.3 Drawbacks of Variable-Rate Personal Loans

- Monthly payments may increase if rates rise.

- Total interest cost is harder to predict.

- Budgeting is more difficult because future payments are uncertain.

- A low starting rate can make the loan look cheaper than it may actually become.

- Borrowers may misunderstand adjustment rules, rate caps, or payment recalculation.

4. Fixed vs Variable Interest Rate Personal Loans: Side-by-Side Comparison

| Feature | Fixed-Rate Personal Loan | Variable-Rate Personal Loan |

|---|---|---|

| Interest rate | Stays the same for the loan term. | Can increase or decrease based on the loan agreement. |

| Monthly payment | Usually predictable and consistent. | May change when the rate adjusts. |

| Budgeting | Easier for beginners and households with tight cash flow. | Requires more flexibility and planning. |

| Starting rate | May be slightly higher than variable. | May start lower, but not always. |

| Risk level | Lower payment uncertainty. | Higher payment and total-cost uncertainty. |

| Best for | Borrowers who value stability and a clear payoff plan. | Borrowers who can handle rate changes or plan fast repayment. |

| Main warning | Do not overborrow simply because the payment is predictable. | Do not rely only on the introductory or starting rate. |

5. Why the Rate Type Matters

The difference between fixed and variable rates is not just technical. It affects three practical questions: Can you afford the payment every month? Can you predict the total cost? Can you stay on track if your income or expenses change?

A personal loan is usually unsecured, meaning there may be no collateral, but missing payments can still damage credit, trigger fees, lead to collections, and make future borrowing more expensive. Choosing the wrong rate type can turn a manageable loan into a financial burden.

| Borrower Concern | Why Rate Type Matters |

|---|---|

| Monthly budget | Fixed rates help you know the payment in advance. Variable rates require a cushion for increases. |

| Debt consolidation | Fixed rates make it easier to compare the new loan payment with current debt payments. |

| Emergency borrowing | Predictability may be more important when the borrower is already under stress. |

| Short repayment plans | Variable rates may be less risky if the loan will be paid off quickly, but only if early repayment is allowed. |

| Longer loan terms | Rate uncertainty becomes more important as the repayment period gets longer. |

6. APR, Interest Rate, and Fees: What Borrowers Must Compare

The interest rate is the cost of borrowing the principal amount. The annual percentage rate, or APR, is broader because it can include the interest rate plus certain fees. Consumer finance regulators commonly emphasize APR because it helps borrowers compare the cost of credit more consistently across lenders.

For personal loans, the lowest interest rate is not always the cheapest loan. A loan with a lower rate but a high origination fee may cost more than a loan with a slightly higher rate and no fee. Always compare APR, monthly payment, total repayment amount, fees, and repayment flexibility.

6.1 Common Costs and Fees

| Cost or Fee | What It Means | Why It Matters |

|---|---|---|

| Interest | The charge for borrowing money. | This is usually the largest cost of the loan. |

| APR | A yearly cost measure that may include interest and certain fees. | Useful for comparing loan offers. |

| Origination fee | A fee for processing or funding the loan. | May be deducted from the loan proceeds or added to cost. |

| Late payment fee | A fee charged when a payment is missed or late. | Can increase cost and may harm credit. |

| Returned payment fee | A fee if your bank payment fails. | Can occur when there are insufficient funds. |

| Prepayment penalty | A fee for paying off the loan early. | Can reduce the benefit of early repayment. |

| Rate adjustment terms | Rules for changing a variable rate. | Important for understanding future payment risk. |

7. Eligibility Requirements for Fixed and Variable Personal Loans

Eligibility depends on the lender and the borrower’s financial profile. Fixed and variable personal loans often use similar underwriting standards, but lenders may be more selective for certain variable-rate products because payment risk can change over time.

- Credit history: Lenders review how you have handled past credit accounts.

- Credit score: A stronger score can help you qualify for better terms, though requirements vary.

- Income: Lenders want evidence that you can repay the loan.

- Debt-to-income ratio: This compares your monthly debt obligations with your income.

- Employment or income stability: Consistent income may improve approval chances.

- Loan purpose: Some lenders restrict how personal loan funds can be used.

- Residency, age, and identification requirements: Lenders must verify identity and legal eligibility.

- Bank account: Many lenders require a bank account for funding and automatic payments.

8. When a Fixed-Rate Personal Loan May Be Better

- You need a predictable monthly payment.

- Your budget has little room for surprise increases.

- You are consolidating debt and want a clear payoff date.

- The loan term is medium or long.

- You expect interest rates may rise.

- You prefer simple repayment and do not want to monitor rate changes.

- You are borrowing during a stressful financial period and need certainty.

8.1 Example: Debt Consolidation With a Fixed Rate

Sara has several high-interest credit card balances and wants one predictable monthly payment. She chooses a fixed-rate personal loan because her main goal is stability. Even if market rates change, her loan payment remains the same, making it easier to build the payment into her monthly budget. The key benefit is not just the rate; it is the clear repayment plan.

9. When a Variable-Rate Personal Loan May Be Better

- You can comfortably afford a higher payment if rates rise.

- The starting APR is meaningfully lower than fixed-rate alternatives after fees are considered.

- You plan to repay the loan quickly.

- There is no prepayment penalty or the penalty is small.

- The loan has clear rate caps that limit how high the rate can go.

- You understand the benchmark, adjustment schedule, and payment recalculation method.

- You have emergency savings or reliable cash flow.

9.1 Example: Short-Term Borrowing With a Variable Rate

Daniel needs a personal loan for a short home repair and expects a work bonus within six months. A variable-rate loan offers a lower starting rate, and the agreement has no prepayment penalty. Because he plans to repay quickly and has room in his budget, he may consider the variable option. However, he should still calculate whether he can afford the payment if the rate rises before payoff.

10. Real-World Scenarios: Which Rate Type Fits?

| Scenario | Likely Better Fit | Reason |

|---|---|---|

| Borrower has a tight monthly budget | Fixed rate | Payment predictability matters more than possible savings. |

| Borrower expects to repay in a few months | Variable rate may be considered | Short exposure to rate changes, but only if fees are low and early payoff is allowed. |

| Borrower is consolidating credit cards | Fixed rate | A stable payment supports a clear debt payoff plan. |

| Borrower has unstable income | Fixed rate | Reduced payment uncertainty can lower stress. |

| Borrower has high savings and flexible income | Either, depending on total cost | The borrower may be able to absorb rate changes. |

| Borrower does not understand rate adjustment terms | Fixed rate or pause before borrowing | Confusion about variable terms can lead to expensive mistakes. |

11. How to Compare Fixed and Variable Personal Loan Offers Step by Step

- Step 1: Decide the loan purpose and amount: Borrow only what you need. A lower loan amount reduces interest cost and repayment pressure.

- Step 2: Check your budget: Look at your income, essential expenses, current debt payments, and emergency savings. Decide the highest monthly payment you can afford without relying on perfect conditions.

- Step 3: Compare APR, not just interest rate: APR helps you compare interest and certain fees. Also review the total repayment amount.

- Step 4: Ask whether the payment can change: For fixed loans, confirm the payment schedule. For variable loans, ask how often the rate adjusts and what happens to the payment.

- Step 5: Review all fees: Look for origination fees, late fees, returned payment fees, and prepayment penalties.

- Step 6: Stress-test a variable rate: Ask yourself: Could I afford the payment if the rate increased? If not, a fixed rate may be safer.

- Step 7: Check lender credibility: Use licensed, reputable lenders. Avoid pressure tactics, guaranteed approval claims, and requests for unusual upfront payments.

- Step 8: Read the loan agreement before signing: Make sure the final terms match what you expected. Do not rely only on advertisements or prequalification screens.

- Step 9: Set up a repayment plan: Use automatic payments if appropriate, keep records, and track the payoff date.

- Step 10: Reassess if your finances change: If rates rise, income drops, or repayment becomes difficult, contact the lender early rather than missing payments.

12. Cost Comparison Example: Fixed vs Variable Loan

The following simplified example is for education only. It does not represent a lender quote. Actual payments depend on the loan amount, APR, fees, term, credit profile, and the lender’s calculation method.

| Example Item | Fixed-Rate Loan | Variable-Rate Loan |

|---|---|---|

| Loan amount | $10,000 | $10,000 |

| Starting interest rate | Higher but locked | Lower at the start |

| Payment predictability | Payment stays the same if paid as agreed | Payment may change if the rate adjusts |

| Best-case outcome | Stable cost and clear payoff | Could cost less if rates stay low or fall |

| Worst-case outcome | You miss out on lower market rates | Payment and total cost rise if rates increase |

| Decision question | Is certainty worth the possible higher starting rate? | Can you handle payment increases without financial strain? |

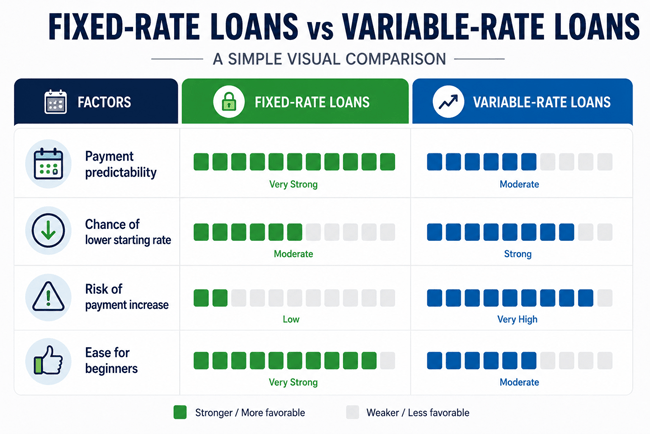

12.1 Simple Visual Comparison

13. Risks of Fixed and Variable Personal Loans

| Risk | Fixed-Rate Loan | Variable-Rate Loan | How to Reduce the Risk |

|---|---|---|---|

| Overborrowing | Possible because the payment looks manageable. | Possible because the starting rate looks attractive. | Borrow only what you need and compare total repayment. |

| Payment shock | Usually low if terms are followed. | Higher because payments may rise. | Stress-test the payment before signing. |

| Fees | Origination or late fees can increase cost. | Same, plus rate adjustment risk. | Read the disclosure and fee schedule. |

| Misleading comparisons | A fixed loan can look costly if only starting rate is compared. | A variable loan can look cheap if future increases are ignored. | Compare APR, total cost, and worst-case payment. |

| Credit damage | Late or missed payments can hurt credit. | Late or missed payments can hurt credit. | Use reminders, autopay, and emergency savings. |

14. Common Mistakes to Avoid

- Comparing only the advertised rate: Advertised rates may apply only to highly qualified borrowers. Compare personalized offers and APR.

- Ignoring fees: Origination fees and other charges can make a low-rate loan more expensive.

- Choosing variable rate without a payment cushion: A variable loan should not be chosen if a modest payment increase would cause missed bills.

- Assuming all personal loans work the same way: Terms vary by lender, country, loan product, and borrower profile.

- Not checking rate caps: If a variable loan has no clear cap or has a high cap, future cost may be difficult to manage.

- Taking a longer term only for a lower payment: A longer term may reduce monthly payments but can increase total interest paid.

- Using a personal loan without fixing the underlying spending problem: Debt consolidation can fail if the borrower keeps adding new debt.

- Skipping the loan agreement: The agreement contains the real terms, including payment changes, fees, and default consequences.

- Falling for loan scams: Be cautious with guaranteed approval, pressure tactics, and requests for upfront payment by unusual methods.

- Borrowing without a payoff plan: A personal loan should have a clear purpose, repayment source, and backup plan.

15. Alternatives to Fixed and Variable Personal Loans

| Alternative | When It May Help | Important Warning |

|---|---|---|

| Emergency savings | For small urgent expenses. | Do not drain all savings if it leaves you exposed. |

| Credit union loan | When you want potentially lower rates or relationship-based lending. | Membership may be required. |

| 0% balance transfer card | For credit card debt you can repay during the promotional period. | Rates can jump after the promotional period, and fees may apply. |

| Home equity loan or HELOC | For homeowners with equity and larger needs. | Your home may be at risk if you cannot repay. |

| Payment plan with provider | For medical bills, tuition, or repairs. | Confirm fees and whether interest applies. |

| Borrowing from family or friends | For limited needs with trusted relationships. | Put terms in writing to prevent conflict. |

| Debt management plan | For borrowers struggling with multiple unsecured debts. | Use reputable nonprofit credit counseling agencies where available. |

| Avoid borrowing | When the purchase is optional or unaffordable. | Delaying may be the safest financial decision. |

16. Expert Tips for Choosing the Right Rate Type

- Match the rate type to your cash-flow stability. If your income is fixed or unpredictable, payment certainty is valuable.

- For variable loans, ask for the maximum possible payment under the agreement, not just the starting payment.

- Use APR as a starting point, but also compare total repayment and fees.

- Do not choose a variable loan only because the first payment looks easier.

- Avoid long repayment terms unless the lower payment is necessary and the total cost still makes sense.

- Check whether autopay discounts require automatic withdrawal and whether you can safely maintain account balances.

- If using a personal loan for debt consolidation, stop using the paid-off credit cards until your finances are stable.

- Keep proof of payments and review statements regularly.

- Prequalify with multiple lenders where available, but understand that final approval may involve a hard credit check.

- Choose the loan you can afford in a bad month, not only in a good month.

17. Quick Action Checklist

- Define why you need the loan and the exact amount required.

- Calculate a safe monthly payment based on your real budget.

- Compare at least a few offers using APR, fees, monthly payment, and total repayment.

- Confirm whether the rate is fixed or variable before applying.

- For variable loans, identify the benchmark, margin, adjustment frequency, and rate caps.

- Ask whether early repayment is allowed without penalty.

- Check the lender’s reputation and licensing where applicable.

- Read the final loan agreement carefully before signing.

- Set payment reminders or autopay only if your bank balance is reliable.

- Build or protect an emergency cushion so one surprise expense does not lead to missed payments.

18. Frequently Asked Questions

18.1 What is the main difference between fixed and variable interest rate personal loans?

A fixed-rate personal loan keeps the same interest rate for the loan term, while a variable-rate personal loan can change based on the loan agreement.

The fixed option is usually more predictable; the variable option may offer savings but carries payment risk.

18.2 Is a fixed-rate personal loan better than a variable-rate loan?

A fixed-rate personal loan is often better for borrowers who need predictable payments.

A variable-rate loan may be better only when the borrower understands the risk, can afford payment increases, and may repay quickly.

18.3 Can my payment increase on a variable-rate personal loan?

Yes.

If your loan agreement allows rate adjustments and the benchmark rate rises, your payment may increase. The exact method depends on the lender’s terms.

18.4 Can my payment increase on a fixed-rate personal loan?

The scheduled payment usually stays the same on a fixed-rate loan if you pay as agreed.

However, late fees, optional products, or loan modifications can change what you owe.

18.5 Why would anyone choose a variable-rate personal loan?

Some borrowers choose variable rates because the starting rate may be lower or because they expect to repay the loan quickly.

The choice only makes sense if the borrower can handle possible rate increases.

18.6 What is APR on a personal loan?

APR stands for annual percentage rate.

It is a yearly cost measure that may include the interest rate and certain fees, making it useful for comparing loan offers.

18.7 Is the lowest interest rate always the best personal loan?

No.

Fees, repayment term, prepayment rules, and total repayment amount also matter. A loan with a low rate but high fees may not be the cheapest.

18.8 Are personal loans usually fixed or variable?

Many personal loans are fixed-rate installment loans, but variable-rate personal loans are also available from some lenders.

Always confirm the rate type before signing.

18.9 What is a rate cap?

A rate cap is a limit on how much a variable interest rate can increase.

Some caps limit each adjustment, while others limit the lifetime rate. Read the agreement to understand the protection.

18.10 Should I choose a fixed rate if interest rates are rising?

A fixed rate can protect you from future increases on that loan.

However, you should still compare APR, fees, and affordability before deciding.

18.11 Should I choose a variable rate if interest rates are falling?

A variable rate may benefit from falling rates, but the benefit is not guaranteed.

The rate adjustment schedule, margin, caps, and lender rules all matter.

18.12 Can I refinance a personal loan later?

Some borrowers refinance by taking a new loan with better terms.

Refinancing may involve a credit check, fees, and no guarantee of approval.

18.13 Do fixed and variable loans have the same eligibility requirements?

They often have similar requirements, such as credit history, income, and debt-to-income ratio.

Specific standards vary by lender and product.

18.14 Are variable-rate personal loans risky?

They can be risky for borrowers with tight budgets because payments may rise.

The risk is lower when the borrower has stable income, savings, a short payoff plan, and clear rate caps.

18.15 What should I ask a lender before choosing a variable-rate loan?

Ask what benchmark is used, what margin is added, how often the rate adjusts, whether there are caps, how payments are recalculated, and whether early payoff has a penalty.

19. Conclusion: The Best Rate Is the One You Can Repay Safely

Fixed and variable interest rate personal loans can both be useful, but they serve different borrower needs. A fixed-rate personal loan is usually easier to understand and budget for because the scheduled payment is predictable. A variable-rate personal loan may start cheaper, but it can become more expensive if rates rise.

The safest decision is not always the loan with the lowest advertised rate. It is the loan with terms you understand, payments you can afford, fees you have reviewed, and risks you can manage. Before signing, compare APR, total repayment amount, rate adjustment rules, fees, and your own monthly budget.

A personal loan should solve a financial problem, not create a bigger one. Choose carefully, borrow only what you need, and build a repayment plan before the money reaches your account.

19.1 Sources Consulted

- Consumer Financial Protection Bureau: guidance on interest rate vs APR and personal installment loan fees.

- Federal Trade Commission: consumer credit disclosures and borrower protection principles.

- Federal Reserve: selected interest rates and broader interest-rate context.

- Citizens Advice: explanation that personal loan variable rates may rise or fall and affect required payments.

- Experian UK and other consumer education sources: APR as a comparison tool for borrowing costs.

Reader Advice: This article is for general educational and informational purposes only and does not constitute individualized financial, legal, tax, accounting, or investment advice. Loan rates, APRs, fees, eligibility, underwriting standards, credit reporting practices, and applicable laws may vary by lender, loan type, borrower profile, location, and current regulations.

Always review the official loan agreement and disclosures, compare offers based on APR, fees, monthly payments, and total repayment cost, and verify current terms with the lender, loan servicer, StudentAid.gov, the SBA, or other relevant official sources when applicable.

If you need advice for your specific situation, especially involving debt disputes, lawsuits, foreclosure, wage garnishment, bankruptcy, or tax matters, consult a qualified financial professional, nonprofit credit counselor, tax adviser, accountant, consumer attorney, or legal aid organization.