Personal Loan Credit Score Requirements

Applying for a personal loan can feel confusing because lenders rarely use one simple approval rule. You may see one lender advertise loans for fair credit, another focus on excellent-credit borrowers, and a third say it considers more than your credit score. That leaves many borrowers asking the same practical question: what credit score do I actually need for a personal loan?

Personal loan credit score requirements are the credit-score standards lenders use when deciding whether to approve you, how much you can borrow, what interest rate you may receive, and whether extra conditions such as a cosigner, collateral, or higher fee may apply. Your score matters because it helps lenders estimate repayment risk, but it is not the only factor. Income, debt-to-income ratio, employment stability, payment history, loan amount, loan purpose, and the lender's own risk rules can all affect the decision.

This guide is written for beginners who want clear, realistic answers before applying. It explains score ranges, typical lender expectations, how credit checks work, what to do if your score is low, and how to avoid expensive mistakes. The goal is not to push you into borrowing. It is to help you decide whether a personal loan is likely to help, whether you should wait, and how to compare offers safely.

Reader Advice

There is no universal minimum credit score for every personal loan. Each lender sets its own rules, and the same borrower may be approved by one lender and declined by another.

1. What Are Personal Loan Credit Score Requirements?

Personal loan credit score requirements are the minimum or preferred credit-score levels a lender uses when reviewing an unsecured or secured personal loan application. In plain English, they are the credit-score benchmarks that influence whether you qualify and what loan terms you receive.

A credit score is a three-digit number, commonly ranging from 300 to 850 for many general-purpose consumer scoring models, that estimates how likely you are to repay borrowed money on time. The Federal Trade Commission explains that credit scores are calculated in different ways and that many lenders use FICO scores when evaluating credit risk. FICO also notes that lenders may consider information beyond the score, including income, job history, and the type of credit requested.

| Term | Plain-English Meaning | Why It Matters |

|---|---|---|

| Credit score | A number that summarizes credit risk based on credit report information. | Higher scores often help borrowers qualify for better rates and terms. |

| Credit report | A record of credit accounts, payment history, balances, inquiries, and certain public-record or collection information. | Your score is usually calculated from report data, so errors can affect approval. |

| Minimum credit score | The lowest score a lender may consider for approval. | Meeting it does not guarantee approval; missing it may lead to denial. |

| Preferred credit score | The score range where a lender may offer stronger rates and higher approval odds. | This can affect total borrowing cost. |

| Soft inquiry | A credit check that does not affect your score. | Common during prequalification. |

| Hard inquiry | A credit check tied to a formal credit application. | May cause a small, temporary score change. |

2. How Personal Loan Credit Score Requirements Work

When you apply for a personal loan, the lender evaluates your application through underwriting. Underwriting is the process of deciding whether the lender is willing to lend, how much, at what interest rate, and under what conditions.

2.1 The lender checks your credit profile

The lender may review one or more credit reports and scores. Some lenders rely heavily on FICO-based scores, while others use VantageScore, internal scoring models, alternative data, or a combination of methods. Because scoring models vary, your score may not be identical across apps, bureaus, or lenders.

2.2 The score is matched against the lender's risk bands

Many lenders group applicants into broad score bands such as poor, fair, good, very good, and excellent. These bands help the lender estimate risk. A higher score generally suggests a stronger history of paying bills as agreed, while a lower score may signal late payments, high balances, short credit history, collections, or other risk indicators.

2.3 The lender reviews non-score factors

Even a strong score may not be enough if the loan payment would strain your budget. Lenders commonly review income, existing debt, monthly obligations, employment or income stability, requested loan amount, loan term, and whether the loan is unsecured or secured.

2.4 The lender prices the loan

Credit score can affect pricing. Borrowers with stronger credit profiles are more likely to receive lower APRs, fewer fees, and larger loan limits. Borrowers with weaker credit may face higher APRs, smaller loan amounts, shorter repayment terms, origination fees, or a requirement to add a cosigner or collateral.

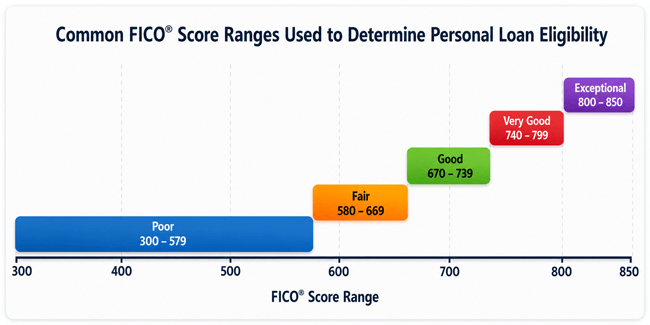

3. Typical Credit Score Ranges for Personal Loans

The following ranges are commonly used to describe FICO credit quality. They are not approval guarantees, but they help borrowers understand where they may stand before applying.

| Credit Score Range | Common Label | What It May Mean for Personal Loans |

|---|---|---|

| 300-579 | Poor | Approval may be difficult with mainstream lenders. Some lenders may require secured borrowing, a cosigner, high APRs, or smaller loan amounts. Watch carefully for predatory terms. |

| 580-669 | Fair | Some lenders may approve borrowers in this range, especially with steady income and low debt. Rates may be higher than average. |

| 670-739 | Good | Often a stronger position for approval and more competitive offers, assuming income and debt levels also fit lender rules. |

| 740-799 | Very Good | Usually improves access to lower APRs, higher loan limits, and better lender selection. |

| 800-850 | Exceptional | Often qualifies for the strongest advertised terms, though income and debt still matter. |

Reader Advice

Most borrowers have a better chance of qualifying for a personal loan once their credit score is at least in the fair range, but favorable terms are more common with good to excellent credit. No credit score guarantees approval because lenders also evaluate income, debt, credit history, and loan amount.

4. Why Credit Score Matters for Personal Loans

Your credit score matters because personal loans are often unsecured. Unsecured means you do not pledge collateral, such as a car title or savings account, that the lender can claim if you fail to repay. Since the lender is taking more risk, your credit profile becomes a major part of the decision.

4.1 A higher score can improve your borrowing options

- More lenders may be willing to review your application.

- You may qualify for lower APRs, which can reduce the total cost of the loan.

- You may qualify for a larger loan amount or longer repayment term.

- You may have more negotiating power because you can compare multiple offers.

4.2 A lower score can make borrowing more expensive

- You may be approved only by lenders that charge higher APRs or fees.

- You may receive a smaller loan amount than requested.

- You may be asked for a cosigner, collateral, or proof of stronger income.

- You may be denied if recent late payments, collections, or high debt make the loan too risky.

5. Credit Score vs Other Personal Loan Approval Factors

A credit score is important, but lenders do not usually approve loans based on score alone. A borrower with a good score but unstable income may still be denied. A borrower with fair credit but strong income, low debt, and a clean recent payment record may still qualify.

| Approval Factor | What Lenders Look For | How to Improve It |

|---|---|---|

| Credit score | Overall credit risk based on credit report data. | Pay on time, reduce revolving balances, avoid unnecessary applications, and correct report errors. |

| Payment history | Whether you have paid credit accounts on time. | Set autopay reminders and bring overdue accounts current where possible. |

| Debt-to-income ratio | How much of your income is already committed to debt payments. | Pay down debt, increase income, or request a smaller loan. |

| Income consistency | Whether you can afford the new monthly payment. | Prepare pay stubs, tax returns, bank statements, or benefit documentation. |

| Credit utilization | How much available revolving credit you are using. | Lower credit card balances before applying. |

| Credit history length | How long your accounts have been open. | Avoid closing old accounts without understanding the impact. |

| Recent credit applications | How many hard inquiries or new accounts appear recently. | Space out applications and use prequalification tools first. |

| Loan amount and term | Whether the requested payment fits your financial profile. | Borrow only what you need and compare payment options. |

6. Step-by-Step Process: Check Your Readiness Before Applying

Use this process before submitting a formal application. It can help you reduce avoidable denials and compare offers more safely.

- Check your credit reports. Review reports from Equifax, Experian, and TransUnion for late payments, collections, incorrect balances, unfamiliar accounts, and wrong personal information. AnnualCreditReport.com states that free weekly online credit reports are available from the three nationwide credit reporting companies.

- Check your credit score. Use a reputable bank, credit card issuer, credit bureau, or scoring service. Remember that the score you see may differ from the score a lender uses.

- Estimate your debt-to-income ratio. Add your monthly debt payments and divide by gross monthly income. A lower ratio usually gives lenders more confidence.

- Decide how much you truly need. Borrowing more than necessary can increase your payment, APR, and approval difficulty.

- Use prequalification where available. Prequalification commonly uses a soft inquiry and can show estimated rates without a hard credit check, though it is not a final approval.

- Compare APR, not just monthly payment. APR includes interest and certain fees, making it a better comparison tool than the payment alone.

- Read fees and repayment terms. Look for origination fees, late fees, prepayment penalties, repayment length, and automatic payment discounts.

- Apply only when the offer fits your budget. A formal application may trigger a hard inquiry and requires documentation.

7. Personal Loan Options by Credit Score Range

| Your Situation | Likely Options | Best Next Move |

|---|---|---|

| Excellent or very good credit | Banks, credit unions, online lenders, debt consolidation loans, large unsecured loans. | Compare several prequalified APRs and terms before applying. |

| Good credit | Most mainstream lenders, especially with stable income and manageable debt. | Shop around; small APR differences can matter over the life of the loan. |

| Fair credit | Online lenders, credit unions, smaller loan amounts, possible higher APRs. | Prequalify, reduce credit card balances, and consider a credit union. |

| Poor credit | Secured personal loans, credit-builder alternatives, cosigner options, local credit unions, nonprofit credit counseling. | Avoid high-cost loans, check for scams, and consider waiting if the loan is not urgent. |

| Thin credit file | Credit union loans, secured loans, small starter loans, lenders that consider income and banking history. | Build credit history and prepare income documentation. |

8. Benefits of Meeting Strong Credit Score Requirements

- Lower borrowing cost: A better credit profile may help you qualify for a lower APR.

- More lender choice: You can compare banks, credit unions, and online lenders instead of taking the first offer.

- Better debt consolidation results: Lower APRs can make consolidation more useful when replacing higher-rate debt.

- Fewer restrictive conditions: Strong credit can reduce the need for collateral or a cosigner.

- Improved approval confidence: You are less likely to waste time applying where you are unlikely to qualify.

9. Costs, Fees, and Risks to Understand

Credit score requirements are only part of the decision. The loan must also be affordable and safe.

| Cost or Risk | What It Means | What to Do |

|---|---|---|

| APR | The yearly cost of borrowing, including interest and certain fees. | Compare APR across lenders, not just interest rate. |

| Origination fee | A fee some lenders deduct from the loan proceeds or add to cost. | Ask whether the fee reduces the cash you receive. |

| Late fee | A charge if you miss or delay a payment. | Use autopay and keep an emergency buffer. |

| Prepayment penalty | A fee for paying off the loan early, where allowed. | Choose lenders with no prepayment penalty when possible. |

| Hard inquiry | A formal credit check tied to an application. | Use prequalification first and limit unnecessary applications. |

| Debt trap risk | Borrowing to cover spending without fixing the budget problem. | Use a repayment plan and avoid taking on new debt after consolidation. |

| Predatory lending | Loans with abusive fees, unclear terms, pressure tactics, or unaffordable payments. | Avoid lenders that guarantee approval, demand upfront fees, or hide APR. |

10. Good Credit vs Fair Credit vs Bad Credit Personal Loan Experience

| Feature | Good/Excellent Credit | Fair Credit | Poor Credit |

|---|---|---|---|

| Approval odds | Generally stronger | Possible but lender-dependent | More difficult |

| APR range | More likely to be competitive | Often higher | Often high or unavailable |

| Loan amount | May qualify for larger amounts | May be limited | Often smaller |

| Fees | May have fewer fees | Origination fees more common | Fees can be expensive |

| Best strategy | Compare multiple offers | Prequalify and improve weak factors | Consider alternatives and avoid predatory loans |

11. Real-World Examples

11.1 Example 1: Good credit borrower consolidating credit cards

Maria has a good credit score, steady income, and several credit card balances. She wants one fixed monthly payment. She checks her credit reports, prequalifies with three lenders, and compares APRs and origination fees. Because her score and income are strong enough, she may qualify for a lower APR than her credit cards. The personal loan could help if she stops adding new card debt and keeps the payment affordable.

11.2 Example 2: Fair credit borrower with high credit card balances

James has fair credit. His payment history is mostly clean, but his credit cards are close to their limits. He prequalifies and receives offers with higher APRs than expected. Instead of applying immediately, he uses two months to reduce card balances and update his budget. Lower balances may improve his credit utilization and make his application stronger.

11.3 Example 3: Poor credit borrower facing an emergency

Nadia has recent late payments and needs funds for an urgent car repair. Several lenders decline her. One lender offers a loan with very high fees and a payment she cannot comfortably afford. She pauses before accepting, asks her credit union about a smaller secured loan, checks local assistance programs, and avoids any lender asking for an upfront approval fee. In her case, protecting her cash flow may be more important than getting a fast loan.

11.4 Example 4: Strong score but denied anyway

Omar has a very good credit score but recently changed jobs and requested a large loan. The lender denies him because his debt-to-income ratio is too high after including the proposed payment. This shows why credit score requirements are not the whole story. A smaller loan amount, longer documented income history, or lower existing debt could improve his chances.

12. Expert Tips to Improve Personal Loan Approval Odds

- Check all three credit reports before applying, not just one score in an app.

- Dispute genuine errors with the credit bureau and the creditor before applying if time allows.

- Lower credit card balances, especially cards near their limits.

- Avoid opening multiple new accounts shortly before a loan application.

- Use prequalification tools to compare estimated offers with soft inquiries where available.

- Apply for a realistic loan amount based on your budget, not the maximum advertised amount.

- Consider credit unions, especially if you have fair credit or an existing relationship.

- Prepare proof of income before applying to reduce delays.

- Read the full loan agreement before accepting funds.

- Walk away from lenders that pressure you, hide APR, or guarantee approval regardless of credit.

13. Common Mistakes to Avoid

| Mistake | Why It Hurts | Better Approach |

|---|---|---|

| Assuming one score is the lender score | Different models and bureaus can produce different scores. | Use your score as a guide, not a guarantee. |

| Applying with many lenders without prequalification | Multiple hard inquiries may affect your credit and signal risk. | Prequalify first when possible. |

| Ignoring APR and focusing only on payment | A longer term can lower payment but raise total cost. | Compare APR, fees, term, and total repayment. |

| Borrowing more than needed | A larger loan may be harder to approve and more expensive. | Borrow the minimum amount that solves the problem. |

| Using a personal loan without fixing spending habits | Debt can return after consolidation. | Create a budget and stop adding new high-interest debt. |

| Missing credit report errors | Incorrect negative information can lower scores unfairly. | Review reports and dispute inaccuracies. |

| Choosing a predatory lender | High fees and unaffordable payments can worsen financial stress. | Verify lender reputation and read the agreement carefully. |

14. Quick Action Checklist

- Review your credit reports from all three major credit reporting companies.

- Check your current credit score and note the scoring model if shown.

- List your monthly debt payments and estimate debt-to-income ratio.

- Decide the smallest loan amount that meets your goal.

- Prequalify with multiple reputable lenders before formally applying.

- Compare APR, fees, loan term, monthly payment, and total repayment.

- Confirm whether the lender charges an origination fee or prepayment penalty.

- Prepare income documents before applying.

- Avoid any lender asking for upfront approval fees or guaranteeing approval.

- Apply only when the loan improves your situation and fits your budget.

15. Frequently Asked Questions About Personal Loan Credit Score Requirements

15.1 What credit score do I need for a personal loan?

There is no universal minimum. Many lenders prefer fair credit or better, and stronger terms are more common with good to excellent credit. Some lenders may work with lower scores if income, debt, and other factors support approval.

15.2 Can I get a personal loan with a 580 credit score?

Possibly. A 580 score is often considered fair in common FICO ranges. Some lenders may consider applicants around this range, but APRs and fees may be higher and approval is not guaranteed.

15.3 Can I get a personal loan with bad credit?

Yes, but options may be limited and expensive. You may need a secured loan, cosigner, credit union, smaller loan amount, or alternative assistance. Avoid lenders that use pressure tactics or hide costs.

15.4 Does prequalifying for a personal loan hurt my credit score?

Prequalification commonly uses a soft inquiry, which does not affect your score. A formal application usually involves a hard inquiry, which may have a small, temporary impact.

15.5 Why was I denied with a good credit score?

A good score does not guarantee approval. Common reasons include high debt-to-income ratio, insufficient income, unstable employment, recent credit applications, unverifiable information, or requesting too much money.

15.6 Is FICO or VantageScore used for personal loans?

It depends on the lender. Many lenders use FICO scores, but some use VantageScore, internal models, or multiple data points. Ask the lender which score range it considers if the information is available.

15.7 What is the best credit score for a personal loan?

The higher the better, but excellent credit is not always required. Borrowers in good, very good, or exceptional ranges generally have stronger access to competitive rates and terms.

15.8 How can I improve my credit score before applying?

Pay bills on time, reduce credit card balances, avoid unnecessary new credit, correct credit report errors, and keep older positive accounts open when appropriate.

15.9 Do personal loans help build credit?

They can if you make every payment on time. However, missed payments can damage credit, and taking on unaffordable debt can create long-term problems.

15.10 Will a personal loan lower my credit score?

It may cause short-term changes because of a hard inquiry and a new account. Over time, responsible payments may help, while missed payments can hurt significantly.

15.11 What if I have no credit history?

A thin credit file can make approval harder. Consider a credit union, secured loan, credit-builder loan, authorized-user strategy, or building credit before applying.

15.12 Do lenders only look at credit score?

No. Lenders may also review income, debt-to-income ratio, employment, payment history, loan amount, and the purpose or structure of the loan.

15.13 Are credit unions easier for personal loans?

Sometimes. Credit unions may consider member relationships and may offer smaller loans or more flexible underwriting, but approval standards still apply.

15.14 Should I use a cosigner for a personal loan?

A cosigner may improve approval odds if they have strong credit and income, but they become legally responsible for the debt if you do not pay.

15.15 How long should I wait after improving my score to apply?

Wait until your credit reports reflect the improvements, such as lower balances or corrected errors. Timing varies by creditor reporting cycles, so check your updated reports and score before applying.

15.16 Sources Consulted

This article is educational and is not personalized financial, legal, or credit advice. Requirements vary by lender, product, state, and borrower profile. For personal guidance, consider speaking with a qualified financial counselor, a reputable nonprofit credit counselor, or the lender before applying.

- Federal Trade Commission (FTC): Credit Scores and Free Credit Reports consumer education.

- AnnualCreditReport.com: Official access point for free credit reports from Equifax, Experian, and TransUnion.

- myFICO: FICO score education, score ranges, and scoring-factor explanations.

- Experian: Personal loan credit score and prequalification education.

- Equifax: Credit score education and credit-score factor explanations.

- Consumer Financial Protection Bureau (CFPB) and USA.gov: Consumer finance education, complaint resources, and credit-reporting information.

16. Conclusion: Know Your Score, But Do Not Stop There

Personal loan credit score requirements matter because they influence approval odds, APR, loan amount, fees, and the lenders available to you. But your score is only one part of the decision. Lenders also care about your income, existing debts, payment history, recent applications, and whether the new payment fits your budget.

Before applying, check your credit reports, understand your score range, prequalify where possible, compare APRs and fees, and borrow only what you can comfortably repay. If your score is lower than you hoped, do not panic. You may still have options, but the safest move may be to improve your credit profile, lower debt, or consider a credit union or secured alternative before accepting an expensive loan.

The best personal loan is not simply the loan you can get. It is the loan that solves a real financial need, fits your budget, and leaves you in a stronger position after repayment.

Reader Advice: This article is for general educational and informational purposes only and does not constitute individualized financial, legal, tax, accounting, or investment advice. Loan rates, APRs, fees, eligibility, underwriting standards, credit reporting practices, and applicable laws may vary by lender, loan type, borrower profile, location, and current regulations.

Always review the official loan agreement and disclosures, compare offers based on APR, fees, monthly payments, and total repayment cost, and verify current terms with the lender, loan servicer, StudentAid.gov, the SBA, or other relevant official sources when applicable.

If you need advice for your specific situation, especially involving debt disputes, lawsuits, foreclosure, wage garnishment, bankruptcy, or tax matters, consult a qualified financial professional, nonprofit credit counselor, tax adviser, accountant, consumer attorney, or legal aid organization.