What Is a Mortgage?

1. Why Understanding Mortgages Matters

A mortgage is often the largest financial commitment a person makes. It can help you buy a home without paying the full price upfront, but it also creates a long-term legal and financial obligation. Understanding the basics before you apply can help you avoid expensive surprises, compare offers more confidently, and choose a loan that fits your life rather than only your dream house.

This guide is for first-time homebuyers, homeowners thinking about refinancing, renters planning for a future purchase, and anyone who wants a plain-English explanation of mortgage terms. Many people worry about monthly payments, interest rates, down payments, closing costs, credit scores, and what could happen if income changes later. Those concerns are valid. A mortgage can be useful, but it should be entered with care.

The goal is not to push you toward borrowing. The goal is to help you understand what a mortgage is, how it works, what it costs, what risks to watch for, and what practical steps you can take before signing loan documents.

2. Mortgage Definition: What Is a Mortgage?

A mortgage is a loan used to buy, refinance, or borrow against real estate. The property acts as collateral, which means the lender has a legal claim against the property if the borrower fails to repay the loan according to the agreement.

In everyday conversation, people often say “mortgage” when they mean the home loan itself. Technically, the mortgage is the legal security agreement tied to the property, while the promissory note is the borrower’s promise to repay. For most consumers, it is enough to understand that a mortgage is a secured home loan with scheduled payments over time.

3. What a Mortgage Is - and What It Is Not

| Term | Simple meaning | Why it matters |

|---|---|---|

| Mortgage | A real estate loan secured by the property | The lender can foreclose if the loan is not repaid |

| Home loan | Common everyday term for a mortgage | Often used interchangeably with mortgage |

| Rent | Payment to use someone else’s property | Rent does not usually build ownership equity |

| Deed | Document showing property ownership | The borrower can own the home while still owing the mortgage |

| Title | Legal ownership rights in a property | Title problems can affect the purchase or refinancing process |

4. How a Mortgage Works

A mortgage works by allowing a borrower to buy or refinance property now and repay the lender over time. The borrower usually makes a down payment, receives the loan funds at closing, and then makes monthly payments that may include principal, interest, taxes, insurance, and mortgage insurance.

4.1. The Basic Mortgage Process

- You estimate your budget and decide how much house you can realistically afford.

- You compare lenders and apply for preapproval or loan approval.

- The lender reviews your credit, income, debts, assets, employment, and the property.

- You receive disclosures, including a Loan Estimate that helps you compare costs and terms.

- The property is appraised and title work is completed.

- You review final documents, including the Closing Disclosure, before signing.

- After closing, you repay the loan through regular monthly payments.

The Consumer Financial Protection Bureau (CFPB) encourages borrowers to use the Loan Estimate and Closing Disclosure to compare mortgage offers and understand final loan costs before closing. The FTC also warns consumers to be alert for deceptive mortgage advertising and foreclosure-relief scams. Sources consulted are listed at the end of this document.

5. The Main Parts of a Mortgage Payment

A monthly mortgage payment is often more than just the loan repayment. Many payments include PITI: principal, interest, taxes, and insurance.

| Payment part | What it means | Beginner tip |

|---|---|---|

| Principal | The amount borrowed that you still owe | Paying principal builds equity |

| Interest | The cost of borrowing money | The rate and loan term strongly affect total cost |

| Property taxes | Local taxes assessed on the home | Often collected through escrow |

| Homeowners insurance | Insurance that protects the home against covered losses | Lenders usually require it |

| Mortgage insurance | Extra protection for the lender on some low-down-payment loans | It can increase monthly cost |

| HOA dues | Fees paid to a homeowners association, if applicable | Usually separate from the mortgage payment |

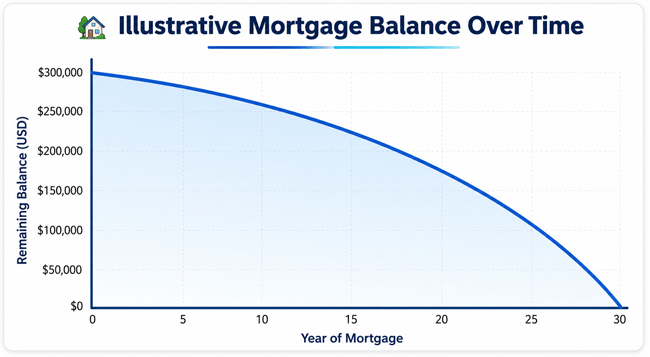

6. Mortgage Amortization: Why Early Payments Feel Slow

Most traditional mortgages are amortizing loans. That means each payment is split between interest and principal. Early in the loan, a larger share goes to interest because the balance is still high. Later, more of each payment goes toward principal.

The chart below is illustrative only. It shows how a $300,000 mortgage balance could decline over a 30-year repayment period. Actual results depend on loan amount, interest rate, payment timing, extra payments, and loan terms.

7. Common Types of Mortgages

The right mortgage type depends on your credit, down payment, income, property, location, military status, and long-term plans. Always compare eligibility rules, monthly payment, total cost, and risk.

| Mortgage type | Best for | Key consideration |

|---|---|---|

| Fixed-rate mortgage | Borrowers who want predictable payments | Interest rate stays the same for the loan term |

| Adjustable-rate mortgage (ARM) | Borrowers who can handle future payment changes | Rate may adjust after an initial period |

| Conventional loan | Borrowers with solid credit and stable finances | May require private mortgage insurance with a smaller down payment |

| FHA loan | Some first-time buyers or borrowers with lower credit profiles | Mortgage insurance costs can apply |

| VA loan | Eligible service members, veterans, and certain surviving spouses | Eligibility rules apply; funding fee may apply |

| USDA loan | Eligible rural and some suburban buyers | Property and income limits apply |

| Jumbo loan | Higher-priced homes above conforming loan limits | Stricter qualification standards are common |

| Interest-only mortgage | Special situations with advanced planning | Higher risk if principal is not being reduced |

8. Fixed-Rate Mortgage vs Adjustable-Rate Mortgage

| Feature | Fixed-rate mortgage | Adjustable-rate mortgage |

|---|---|---|

| Interest rate | Stays the same for the loan term | Can change after the initial fixed period |

| Monthly payment | More predictable | Can rise or fall when the rate adjusts |

| Best for | Long-term owners who value stability | Borrowers with a clear plan and tolerance for payment changes |

| Main risk | Initial rate may be higher than some ARMs | Future payment shock if rates rise |

| Beginner-friendly? | Often easier to understand | Requires careful reading of caps, index, margin, and adjustment rules |

9. Why Mortgages Matter

- They make homeownership possible without paying the full purchase price in cash.

- They affect monthly cash flow for many years.

- They can help build home equity over time when payments are made responsibly.

- They expose borrowers to serious risk if payments become unaffordable.

- They influence major life choices, including where you live, how much you save, and when you can move.

10. Benefits of a Mortgage

| Benefit | How it helps | Practical caution |

|---|---|---|

| Access to homeownership | You can buy property without paying the full price upfront | Borrow only what you can afford, not only what a lender approves |

| Predictable housing cost with fixed-rate loans | Principal and interest stay stable on a fixed-rate mortgage | Taxes, insurance, and HOA costs can still rise |

| Equity building | Part of each payment can reduce the loan balance | Home values can rise or fall |

| Potential financial flexibility | Cash stays available for emergencies or other goals | High debt can reduce flexibility later |

| Refinancing opportunities | You may replace the loan if better terms become available | Refinancing has costs and is not always worth it |

11. Mortgage Costs and Fees

Mortgage costs vary by lender, location, loan type, property, credit profile, and market conditions. Ask for written estimates and compare the annual percentage rate (APR), loan terms, cash needed to close, and total cost over time.

| Cost or fee | What it is | What to ask |

|---|---|---|

| Down payment | Money you pay upfront toward the purchase price | How much is required and how does it affect monthly payment? |

| Origination fee | Fee charged by a lender to make the loan | Is it optional, negotiable, or included in the rate? |

| Discount points | Upfront cost to buy a lower interest rate | How long is the break-even period? |

| Appraisal fee | Cost to estimate the property’s value | Is a waiver available? |

| Title and settlement fees | Costs for title search, insurance, and closing services | Can I shop for these services? |

| Prepaid taxes and insurance | Amounts paid upfront for escrow or coverage | How much cash will I need at closing? |

| Mortgage insurance | Insurance that protects the lender, not the borrower | When can it be removed or reduced? |

12. Risks of a Mortgage

- Foreclosure risk: If you fall seriously behind, the lender may be able to take legal action to sell the property.

- Payment shock: Adjustable-rate loans, rising insurance, higher property taxes, or expired temporary buydowns can increase monthly payments.

- Overborrowing: A lender’s approval amount may be higher than what is comfortable for your real budget.

- Low equity or negative equity: If home values fall, you may owe more than the home is worth.

- Refinancing risk: Future refinancing is never guaranteed because rates, credit, income, and property values can change.

- Complex documents: Misunderstanding loan terms can lead to costly decisions.

13. Step-by-Step: How to Get a Mortgage

- Check your credit reports and correct errors before applying.

- Estimate your affordable monthly payment using your income, debts, savings, taxes, insurance, and emergency fund needs.

- Save for a down payment, closing costs, moving costs, repairs, and a cash cushion.

- Compare at least several lenders, including banks, credit unions, mortgage companies, and brokers where appropriate.

- Request written Loan Estimates for the same loan amount, loan type, and rate-lock period so comparisons are fair.

- Review the interest rate, APR, monthly payment, closing costs, prepayment penalties, and whether the payment can change.

- Choose a loan and lock the rate only after understanding the terms.

- Read the Closing Disclosure carefully and compare it with the Loan Estimate before signing.

- Set up automatic payments only after confirming due dates, grace periods, and escrow details.

- Keep records and contact your servicer early if you ever expect trouble making payments.

14. Real-World Mortgage Examples

14.1. Example 1: First-Time Buyer Choosing Stability

Maya wants a home she can keep for at least seven years. She has steady income but does not want payment surprises. A fixed-rate mortgage may fit her better than an adjustable-rate mortgage because predictable principal and interest payments help her plan around childcare, savings, and repairs.

14.2. Example 2: Buyer Comparing Monthly Payment vs Total Cost

Daniel compares a shorter-term loan with a longer-term loan. The shorter term has a higher monthly payment but could reduce total interest. The longer term offers a lower monthly payment, but he may pay more over the life of the loan. The better choice depends on emergency savings, job stability, other debts, and whether he will keep the home long enough for the cost difference to matter.

14.3. Example 3: Homeowner Considering Refinancing

A homeowner sees an advertisement for a lower rate. Before refinancing, she compares closing costs, the new loan term, monthly savings, break-even point, and whether the new loan restarts the repayment clock. A lower monthly payment is not automatically a better deal if total lifetime cost increases.

15. Pros and Cons of Getting a Mortgage

| Pros | Cons |

|---|---|

| Can help you buy a home sooner | Creates long-term debt |

| May build equity over time | Home value is not guaranteed to rise |

| Fixed-rate loans can offer predictable principal and interest | Taxes, insurance, and maintenance can increase |

| Can be refinanced if conditions are favorable | Refinancing costs money and approval is not guaranteed |

| May support family stability and long-term planning | Missed payments can damage credit and risk foreclosure |

16. Common Mortgage Mistakes to Avoid

- Shopping only by interest rate and ignoring fees, APR, loan term, and mortgage insurance.

- Assuming preapproval means the payment is affordable in real life.

- Forgetting property taxes, insurance, HOA dues, repairs, utilities, and moving costs.

- Choosing an ARM without understanding when and how the payment can change.

- Draining all savings for the down payment and having no emergency fund after closing.

- Making major credit changes before closing, such as financing a car or opening new credit cards.

- Ignoring the Closing Disclosure or signing under pressure without asking questions.

- Believing “no closing cost” means free; costs may be built into the rate or loan balance.

- Assuming refinancing later will solve an affordability problem.

- Waiting until payments are already missed before contacting the loan servicer.

17. Expert Tips for Beginners

- Think in terms of total housing cost, not just the mortgage payment.

- Keep a separate emergency fund for repairs and income disruption.

- Compare loans using the same assumptions: loan amount, term, rate-lock period, points, and down payment.

- Ask lenders to explain every fee you do not understand.

- Read the “Can this amount increase after closing?” section of your disclosures carefully.

- Avoid stretching your budget just because you expect future income growth.

- Consider how long you realistically plan to stay in the home before paying points or refinancing.

- Treat mortgage ads as starting points, not final offers.

18. Quick Action Checklist

- Write down your comfortable monthly housing budget.

- Check credit reports and fix errors early.

- Estimate cash needed for down payment, closing costs, moving, repairs, and reserves.

- Compare multiple lenders using written Loan Estimates.

- Review the interest rate, APR, total monthly payment, cash to close, and whether the payment can change.

- Ask about mortgage insurance and when it can be removed.

- Read the Closing Disclosure before closing day.

- Keep copies of all mortgage documents.

- Contact your servicer early if payment trouble appears.

19. Frequently Asked Questions About Mortgages

19.1. What is a mortgage in simple terms?

A mortgage is a loan used to buy or refinance property. The home is collateral, so the lender can take legal action if the borrower does not repay.

19.2. Is a mortgage the same as a home loan?

In everyday use, yes. People usually use “mortgage” and “home loan” to mean the same thing, although mortgage can also refer to the legal security interest in the property.

19.3. Who owns the house when you have a mortgage?

The buyer usually owns the home, but the lender has a secured interest in it until the mortgage is repaid. Ownership details can vary by state and legal structure.

19.4. What are the main parts of a mortgage payment?

The main parts are principal and interest. Many payments also include property taxes, homeowners insurance, and mortgage insurance through escrow.

19.5. What is principal on a mortgage?

Principal is the amount of money borrowed that you still owe. Paying principal reduces the loan balance and helps build equity.

19.6. What is mortgage interest?

Mortgage interest is the cost of borrowing money. It is calculated based on the loan balance, interest rate, and repayment schedule.

19.7. What is a fixed-rate mortgage?

A fixed-rate mortgage has an interest rate that stays the same for the life of the loan. This makes principal and interest payments more predictable.

19.8. What is an adjustable-rate mortgage?

An adjustable-rate mortgage has a rate that can change after an initial period. Payments may rise or fall depending on the loan rules and market conditions.

19.9. What is mortgage insurance?

Mortgage insurance protects the lender if the borrower defaults. It may be required on some loans, especially when the down payment is small.

19.10. What are closing costs?

Closing costs are fees and prepaid expenses paid when the mortgage is finalized. They can include lender fees, title fees, appraisal fees, taxes, and insurance-related costs.

19.11. Can you pay off a mortgage early?

Many mortgages allow early payoff, but borrowers should check whether a prepayment penalty applies. Extra principal payments can reduce interest cost and shorten repayment time.

19.12. What happens if you cannot pay your mortgage?

Contact your servicer as early as possible. Options may include repayment plans, forbearance, modification, selling the home, or other assistance depending on the situation.

19.13. Is refinancing a mortgage always a good idea?

No. Refinancing can help if it lowers cost or improves terms, but it may add fees, extend the repayment period, or increase total interest.

19.14. How do I compare mortgage offers?

Compare Loan Estimates using the same loan amount and assumptions. Look at interest rate, APR, monthly payment, cash to close, rate type, points, and whether costs can change.

19.15. How much mortgage can I afford?

A lender can estimate what you qualify for, but affordability should be based on your full budget, emergency savings, debts, taxes, insurance, repairs, and lifestyle needs.

20. Conclusion: The Smart Way to Think About a Mortgage

A mortgage is a powerful financial tool, but it is not just a monthly payment. It is a secured loan tied to your home, your cash flow, your long-term plans, and your risk tolerance.

The best mortgage is not always the one with the lowest advertised rate. It is the loan you understand, can afford, and can manage through normal life changes. Before you sign, compare written offers, read the disclosures, ask questions, and leave room in your budget for taxes, insurance, repairs, and emergencies.

Used wisely, a mortgage can help you build a stable home and long-term equity. Used carelessly, it can create stress and financial risk. The practical next step is simple: learn the terms, compare carefully, and borrow based on your real budget rather than the maximum amount available.

20.1. Sources Consulted

- Consumer Financial Protection Bureau (CFPB), Know Before You Owe: Mortgages - https://www.consumerfinance.gov/know-before-you-owe/

- CFPB, Loan Estimate and Closing Disclosure forms and samples - https://www.consumerfinance.gov/compliance/compliance-resources/mortgage-resources/tila-respa-integrated-disclosures/forms-samples/

- USA.gov, Consumer Financial Protection Bureau overview - https://www.usa.gov/agencies/consumer-financial-protection-bureau

- Federal Reserve, Consumer Handbook on Adjustable Rate Mortgages - https://www.federalreserve.gov/pubs/arms/armstext_cover2005.pdf

- Federal Reserve, A Consumer’s Guide to Mortgage Refinancings - https://www.federalreserve.gov/pubs/refinancings/

- Federal Trade Commission, Mortgages and consumer protection - https://www.ftc.gov/business-guidance/credit-finance/mortgages

Reader Advice: This article is written for educational purpose only and should not be taken as personalized financial, legal, tax, or mortgage advice. Mortgage rules, lender overlays, interest rates, assistance programs, and eligibility standards can change. Always verify details with licensed mortgage professionals, official program sources, and your lender before making a home-buying decision. Borrowers should compare current lender offers and consult qualified professionals before making a decision.