How Much House Can I Afford?

Buying a home is not only a real estate decision. It is a long-term cash-flow decision that can affect your savings, debt, lifestyle, retirement planning, and ability to handle emergencies. The question “How much house can I afford?” is really asking: What home price can I buy without becoming financially stretched?

This matters because the amount a lender may approve is not always the amount you should comfortably borrow. A mortgage approval focuses on whether you meet underwriting rules. Your personal affordability should also include groceries, transportation, childcare, healthcare, insurance, savings goals, repairs, and the possibility that life will not go exactly as planned.

This guide is for first-time home buyers, repeat buyers, renters preparing to buy, families comparing neighborhoods, and anyone trying to avoid becoming house poor. You will learn how mortgage affordability works, how lenders estimate risk, how to calculate your own safe price range, and how to make a practical home-buying decision.

1. What Does “How Much House Can I Afford?” Mean?

Home affordability is the estimated home price and monthly housing payment you can manage based on your income, debts, cash savings, loan terms, and ongoing ownership costs. It is not just the listing price of the property. It is the full cost of owning the home each month and the cash you need before and after closing.

Concise Definition You can afford a house when the monthly payment, upfront cash needed, ongoing ownership costs, and emergency savings fit comfortably within your income and financial goals without forcing you to rely on credit cards or drain all savings.

1.1 The four numbers that matter most

- Your monthly housing payment: principal, interest, property taxes, homeowners insurance, mortgage insurance, and HOA dues if applicable.

- Your debt-to-income ratio: the share of gross monthly income used for the mortgage and other recurring debts.

- Your cash to close: down payment plus closing costs, prepaid taxes, insurance, and escrow deposits.

- Your post-closing cushion: emergency savings and maintenance money left after you buy.

2. How Home Affordability Works

A home affordability estimate starts with a target monthly payment and works backward to a realistic purchase price. The same income can support different home prices depending on interest rates, taxes, insurance, loan type, debts, credit score, and down payment.

2.1 The basic affordability formula

A simplified way to estimate affordability is:

Affordability formula Affordable home price depends on: affordable monthly housing payment + down payment - estimated taxes, insurance, mortgage insurance, HOA dues, closing costs, and loan costs.

Because taxes, insurance, and loan terms vary by location and borrower, no single salary-to-home-price rule works for everyone. Two buyers with the same income can have very different budgets if one has student loans, a car payment, high property taxes, or a smaller down payment.

2.2 What lenders usually review

- Income: salary, wages, bonuses, commissions, self-employment income, retirement income, or other documented income.

- Debts: credit cards, auto loans, student loans, personal loans, alimony or child support obligations, and other recurring debts.

- Credit profile: credit score, payment history, credit utilization, collections, and recent credit inquiries.

- Assets: checking, savings, retirement accounts, gift funds, and reserves after closing.

- Property details: appraised value, property taxes, insurance, HOA dues, property condition, and loan eligibility.

CFPB guidance encourages buyers to compare Loan Estimates from different lenders because the Loan Estimate shows important loan terms and estimated costs. The CFPB also explains that Closing Disclosure settlement costs are the upfront costs charged to get the loan and transfer ownership. Sources are listed at the end of this document.

3. Why Home Affordability Matters

Affordability matters because a home is usually the largest monthly bill in a household budget. A home that looks affordable on paper can become stressful when repairs, taxes, insurance, utilities, commuting costs, and lifestyle expenses are ignored.

3.1 Benefits of calculating affordability before house hunting

- You avoid shopping above your true comfort zone.

- You know whether to save more, pay down debt, or improve credit before applying.

- You can compare loan options without focusing only on the lowest monthly payment.

- You reduce the risk of becoming house poor.

- You negotiate with clearer limits and fewer emotional decisions.

4. The Main Costs Included in Home Affordability

| Cost | What it means | Why it affects affordability |

|---|---|---|

| Principal | The part of your payment that repays the amount borrowed. | Higher loan amounts increase the monthly payment. |

| Interest | The cost of borrowing money. | A higher rate can reduce the home price you can afford even if your income stays the same. |

| Property taxes | Local taxes based on the property and location. | Taxes can vary widely by city, county, and home value. |

| Homeowners insurance | Coverage for damage, liability, and other risks. | Premiums can be higher in areas exposed to storms, wildfire, theft, or other risks. |

| Mortgage insurance | Usually required on many low-down-payment loans. | Adds to the monthly payment and may also involve upfront premiums on some loan types. |

| HOA dues | Fees charged by a homeowners association or condo association. | They count as a housing cost and reduce the mortgage payment you can support. |

| Closing costs | Upfront charges for the loan and property transfer. | They increase the cash needed to buy and can reduce your down payment or reserves. |

| Maintenance and repairs | Ongoing upkeep after purchase. | Not usually in lender ratios, but essential for real-life affordability. |

5. Debt-to-Income Ratio: The Lender’s Affordability Lens

Debt-to-income ratio, or DTI, compares recurring monthly debt payments with gross monthly income. It is one of the most important mortgage approval measures.

5.1 Front-end DTI

Front-end DTI measures only housing costs. It typically includes principal, interest, taxes, insurance, mortgage insurance, and HOA dues.

5.2 Back-end DTI

Back-end DTI includes the proposed housing payment plus other monthly debts such as car loans, student loans, credit cards, and personal loans.

DTI formula DTI = total monthly debt payments ÷ gross monthly income x 100

For example, if your gross monthly income is $7,000 and your total monthly debts after buying would be $2,520, your back-end DTI would be 36%.

5.3 Common DTI guidelines and why they are not absolute

Many buyer education resources mention the 28/36 guideline: try to keep housing costs near 28% of gross income and total debts near 36%. This is a helpful starting point, not a law. Some loan programs and automated underwriting systems may allow higher ratios when the borrower has strong credit, savings, stable income, or a larger down payment. Fannie Mae’s public Selling Guide states that manually underwritten loans generally have a 36% maximum total DTI, with possible flexibility up to 45% for certain borrowers, while Desktop Underwriter may allow up to 50%. Freddie Mac guidance describes 36% as a guideline and requires additional evaluation above that level.

The practical lesson: approval is not the same as comfort. A borrower approved at a high DTI may still feel financially squeezed if other living costs are high.

| Ratio or rule | What it means | Best use |

|---|---|---|

| 28% housing guideline | Housing payment is about 28% of gross monthly income. | Conservative benchmark for comfort and savings flexibility. |

| 36% total debt guideline | Mortgage plus other debts are about 36% of gross income. | Useful starting point for buyers with normal expenses. |

| 43% historic QM benchmark | A widely known mortgage threshold; current QM rules have evolved from a strict DTI test. | Helpful risk reference, but not the only underwriting standard. |

| 45% to 50% range | Sometimes possible with strong borrower profile or automated approval. | Use cautiously; stress-test your budget before accepting. |

6. Step-by-Step: How to Calculate How Much House You Can Afford

- Start with monthly gross income. Add stable income that can be documented. Do not rely on uncertain bonuses or side income unless a lender is likely to count it and you are comfortable depending on it.

- List recurring monthly debts. Include minimum credit card payments, student loans, car loans, personal loans, and other required payments.

- Choose a target total DTI. A conservative buyer may use 36%. A buyer with strong savings and low lifestyle costs may consider a higher number, but should stress-test it.

- Calculate your maximum total debt payment. Multiply gross monthly income by the target DTI.

- Subtract non-housing debts. The remainder is the maximum monthly housing payment under that target.

- Estimate taxes, insurance, PMI, HOA dues, and maintenance. These costs reduce the amount available for principal and interest.

- Estimate the loan amount supported by the remaining principal-and-interest budget. Mortgage calculators can do this quickly.

- Add your down payment to estimate purchase price, then subtract a margin for closing costs, repairs, moving, and reserves.

- Compare the result with your real monthly budget using take-home pay. If it feels tight, lower the target price.

- Get preapproved and compare Loan Estimates from multiple lenders before making an offer.

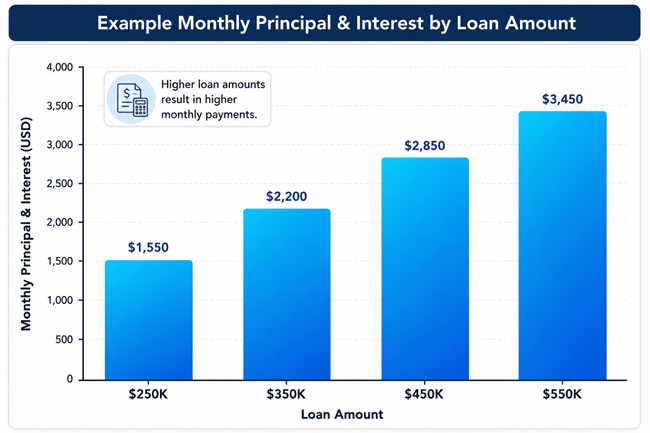

7. Example: Calculating an Affordable Home Price

Assume a buyer has gross monthly income of $8,000, other monthly debts of $700, and wants to keep total debt near 36% of gross income.

| Step | Calculation | Result |

|---|---|---|

| Target total debt payment | $8,000 x 36% | $2,880 |

| Subtract other debts | $2,880 - $700 | $2,180 available for housing |

| Estimate taxes, insurance, PMI, HOA | $2,180 - $650 | $1,530 available for principal and interest |

| Estimate loan amount | Based on a 30-year fixed loan at an example rate | The supported loan amount changes when rates change |

| Add down payment | Loan amount + buyer cash down | Estimated purchase price before closing-cost adjustment |

This example shows why the home price is not the first number to calculate. The safer starting point is the monthly payment that fits the buyer’s real life.

This simplified illustration shows principal and interest only. Taxes, insurance, mortgage insurance, HOA dues, and closing costs are not included and can materially change affordability.

8. Home Affordability by Income: Example Table

The table below is educational, not a quote or approval. It uses a simplified target housing payment of 28% of gross income. Actual affordability depends on debts, rates, taxes, insurance, credit, location, loan type, and savings.

| Annual gross income | Monthly gross income | 28% housing payment guideline | What to remember |

|---|---|---|---|

| $60,000 | $5,000 | $1,400 | Could be tight in high-tax or high-insurance areas. |

| $80,000 | $6,667 | $1,867 | Other debt strongly affects the comfortable price range. |

| $100,000 | $8,333 | $2,333 | Higher savings can improve options, but repairs and lifestyle still matter. |

| $125,000 | $10,417 | $2,917 | A larger payment may still be risky if income is variable. |

| $150,000 | $12,500 | $3,500 | Do not ignore taxes, HOA dues, insurance, and maintenance. |

9. Down Payment and Cash Needed to Buy

Your down payment affects your loan amount, monthly payment, mortgage insurance, and cash reserves. A larger down payment can improve affordability, but using every dollar for the down payment can create a fragile situation after closing.

| Down payment choice | Potential benefit | Potential trade-off |

|---|---|---|

| Low down payment | Lets you buy sooner and keep more cash available. | Higher loan amount, possible mortgage insurance, and higher monthly payment. |

| 20% down | Can help avoid private mortgage insurance on many conventional loans. | Requires more cash and may delay buying. |

| Very large down payment | Lower payment and less interest over time. | May leave too little cash for repairs, emergencies, or furnishing. |

9.1 Closing costs and prepaid expenses

Closing costs are separate from the down payment. They can include lender fees, title-related charges, appraisal fees, recording charges, prepaid interest, property taxes, initial escrow deposits, and insurance. The CFPB’s Loan Estimate and Closing Disclosure tools are designed to help buyers understand and compare these costs.

10. Loan Type and Affordability

| Loan type | How it may affect affordability | Important caution |

|---|---|---|

| Conventional loan | May offer strong pricing for borrowers with solid credit and larger down payments. | Low down payment conventional loans may require private mortgage insurance. |

| FHA loan | May help buyers with lower credit scores or smaller down payments qualify. | Mortgage insurance costs can affect monthly affordability and long-term cost. |

| VA loan | Eligible borrowers may be able to buy with no VA-required down payment and no PMI. | A VA funding fee may apply unless the borrower is exempt. Lenders still review income, credit, and occupancy requirements. |

| USDA loan | May help eligible rural or suburban buyers with low or no down payment. | Property location and household income eligibility rules apply. |

| Adjustable-rate mortgage | May start with a lower initial rate than a fixed-rate loan. | Payment can rise later; affordability should be stress-tested at future possible payments. |

11. Preapproval vs Personal Affordability

A mortgage preapproval estimates how much a lender may be willing to lend based on the information reviewed. It can help when making an offer, but it should not replace your own budget.

| Question | Preapproval answers | Personal affordability answers |

|---|---|---|

| Main focus | Can the lender approve this loan? | Can I live comfortably with this payment? |

| Uses gross or net income? | Usually gross income for ratios. | Take-home pay and real spending matter more. |

| Includes lifestyle costs? | Usually limited. | Yes: food, travel, childcare, medical, hobbies, savings, repairs. |

| Best use | Offer strength and loan planning. | Avoiding stress and long-term regret. |

12. Real-World Scenarios

12.1 Scenario 1: The buyer with strong income but high debt

A buyer earns a good salary but has a car loan, student loan, and credit card balances. Even if the buyer’s income looks strong, the back-end DTI may leave less room for housing. Paying down high-interest debt before buying could increase affordability and reduce stress.

12.2 Scenario 2: The renter with low debt but limited savings

A renter has almost no debt and can handle the monthly payment, but only has enough cash for the down payment. This buyer may need to wait, save more, negotiate seller credits if appropriate, or choose a lower price so closing costs and emergency reserves are not wiped out.

12.3 Scenario 3: The family choosing between two homes

One home has a lower price but high property taxes and HOA dues. Another costs more but has lower ongoing costs. The cheaper listing may not be the cheaper monthly payment. Affordability should compare total monthly ownership cost, not just price.

12.4 Scenario 4: The buyer with variable income

A commission-based or self-employed buyer may qualify using documented income, but comfort depends on income stability. A safer approach is to calculate affordability using a conservative income average and maintain larger cash reserves.

13. Pros and Cons of Buying at the Top of Your Approved Budget

| Pros | Cons |

|---|---|

| You may access a better location, school district, commute, or property condition. | You may have less money for savings, repairs, retirement, travel, or emergencies. |

| You may avoid moving again soon if the home fits long-term needs. | A job loss, medical bill, insurance increase, or tax increase can create stress. |

| You may benefit if your income rises and the payment becomes easier over time. | If income does not rise, you may feel house poor for years. |

| You may reduce compromises in a competitive housing market. | You may be more vulnerable to maintenance surprises and high-interest debt. |

14. Expert Tips for Safer Home Affordability

- Use both lender math and household budget math. Lender approval is a starting point, not a spending target.

- Stress-test the payment. Ask whether you could still pay if insurance, taxes, repairs, or childcare increased.

- Keep a separate emergency fund after closing. Do not confuse “cash to close” with “all the cash you need.”

- Compare at least a few Loan Estimates. Rate, points, lender credits, closing costs, and mortgage insurance can change the total cost.

- Avoid using the maximum approval amount as your search filter. Search below your limit so you have room for competition, repairs, and negotiation.

- For condos or HOA properties, review dues, reserves, special assessments, and rules carefully.

- Do not assume refinancing will solve affordability. Future rates and qualification are uncertain.

- Ask for a full monthly payment estimate, including taxes, insurance, PMI, HOA dues, and escrow assumptions.

15. Common Mistakes to Avoid

- Shopping by home price instead of monthly payment.

- Ignoring property taxes, insurance, HOA dues, and mortgage insurance.

- Draining all savings for the down payment.

- Assuming a lender’s maximum approval equals a safe personal budget.

- Forgetting closing costs, prepaid items, moving costs, furnishings, and immediate repairs.

- Using optimistic income instead of stable documented income.

- Taking on new debt before closing, which can affect approval.

- Not comparing lenders or reviewing the Loan Estimate carefully.

- Buying a home that leaves no room for life changes.

- Underestimating maintenance costs, especially for older homes.

16. Quick Action Checklist

- Calculate gross monthly income and take-home pay.

- List every recurring monthly debt payment.

- Choose a target housing payment you can live with comfortably.

- Estimate property taxes, homeowners insurance, mortgage insurance, and HOA dues.

- Estimate closing costs and prepaid expenses.

- Decide how much cash must remain after closing.

- Check your credit reports and correct errors before applying.

- Compare loan types that fit your situation.

- Get preapproved before serious house hunting.

- Request and compare Loan Estimates from multiple lenders.

- Walk away from homes that make the budget fragile.

17. Frequently Asked Questions

17.1 How much house can I afford?

You can afford the house that fits your monthly payment, upfront cash, debt level, savings goals, and emergency cushion. Start with a comfortable monthly housing payment, subtract taxes, insurance, PMI, and HOA dues, then estimate the loan amount and purchase price.

17.2 How much mortgage can I afford based on income?

A common starting point is to keep housing costs around 28% of gross income and total debts around 36%, but your safe number may be lower or higher depending on debts, taxes, insurance, savings, and income stability.

17.3 Is the 28/36 rule still useful?

Yes, as a conservative benchmark. It is not a strict lending rule, but it helps buyers avoid overcommitting. In expensive markets, some buyers exceed it, but they should stress-test their budget carefully.

17.4 What is the difference between what I can afford and what I can get approved for?

Approval is the lender’s risk decision. Affordability is your real-life cash-flow decision. You may be approved for more than you should comfortably spend.

17.5 Should I calculate affordability using gross income or net income?

Lenders often use gross income for DTI ratios. For your personal budget, also use take-home pay because taxes, retirement contributions, insurance, and payroll deductions affect what you can actually spend.

17.6 How does my down payment affect affordability?

A larger down payment usually lowers the loan amount and monthly payment. It may also reduce or eliminate mortgage insurance on some loans. But using all savings for the down payment can be risky.

17.7 Do property taxes affect how much house I can afford?

Yes. Higher property taxes increase the monthly housing payment and reduce the loan amount you can comfortably support.

17.8 Does homeowners insurance affect affordability?

Yes. Insurance premiums are part of the monthly cost of owning a home. In higher-risk areas, premiums can materially reduce affordability.

17.9 How much should I save after buying a house?

Keep enough emergency savings and repair funds so that a job disruption, medical bill, appliance failure, or urgent home repair does not force you into expensive debt.

17.10 Can I afford a house with student loans?

Possibly. Student loans count in your debt-to-income ratio. Your affordability depends on income, monthly debt payments, credit, savings, and the estimated housing payment.

17.11 Can I buy a house if I have credit card debt?

Yes, but credit card debt can reduce affordability and affect credit score. Paying down high-interest balances may improve both monthly cash flow and loan options.

17.12 Is a bigger down payment always better?

Not always. A bigger down payment can lower the payment, but keeping cash reserves may be more valuable than slightly reducing the loan amount.

17.13 Should I buy less house than I qualify for?

Often, yes. Buying below the maximum approval can leave room for savings, repairs, life changes, and financial peace of mind.

17.14 How do mortgage rates affect affordability?

Higher mortgage rates increase monthly principal and interest. When rates rise, the same monthly payment supports a smaller loan amount.

17.15 What should I do if I cannot afford homes in my target area?

Consider saving longer, paying down debt, improving credit, expanding the search area, choosing a smaller home, comparing loan programs, or waiting until your income and savings improve.

18. Conclusion

The best answer to “How much house can I afford?” is not the largest number a calculator or lender gives you. It is the home price that lets you make the payment, maintain the property, keep emergency savings, handle normal life expenses, and continue building financial security.

Use lender guidelines, DTI ratios, and preapproval as helpful tools, but make the final decision with your own budget. Compare total monthly ownership costs, protect your cash reserves, and avoid stretching so far that homeownership becomes a source of constant stress.

A well-chosen home should support your life, not consume it. The smartest purchase is usually the one that gives you both a place to live and enough financial breathing room to enjoy it.

18.1 Sources Consulted

- Consumer Financial Protection Bureau (CFPB), “Decide how much you want to spend on a home” and Loan Estimate/Closing Disclosure explainers: https://www.consumerfinance.gov/owning-a-home/

- CFPB Regulation Z, ability-to-repay and qualified mortgage standards: https://www.consumerfinance.gov/rules-policy/regulations/1026/43

- Fannie Mae Selling Guide, Debt-to-Income Ratios: https://selling-guide.fanniemae.com/sel/b3-6-02/debt-income-ratios

- Freddie Mac Single-Family Seller/Servicer Guide, DTI guidance: https://guide.freddiemac.com/

- U.S. Department of Housing and Urban Development (HUD/FHA), FHA lender and mortgagee letter resources: https://www.hud.gov/

- U.S. Department of Veterans Affairs (VA), VA home loan eligibility and funding fee information: https://www.va.gov/housing-assistance/home-loans/

- Federal Housing Finance Agency (FHFA), conforming loan limit values: https://www.fhfa.gov/data/conforming-loan-limit

Reader Advice: This article is written for educational purpose only and should not be taken as personalized financial, legal, tax, or mortgage advice. Mortgage rules, lender overlays, interest rates, assistance programs, and eligibility standards can change. Always verify details with licensed mortgage professionals, official program sources, and your lender before making a home-buying decision. Borrowers should compare current lender offers and consult qualified professionals before making a decision.