How to Improve Your Credit Score Before Applying for a Mortgage

Your credit score can affect whether you qualify for a mortgage, how much you may need to bring to closing, and the interest rate a lender offers. For a first-time homebuyer, even a small misunderstanding about credit can lead to avoidable stress: applying too early, disputing the wrong item at the wrong time, opening a new card before closing, or assuming a free educational score is the same score a mortgage lender will use.

Improving credit before a mortgage is not about gaming the system. It is about making your credit reports more accurate, your debt load easier to approve, and your payment history more reliable. Lenders want evidence that you can repay a large long-term loan on time. Your credit report is one of the main records they use to judge that risk.

This guide is for anyone planning to buy a home in the next few months to the next two years, especially borrowers with high credit card balances, limited credit history, past late payments, collections, student loans, or uncertainty about which mortgage credit score matters. It explains what to do first, what to avoid, what can work quickly, and what usually takes time.

The most important mindset is simple: start early, verify the data, lower risky balances, pay on time, avoid unnecessary new credit, and talk to a reputable mortgage professional before making major credit moves close to application.

1. What Does It Mean to Improve Your Credit Score Before a Mortgage?

Improving your credit score before applying for a mortgage means taking deliberate steps to make your credit reports show lower risk to lenders. These steps can include correcting inaccurate information, paying every bill on time, reducing revolving balances, avoiding unnecessary hard inquiries, and keeping your accounts stable before pre-approval and closing.

A credit score is a prediction of credit behavior based on information in your credit reports. The Consumer Financial Protection Bureau explains that companies use credit scores to help decide whether to offer credit and what interest rate or credit limit to provide. Mortgage lenders use credit scores alongside income, assets, debt-to-income ratio, down payment, property type, and loan program rules.

| Term | Plain-English meaning | Why it matters for a mortgage |

|---|---|---|

| Credit report | A detailed record of your credit accounts, balances, payment history, inquiries, and public-record credit items. | Your score is calculated from report data, so report errors can hurt approval or pricing. |

| Credit score | A number generated from credit report information to estimate repayment risk. | Higher scores can improve approval odds and may qualify you for better rates or lower mortgage insurance costs. |

| Mortgage credit score | The score model or set of scores used by mortgage lenders. | The score you see in a banking app may differ from the score used for mortgage underwriting. |

| Credit utilization | How much revolving credit you use compared with your limits. | High card balances can lower scores and increase perceived risk. |

| Hard inquiry | A lender credit check after you apply for credit. | Too many unrelated new-credit inquiries can hurt scores and raise lender questions. |

| Debt-to-income ratio | Monthly debt payments compared with gross monthly income. | Paying down debt can improve both credit scores and mortgage affordability. |

2. How Credit Scores Work in Mortgage Lending

Mortgage underwriting does not rely on one magic number. A lender reviews credit scores, full credit reports, income documentation, assets, existing debts, property details, and the specific loan program. The credit score still matters because it can influence eligibility, interest-rate pricing, and mortgage insurance costs.

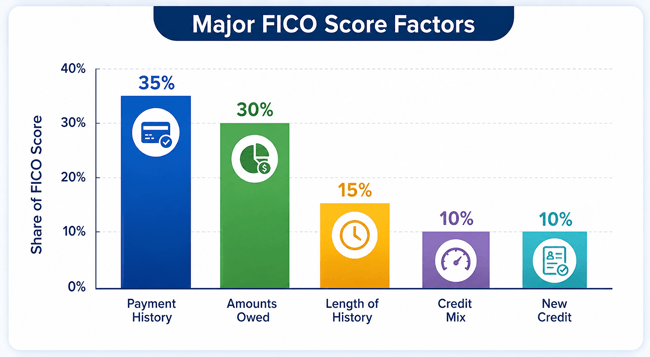

2.1 The main FICO score factors

FICO identifies five major scoring categories: payment history, amounts owed, length of credit history, credit mix, and new credit. These categories explain why the most effective mortgage-preparation moves are usually paying on time, reducing card balances, and avoiding unnecessary new accounts.

Figure: Major FICO Score factors. Source: FICO educational materials.

| FICO factor | Typical weight | Mortgage-prep action |

|---|---|---|

| Payment history | 35% | Set autopay, catch up past-due accounts, and avoid any late payment before closing. |

| Amounts owed | 30% | Pay down revolving balances and avoid running cards up before lender pulls credit again. |

| Length of credit history | 15% | Avoid closing old accounts without a clear reason before applying. |

| Credit mix | 10% | Do not open credit just to create a mix; stability matters more. |

| New credit | 10% | Avoid unnecessary applications for cards, auto loans, personal loans, or store financing. |

2.2 Why mortgage scores may differ from the score you see online

Many free credit score tools are useful for monitoring trends, but they may use a different score model from a mortgage lender. Mortgage lenders commonly evaluate scores from the major credit bureaus and follow investor or agency rules for selecting a representative score. For example, Fannie Mae guidance explains that when three scores are obtained for a borrower, the middle score is selected; when two scores are obtained, the lower score is selected. If there are multiple borrowers, lenders may apply additional program-specific rules.

3. Why Your Credit Score Matters Before You Apply for a Mortgage

- Approval: Some loan programs have minimum credit requirements, and lenders may add stricter overlays.

- Interest rate: Higher scores generally represent lower credit risk and can help borrowers qualify for better pricing.

- Mortgage insurance: On many conventional loans, credit score can affect private mortgage insurance costs.

- Down payment options: FHA rules treat very low scores differently for minimum down payment eligibility.

- Negotiating power: A stronger profile may make it easier to compare lenders and loan options confidently.

- Stress reduction: Fixing report errors before a deadline is easier than trying to solve them during underwriting.

| Loan context | Credit-score issue to understand | Practical takeaway |

|---|---|---|

| Conventional mortgage | Automated underwriting and pricing can consider score, credit profile, LTV, DTI, reserves, and property factors. | A higher score may improve pricing and PMI, but the whole file matters. |

| FHA mortgage | HUD states borrowers are not eligible for FHA-insured financing if the minimum decision credit score is below 500; FHA down payment tiers often depend on score. | Borrowers with lower scores should discuss FHA options and lender overlays early. |

| Manual underwriting | Program rules may include explicit score thresholds and more documentation. | Do not assume approval from score alone; compensating factors matter. |

| No-score or thin-file borrowers | Some programs can evaluate nontraditional credit or automated options, but documentation is more important. | Build documented payment history and speak with lenders early. |

4. Step-by-Step: How to Improve Your Credit Score Before Applying for a Mortgage

4.1 Step 1: Check all three credit reports early

Start by reviewing your credit reports from Equifax, Experian, and TransUnion. AnnualCreditReport.com is the official site for free credit reports, and it currently notes that free weekly online credit reports are available from the three nationwide credit reporting companies. The FTC warns that AnnualCreditReport.com is the only authorized place to get the free reports you are entitled to under federal law.

- Check your name, addresses, Social Security number details, and employment references for mixed-file clues.

- Confirm every account belongs to you.

- Look for late payments that you believe are inaccurate.

- Verify balances and credit limits on revolving accounts.

- Review collections, charge-offs, bankruptcies, judgments, and liens carefully.

- Save PDF copies of reports before you dispute or apply.

4.2 Step 2: Identify errors that could affect mortgage approval

Not every typo is a mortgage emergency. Focus first on errors that could lower your score, increase your debt load, or make an underwriter question your file.

| High-priority error | Why it matters | What to gather |

|---|---|---|

| Account that is not yours | Could indicate mixed file or identity theft. | Identity documents, police/FTC identity theft report if fraud is suspected, account statements. |

| Payment marked late incorrectly | Payment history is the largest FICO factor. | Bank proof, creditor confirmation, payment receipts. |

| Balance reported too high | Can increase utilization and DTI concerns. | Recent statements, payoff confirmation, creditor letter. |

| Closed account reported as open with balance | Can inflate debt obligations. | Closure letter, zero-balance statement. |

| Duplicate collection | Can make credit look worse than it is. | Collection notices, original creditor statements. |

4.3 Step 3: Dispute inaccurate information the right way

If you find inaccurate or incomplete credit report information, dispute it with both the credit reporting company and the company that supplied the information. The CFPB and FTC both recommend providing supporting documentation and keeping copies of dispute letters and evidence. Do not dispute accurate negative information simply because you dislike it; frivolous or unsupported disputes may not help and can complicate mortgage underwriting.

- Circle or list the exact item you dispute.

- Explain clearly why it is inaccurate or incomplete.

- Attach copies of supporting documents, not originals.

- Send the dispute to the credit bureau and the furnishing company.

- Track dates, confirmation numbers, and responses.

- Share unresolved disputes with your loan officer before application if they remain open.

4.4 Step 4: Pay every bill on time from now through closing

Payment history carries the largest share of the FICO scoring formula. A new late payment before a mortgage application can be especially damaging because it is recent and may trigger lender questions. Your goal is not only to raise your score but to show the lender that your credit behavior is stable.

- Set minimum-payment autopay on every credit card and loan.

- Create calendar reminders three to five days before due dates.

- Keep a small checking buffer so autopay does not fail.

- Contact creditors immediately if a hardship makes on-time payment difficult.

- Avoid “I will pay it after closing” thinking. Underwriters may re-check credit before funding.

4.5 Step 5: Lower credit card utilization strategically

For many borrowers, reducing revolving credit card balances is one of the fastest legitimate ways to improve score potential. Utilization means the percentage of available revolving credit you are using. A card with a $900 balance and a $1,000 limit looks much riskier than a card with a $90 balance and a $1,000 limit.

| Strategy | When it helps | Caution |

|---|---|---|

| Pay down highest utilization cards first | When one or more cards are near the limit. | Do not drain emergency savings so much that closing costs become unsafe. |

| Pay before statement closing date | When balances report high even though you pay in full monthly. | Ask card issuer when the balance reports to bureaus. |

| Spread payoff across several maxed cards | When multiple cards are above comfortable utilization levels. | A lender may still count minimum payments in DTI until balances update. |

| Request a credit limit increase | When it does not require a hard inquiry and spending will not increase. | Do not request close to application without asking whether a hard inquiry will occur. |

4.6 Step 6: Avoid new credit before and during the mortgage process

A new credit card, auto loan, furniture financing plan, personal loan, or buy-now-pay-later account can create three problems: a hard inquiry, a new account that lowers average account age, and a new payment that affects debt-to-income ratio. Even if the score impact is modest, the underwriting paperwork can slow down approval.

From pre-approval through closing, avoid new credit unless your loan officer tells you it is safe. This includes “no-interest” furniture offers, appliance financing, store cards, auto loans, personal loans, and co-signing for someone else.

4.7 Step 7: Keep old accounts open unless there is a strong reason to close them

Closing a credit card can reduce your available credit and raise utilization. It may also affect credit history over time. If an old card has no annual fee and you can manage it responsibly, keeping it open may help preserve available credit. If a card has a high annual fee or tempts overspending, ask a lender or credit counselor before deciding.

4.8 Step 8: Handle collections, charge-offs, and past-due accounts carefully

Collections and charge-offs require caution because the best move depends on the loan program, account age, amount, whether the debt is valid, and how the creditor reports updates. Paying a valid collection may be necessary in some cases, but it may not instantly erase the history from your report. Before paying or settling large derogatory accounts close to mortgage application, ask your loan officer how the account affects your specific underwriting path.

- Validate that the debt is yours before paying a collector.

- Get settlement terms in writing.

- Do not ignore tax consequences of forgiven debt when applicable.

- Keep proof of payment or settlement.

- Ask whether the lender requires certain collections to be paid before closing.

4.9 Step 9: Consider becoming an authorized user only when it truly helps

Being added as an authorized user on a responsible person’s long-standing, low-balance credit card may help some thin-file borrowers. It can also hurt if the card has high utilization, missed payments, or a short history. Mortgage underwriting may also review whether the account reflects your own credit responsibility. Use this only with someone you trust completely and after asking a lender whether it is likely to help your profile.

4.10 Step 10: Build credit if your file is thin

If you have little or no credit history, improving your mortgage readiness may take longer. The goal is to create documented, responsible credit behavior without taking on risky debt.

- Use a secured credit card from a reputable bank or credit union and pay it in full monthly.

- Consider a small credit-builder loan only if fees are reasonable and payments fit your budget.

- Keep utilization low and payments automatic.

- Document rent, utility, phone, and insurance payments in case a lender can consider nontraditional credit.

- Avoid opening several accounts at once.

4.11 Step 11: Reduce debt-to-income pressure, not just the score

Credit score and debt-to-income ratio are separate, but they overlap. Paying down a credit card can help both utilization and monthly debt obligations. Paying off an installment loan may reduce DTI, but the score effect varies. Mortgage planning should focus on total approval strength, not score points alone.

| Debt move | Possible credit-score effect | Possible mortgage effect |

|---|---|---|

| Pay down credit cards | Often positive if utilization falls. | May reduce minimum payments and improve DTI. |

| Pay off car loan | Mixed; may help or have little score impact. | Can lower DTI if the monthly payment is removed. |

| Consolidate debt | May lower utilization but adds new credit and inquiry. | Can help or hurt depending on payment, timing, and underwriting. |

| Ignore student loan reporting | No score improvement. | Could cause DTI surprises if payment is misestimated. |

4.12 Step 12: Time your mortgage shopping correctly

Checking your own credit does not hurt your scores, according to the CFPB. Lender checks after a mortgage application are different because they are hard inquiries. Credit scoring models generally recognize rate shopping for the same type of loan within a limited window, but you should still organize your shopping and avoid unrelated credit applications at the same time.

5. Mortgage Credit Improvement Timeline

| Time before applying | Best actions | Avoid |

|---|---|---|

| 12+ months | Build payment history, resolve old credit problems, create savings, avoid high-risk debt. | Waiting until pre-approval to look at your reports. |

| 6-12 months | Dispute errors, reduce utilization, catch up accounts, plan debt payoff. | Opening several accounts to “build credit faster.” |

| 3-6 months | Pay down cards before statement dates, compare score trends, talk with a lender. | Making large unexplained deposits or taking new loans. |

| 30-90 days | Keep balances low, freeze new applications, gather documentation. | Closing cards, co-signing, furniture financing, or car shopping. |

| Pre-approval to closing | Maintain the same credit behavior, employment, assets, and debts. | Any new credit or missed payment without telling your loan officer. |

6. Real-World Examples

6.1 Example 1: High credit card balances before pre-approval

A borrower has three credit cards with balances close to their limits. They pay on time, but their score is weaker than expected. Instead of opening a new card, they use savings beyond their emergency fund to lower two cards before the statement closing dates. When updated balances report, their utilization looks less risky. Their lender also sees lower minimum payments, which may help DTI.

6.2 Example 2: A credit report shows a late payment that was not late

A buyer notices a student loan marked 30 days late, but bank records show the payment cleared on time. They dispute the item with the credit bureau and the loan servicer, include supporting documents, and keep copies. They also tell their loan officer about the dispute timeline before applying.

6.3 Example 3: Thin credit file and a future home purchase

A renter plans to buy in 18 months but has no credit card and only a small student loan. They open one secured card from a reputable issuer, use it for a small recurring bill, set autopay, and keep the balance low. They do not open multiple accounts. By the time they apply, they have a longer record of on-time payments.

6.4 Example 4: The risky furniture purchase

A buyer is pre-approved and then finances furniture for the future home. The new account adds a hard inquiry and monthly payment. Before closing, the lender re-checks credit and asks for documentation. In a tight approval, this could delay closing or change loan eligibility. The safer move is to wait until after the mortgage closes and funds.

7. Credit Improvement Strategies Compared

| Strategy | Speed | Best for | Risk level |

|---|---|---|---|

| Correcting true credit report errors | Medium; depends on dispute process | Inaccurate late payments, wrong accounts, duplicate debts | Low if accurate and documented |

| Paying down credit card balances | Often faster after balances update | High utilization borrowers | Low if it does not drain needed cash |

| Opening new credit | Slow and uncertain | Thin files with long timeline | Medium to high near mortgage application |

| Authorized user account | Sometimes fast | Thin files with trusted family support | Medium; can backfire |

| Credit repair company | Varies | People needing organization help | Medium; scams and unnecessary fees are common |

| Nonprofit credit counseling | Medium | Budgeting, debt management, hardship planning | Low to medium; ask how any plan affects mortgage timing |

8. Pros and Cons of Improving Credit Before Applying

| Pros | Cons or limits |

|---|---|

| May improve approval odds. | Some changes take months or years. |

| Can qualify you for better pricing. | Not every score increase changes the rate quote. |

| May reduce mortgage insurance costs on conventional loans. | Credit is only one part of underwriting. |

| Helps you catch identity theft or report errors early. | Disputes close to closing can require extra documentation. |

| Can reduce debt stress before homeownership. | Aggressive payoff can leave too little cash for closing and emergencies. |

9. Costs and Fees to Consider

Improving credit does not have to be expensive. Many important steps are free: checking your official credit reports, disputing inaccurate information, setting autopay, creating reminders, and paying down balances. Be cautious about paid services that promise fast score increases.

| Item | Typical cost issue | Worth considering? |

|---|---|---|

| Official credit reports | Free through AnnualCreditReport.com. | Yes. Start here. |

| Credit scores | Some are free; some mortgage-specific scores may require a paid product. | Useful if you understand the model may differ from lender scores. |

| Credit monitoring | Free or paid depending on service. | Helpful for alerts, not required for everyone. |

| Credit repair company | Fees vary; avoid companies that promise deletion of accurate information. | Only if you need help and choose carefully. |

| Nonprofit credit counseling | Often low-cost or free initial counseling. | Useful for debt stress or budgeting before buying. |

| Balance payoff | Uses cash that might otherwise fund down payment or reserves. | Balance payoff should be coordinated with mortgage cash needs. |

10. Risks and Common Mistakes to Avoid

10.1 Mistake 1: Applying for new credit right before closing

This is one of the most common mortgage-credit mistakes. A new account can change your score, debt-to-income ratio, required documentation, and underwriting approval.

10.2 Mistake 2: Disputing everything on your report

Only dispute information that is inaccurate or incomplete. Broad, unsupported disputes can waste time and may create underwriting complications.

10.3 Mistake 3: Closing old cards to “look responsible”

Closing a card can reduce available credit and increase utilization. Ask a mortgage professional before closing accounts shortly before applying.

10.4 Mistake 4: Paying collections without a plan

Paying a valid debt can be appropriate, but the timing and reporting effect matter. Get written terms and ask how the account affects your loan program.

10.5 Mistake 5: Confusing pre-qualification with full approval

A pre-qualification or early estimate may not include full underwriting. Continue protecting your credit until the loan closes.

10.6 Mistake 6: Draining savings to chase score points

A stronger score is helpful, but lenders also care about cash to close, reserves, and financial stability. Do not trade away your emergency cushion without understanding the mortgage impact.

11. Expert Tips for Mortgage Credit Readiness

- Pull reports before you shop for homes, not after you find one.

- Ask a lender which score model and reporting details matter for your loan path.

- Pay cards before statement closing dates if your reported balances are high.

- Keep written proof of every payoff, settlement, and dispute.

- Do not move debt around just to make it look smaller; underwriters review documents.

- Tell your loan officer before making any major financial move during underwriting.

- Focus on durable habits: on-time payments, low balances, stable accounts, and honest documentation.

12. Quick Action Checklist

- Request credit reports from Equifax, Experian, and TransUnion through AnnualCreditReport.com.

- Save copies of all three reports.

- List inaccurate, unfamiliar, duplicated, or outdated negative items.

- Dispute true errors with the credit bureau and the company that supplied the information.

- Set autopay for at least the minimum payment on every account.

- Pay down credit cards, prioritizing high-utilization accounts.

- Avoid new credit applications until after closing unless your loan officer approves.

- Do not close old credit cards without advice.

- Gather proof for paid collections, settlements, and student loan payment terms.

- Keep cash reserves for down payment, closing costs, repairs, and emergencies.

- Compare mortgage lenders within an organized shopping period.

- Maintain the same credit behavior from pre-approval through closing.

13. Frequently Asked Questions

13.1 What credit score do I need to buy a house?

It depends on the loan program, lender, down payment, and overall file. FHA-insured financing is not available below a 500 minimum decision credit score, while many conventional scenarios use automated underwriting or program-specific requirements. Higher scores generally improve pricing and options.

13.2 How fast can I improve my credit score before a mortgage?

Some actions can help after updated balances or corrections appear on your reports, while payment history and older negative items take longer. A realistic plan should start at least three to six months before applying, and earlier is better.

13.3 Does checking my own credit hurt my score?

No. The CFPB states that checking your own credit report or score does not affect your credit scores. This is considered a soft inquiry.

13.4 Should I pay off all credit cards before applying for a mortgage?

Not always. Paying down high balances often helps, but draining all cash can hurt your ability to cover down payment, closing costs, and reserves. Aim for low reported balances and strong cash readiness.

13.5 Should I close credit cards before applying?

Usually not without a specific reason. Closing cards can reduce available credit and raise utilization. Ask a loan officer before closing accounts near application.

13.6 Can I buy a car before closing on a house?

It is risky. A car loan can add a hard inquiry and a monthly payment that changes your approval. Wait until after closing unless your mortgage team confirms it is safe.

13.7 Do mortgage lenders use FICO or VantageScore?

Mortgage lending has historically relied heavily on specific FICO models, while the industry is transitioning toward updated score frameworks. Ask your lender which scores apply to your loan at the time you apply.

13.8 Will paying a collection improve my mortgage credit score?

It may help your underwriting situation, but it may not instantly remove the negative history or increase your score. The best action depends on the debt, reporting status, and loan program.

13.9 Is a credit repair company worth it before a mortgage?

Sometimes, but many tasks can be done yourself for free. Be wary of companies that promise to remove accurate negative information or demand payment for unrealistic results.

13.10 Can rent payments help my mortgage application?

Sometimes. Some newer scoring and underwriting approaches may consider rental payment data, and lenders may request rent verification for thin-file borrowers. Keep clear records of rent payments.

13.11 What is credit utilization?

Credit utilization is the share of your revolving credit limits that you are using. Lower utilization generally looks less risky than maxed-out cards.

13.12 Can one late payment stop me from getting a mortgage?

One late payment does not always stop approval, but a recent late payment can hurt your score and raise lender concerns. Be ready to document what happened and show stable payments since then.

13.13 Should I dispute credit report errors during mortgage underwriting?

If the error is serious, yes, but coordinate with your loan officer. Open disputes can require additional review, so timing matters.

13.14 How long should I avoid new credit before a mortgage?

A conservative approach is to avoid unnecessary new credit for at least three to six months before applying and from pre-approval through closing.

13.15 What is the best first step if my score is low?

Pull all three credit reports, identify the reasons your score is low, and prioritize on-time payments and lower revolving balances. Guessing without reviewing reports wastes time.

13.16 Sources Consulted

- Consumer Financial Protection Bureau (CFPB): credit scores, mortgage credit checks, and disputing credit report errors.

- AnnualCreditReport.com: official access point for free credit reports from Equifax, Experian, and TransUnion.

- Federal Trade Commission (FTC): warnings about free credit report sites and guidance on disputing report errors.

- FICO/myFICO: major FICO Score factor categories and educational score information.

- HUD/FHA: FHA Single Family Housing Policy Handbook and FHA minimum decision credit score guidance.

- Fannie Mae Selling Guide: representative credit score guidance and general mortgage credit-score requirements.

14. Conclusion: Build a Mortgage-Ready Credit Profile, Not Just a Higher Number

Improving your credit score before applying for a mortgage is one of the most practical ways to prepare for homeownership. The best approach is straightforward: check all three credit reports, correct real errors, pay every bill on time, reduce high credit card balances, avoid unnecessary new credit, and protect your financial stability until closing.

The warning is equally important: do not chase quick fixes that create bigger underwriting problems. Opening new accounts, disputing accurate information, draining savings, or financing purchases before closing can weaken an otherwise approvable mortgage file.

Start early, stay organized, document everything, and work with reputable professionals. A stronger credit profile can give you more choices, more confidence, and a better foundation for responsible homeownership.

14.1 Sources Consulted

These source links are included for editorial transparency. Readers should verify current loan-program requirements with a licensed mortgage professional because lender overlays and agency rules can change.

| Source | URL / topic |

|---|---|

| CFPB | consumerfinance.gov: What is a credit score; mortgage lender credit checks; disputing credit report errors. |

| AnnualCreditReport.com | annualcreditreport.com: official free credit report access from Equifax, Experian, and TransUnion. |

| FTC | consumer.ftc.gov: free credit reports and disputing errors on credit reports. |

| FICO / myFICO | myfico.com: what goes into FICO Scores and major score factor categories. |

| HUD / FHA | hud.gov: FHA Single Family Housing Policy Handbook and FHA minimum decision credit score guidance. |

| Fannie Mae Selling Guide | selling-guide.fanniemae.com: general credit score requirements and representative credit score rules. |

This article is educational and does not provide personalized financial, legal, tax, or mortgage advice. Mortgage rates, fees, loan programs, underwriting rules, and tax laws change. Borrowers should compare current lender offers and consult qualified professionals before making a decision.