How Mortgages Work

A mortgage is the loan most people use to buy a home. Instead of paying the full purchase price upfront, the borrower pays part of the price as a down payment and borrows the rest from a lender. The home serves as collateral, which means the lender can take legal action to recover the property if the borrower does not repay the loan as agreed.

Understanding how mortgages work matters because a mortgage is usually one of the largest financial commitments a household will ever make. The interest rate, loan term, fees, taxes, insurance, and repayment structure can affect your monthly budget for years. A loan that looks affordable on the surface may become stressful if you overlook closing costs, escrow changes, adjustable rates, maintenance, or the risk of buying more house than you can comfortably afford.

This guide is written for first-time homebuyers, homeowners considering refinancing, renters comparing buying versus renting, and anyone who wants to make smarter housing decisions. You do not need a finance background. The goal is to explain the moving parts in plain English so you can ask better questions, compare loan offers more confidently, and avoid costly beginner mistakes.

1. What Is a Mortgage?

A mortgage is a secured loan used to buy, refinance, or borrow against real estate. It is “secured” because the property is pledged as collateral for the debt. The borrower promises to repay the loan through scheduled payments, usually monthly, over a set period such as 15, 20, or 30 years.

In everyday language, people often use “mortgage” to mean both the home loan and the legal agreement that gives the lender a claim against the property if the borrower defaults. The borrower owns the home, but the lender has a security interest until the mortgage is paid off or otherwise satisfied.

Quick Answer: Definition

A mortgage is a loan used to finance real estate, where the property acts as collateral and the borrower repays the lender over time through payments that usually include principal, interest, taxes, insurance, and sometimes mortgage insurance.

2. The Main Parts of a Mortgage Payment

Most mortgage payments are built around four major components, commonly called PITI: principal, interest, taxes, and insurance. Some borrowers also pay mortgage insurance and homeowners association dues.

| Payment Component | What It Means | Why It Matters |

|---|---|---|

| Principal | The amount you borrowed and still owe. | Paying principal builds equity and reduces the loan balance. |

| Interest | The cost of borrowing money from the lender. | The interest rate heavily affects your monthly payment and total cost. |

| Property taxes | Local taxes charged by your city, county, or other taxing authority. | Often collected through escrow and may rise over time. |

| Homeowners insurance | Insurance that helps protect the home against covered losses. | Usually required by lenders and can change annually. |

| Mortgage insurance | Insurance that protects the lender if the borrower defaults. | Often required with low down payments or FHA loans. |

| HOA dues | Fees paid to a homeowners association, if applicable. | Usually not part of the mortgage payment, but affects affordability. |

3. How Mortgages Work Step by Step

A mortgage works by spreading the cost of a home over many years. The lender provides money to complete the purchase, and the borrower repays that money with interest. The process includes qualification, property review, legal documents, closing, monthly payments, and eventual payoff.

- You estimate what you can afford based on income, savings, debt, credit, and housing costs.

- You apply with a lender and provide documents such as income records, bank statements, tax information, and permission to check credit.

- The lender evaluates your ability to repay, including your credit history, debt-to-income ratio, employment or income stability, assets, and the property value.

- The lender issues loan disclosures that summarize rate, payment, closing costs, and loan terms.

- The property is appraised and title work is reviewed to help confirm value and legal ownership.

- If the loan is approved, you receive final documents before closing and review the exact costs and terms.

- At closing, you sign documents, pay required funds, and the loan proceeds are used to complete the home purchase.

- After closing, you make monthly payments. Part of each payment reduces the balance, and part pays interest and other required housing costs.

- Over time, you build equity as the loan balance falls and the home value may change.

- When the loan is paid off, refinanced, or the home is sold, the mortgage lien is released according to applicable procedures.

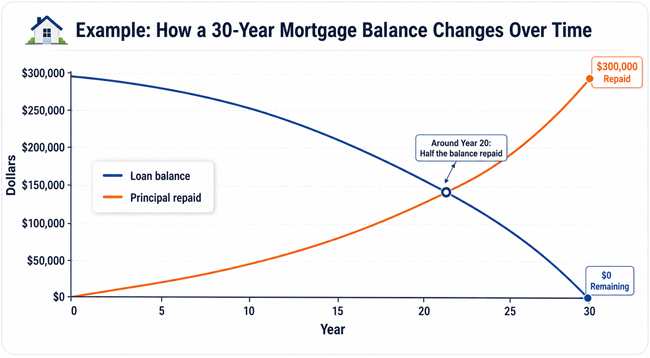

4. How Interest and Amortization Work

Mortgage interest is the price you pay to borrow money. With a typical repayment mortgage, your monthly payment is calculated so that the loan is fully paid off by the end of the term if you make every payment as scheduled. This repayment pattern is called amortization.

In the early years of a long-term mortgage, more of each payment usually goes toward interest because the outstanding loan balance is still high. Later, as the balance falls, more of each payment goes toward principal. This is why homeowners often feel that their loan balance goes down slowly at first.

Chart note: This illustration uses a hypothetical $300,000 mortgage at 6.5% for 30 years. It is for education only and does not include taxes, insurance, mortgage insurance, fees, or future rate changes.

5. Simple Mortgage Payment Example

| Example Item | Amount or Detail |

|---|---|

| Home purchase price | $375,000 |

| Down payment | $75,000 |

| Loan amount | $300,000 |

| Loan term | 30 years |

| Interest rate | 6.5% fixed, hypothetical |

| Principal and interest payment | About $1,896 per month |

| Other monthly costs | Property taxes, homeowners insurance, and possible mortgage insurance would be added separately |

This example shows why borrowers should not judge affordability by principal and interest alone. A realistic housing budget should include taxes, insurance, utilities, maintenance, association dues, and a cushion for emergencies.

6. Fixed-Rate vs Adjustable-Rate Mortgages

The interest-rate structure is one of the most important mortgage choices. The two broad categories are fixed-rate mortgages and adjustable-rate mortgages.

| Feature | Fixed-Rate Mortgage | Adjustable-Rate Mortgage (ARM) |

|---|---|---|

| Interest rate | Stays the same for the life of the loan. | May start fixed for an initial period, then adjust based on the loan terms. |

| Payment stability | More predictable principal and interest payment. | Payment can rise or fall after adjustment periods. |

| Best suited for | Borrowers who want long-term payment certainty. | Borrowers who understand rate risk or expect to sell/refinance before adjustments. |

| Main risk | Initial rate may be higher than some ARM introductory rates. | Future payment increases can strain the budget. |

| Key question | Can I comfortably afford this payment long term? | Can I afford the payment if the rate rises to the cap? |

The CFPB’s adjustable-rate mortgage materials emphasize that borrowers should understand how and when an ARM can change, including caps, indexes, margins, and worst-case payment scenarios. Never choose an ARM only because the first payment looks cheaper.

7. Common Types of Mortgage Loans

| Mortgage Type | How It Works | Common Use Case |

|---|---|---|

| Conventional mortgage | A mortgage not directly insured or guaranteed by a government agency. | Borrowers with solid credit, stable income, and enough savings for down payment and closing costs. |

| FHA loan | A loan insured by the Federal Housing Administration and offered through approved lenders. | Borrowers who may need more flexible credit or down payment options. |

| VA loan | A mortgage program for eligible service members, veterans, and certain surviving spouses. | Eligible military borrowers seeking favorable home financing terms. |

| USDA loan | A program for eligible rural and some suburban properties and borrowers. | Qualified buyers in eligible areas who meet program rules. |

| Jumbo loan | A larger mortgage that exceeds conforming loan limits. | Higher-priced homes requiring larger loan amounts. |

| Refinance mortgage | A new loan that replaces an existing mortgage. | Changing rate, term, loan type, or accessing home equity when appropriate. |

8. Why Mortgages Matter

A mortgage can make homeownership possible without requiring the buyer to save the full purchase price. But it also creates a long-term obligation. The right mortgage can support financial stability, while the wrong mortgage can create stress, reduce savings, or increase the risk of default.

- It affects your monthly cash flow for years.

- It determines how quickly you build equity through principal repayment.

- It influences your total cost of homeownership through interest and fees.

- It can limit or expand your future financial flexibility.

- It can expose you to foreclosure risk if payments become unaffordable.

9. Mortgage Costs and Fees to Understand

A mortgage is not free to set up. Costs vary by lender, loan type, location, property, and borrower profile. The CFPB explains that mortgage closing costs can include lender charges and third-party costs such as appraisal fees, credit report costs, title-related fees, and other settlement charges. Borrowers should compare official loan disclosures instead of relying only on advertised rates.

| Cost or Fee | What It Usually Covers | Smart Borrower Tip |

|---|---|---|

| Origination charge | Lender charge for processing or making the loan. | Compare both rate and fees, not one alone. |

| Appraisal fee | Professional estimate of the home’s value. | A low appraisal can affect approval or require renegotiation. |

| Credit report fee | Cost of obtaining credit reports. | Small fee, but still part of total closing costs. |

| Title search and title insurance | Checks ownership history and protects against certain title problems. | Review who pays which title costs in your market. |

| Prepaid taxes and insurance | Funds collected upfront for escrow or coverage periods. | Budget for these beyond the down payment. |

| Discount points | Optional upfront fee paid to reduce the rate. | Calculate the break-even period before buying points. |

| Mortgage insurance | Required on many low-down-payment loans. | Ask how it works and when it can be removed, if possible. |

10. What Is Escrow in a Mortgage?

Escrow is an account, often managed by the mortgage servicer, used to collect and pay certain property-related expenses such as property taxes and homeowners insurance. Instead of paying those bills separately once or twice a year, many borrowers pay a portion each month with the mortgage payment.

Escrow can make budgeting easier, but it does not freeze your taxes or insurance. If property taxes or insurance premiums rise, your required escrow payment may also rise. This is one reason a mortgage payment can change even when the loan has a fixed interest rate.

11. Mortgage Preapproval, Underwriting, and Closing

Before shopping seriously, many buyers seek mortgage preapproval. Preapproval is a lender’s conditional estimate of how much you may be able to borrow based on a review of your financial profile. It is not a final guarantee, because the property, documentation, underwriting, and final conditions still matter.

Underwriting is the lender’s deeper review of your loan application. The underwriter evaluates your ability to repay, the property value, title information, assets, liabilities, income, and compliance with loan rules. During this stage, the lender may ask for updated documents or explanations.

Closing is the final step where legal documents are signed, funds are exchanged, and the mortgage becomes active. The CFPB notes that the Closing Disclosure is designed to help borrowers double-check loan details before closing and is generally provided three business days before scheduled closing.

12. Benefits of Using a Mortgage

- You can buy a home without paying the full price upfront.

- You may build equity over time as you repay principal and if the property value holds or rises.

- Fixed-rate loans can provide predictable principal and interest payments.

- Homeownership may offer stability for families who plan to stay in one place.

- Mortgage products give borrowers different ways to match financing to their needs, risk tolerance, and eligibility.

13. Risks and Trade-Offs of Mortgages

- Foreclosure risk: If you cannot make payments, the lender may pursue foreclosure according to law and loan terms.

- Interest cost: A long loan term can create a large total interest cost over time.

- Payment shock: Adjustable-rate loans, escrow increases, insurance changes, or tax increases can raise payments.

- Negative equity risk: If home values fall, you could owe more than the home is worth.

- Liquidity risk: Homeownership can tie up cash that might otherwise be used for emergencies, retirement savings, or business needs.

- Maintenance risk: Repairs are the homeowner’s responsibility and can be expensive.

14. Real-World Mortgage Scenarios

14.1 Scenario 1: The first-time buyer choosing between two payments

Maria qualifies for a mortgage with a principal and interest payment of $1,900. But when she adds taxes, insurance, utilities, and maintenance savings, her realistic housing cost is closer to $2,600. Instead of maxing out her approval, she shops for a lower-priced home so she can keep an emergency fund.

14.2 Scenario 2: The borrower comparing a fixed rate and an ARM

David is offered a lower introductory payment on an ARM. He plans to keep the home for only three years, but his job is uncertain. He asks the lender to show the maximum possible payment after adjustments. When he sees the worst-case payment would strain his budget, he chooses the fixed-rate mortgage for stability.

14.3 Scenario 3: The homeowner thinking about refinancing

Aisha has an older mortgage and is considering refinancing to lower her rate. She compares the monthly savings with closing costs and calculates how long it would take to break even. Because she may sell in one year, refinancing may not save enough to justify the upfront cost.

15. Pros and Cons of Mortgages

| Pros | Cons |

|---|---|

| Makes homeownership possible without paying the full price upfront. | Creates a long-term debt obligation. |

| Can help build equity over time. | Interest and fees can substantially increase total cost. |

| Fixed-rate options provide payment predictability. | Taxes, insurance, and HOA costs can still rise. |

| Different loan programs may fit different borrower needs. | Default can lead to serious credit damage and possible foreclosure. |

| Can be refinanced if market conditions and borrower qualifications support it. | Refinancing has costs and may reset the repayment timeline. |

16. Common Mortgage Mistakes to Avoid

- Focusing only on the interest rate and ignoring fees, points, and closing costs.

- Borrowing the maximum amount approved instead of the amount that fits your real budget.

- Ignoring property taxes, insurance, maintenance, utilities, and HOA dues.

- Making large credit purchases before closing, which can affect approval.

- Choosing an ARM without understanding adjustment rules and maximum payment risk.

- Skipping comparison shopping with multiple lenders.

- Not reading the Loan Estimate and Closing Disclosure carefully.

- Assuming preapproval means final approval.

- Using all savings for the down payment and leaving no emergency fund.

- Refinancing without calculating total costs and break-even time.

17. Expert Tips for Smarter Mortgage Decisions

- Compare loans using annual percentage rate, interest rate, monthly payment, cash to close, and total loan costs.

- Ask every lender for the same loan scenario so comparisons are fair.

- Keep a separate home maintenance fund; the mortgage payment is not the full cost of owning a home.

- Review whether paying points makes sense based on how long you expect to keep the loan.

- Before choosing a low down payment loan, understand mortgage insurance costs and removal rules.

- Do not waive important protections or inspections simply to move faster unless you fully understand the risk.

- Keep documentation organized, especially if self-employed or earning variable income.

- Ask the lender to explain any term you do not understand before signing.

18. Quick Action Checklist

- Estimate your comfortable monthly housing budget, not just the maximum loan approval.

- Check your credit reports and correct errors before applying.

- Save for down payment, closing costs, moving costs, repairs, and emergencies.

- Compare at least three lender offers using the same loan amount and loan type.

- Review the Loan Estimate line by line and ask about fees you do not understand.

- Decide whether a fixed-rate or adjustable-rate loan fits your risk tolerance.

- Calculate the impact of taxes, insurance, mortgage insurance, and HOA dues.

- Avoid new debt or major financial changes during underwriting.

- Read the Closing Disclosure carefully before closing.

- After closing, set up on-time payments and review escrow changes each year.

19. Frequently Asked Questions About How Mortgages Work

How does a mortgage work in simple terms?

A mortgage lets you buy a home by borrowing money from a lender and repaying it over time. The home acts as collateral, and your payments usually include principal, interest, and often taxes and insurance.

What is included in a monthly mortgage payment?

A monthly mortgage payment commonly includes principal and interest. Many payments also include escrow for property taxes and homeowners insurance, plus mortgage insurance if required.

What is principal on a mortgage?

Principal is the amount of money you borrowed and still owe. Each principal payment reduces your loan balance and helps build equity.

What is mortgage interest?

Mortgage interest is the cost of borrowing money. It is calculated based on your loan balance, interest rate, and repayment schedule.

Why does more interest get paid at the beginning of a mortgage?

At the beginning, the loan balance is highest, so the interest portion of each payment is larger. As the balance falls, more of each payment goes toward principal.

What is amortization?

Amortization is the process of paying off a loan through scheduled payments over time. In a typical mortgage, each payment includes both interest and principal.

What is escrow?

Escrow is an account used to collect and pay expenses such as property taxes and homeowners insurance. It can help spread large annual bills into monthly payments.

Can a fixed-rate mortgage payment change?

Yes, the principal and interest portion stays the same, but the total payment can change if property taxes, homeowners insurance, mortgage insurance, or escrow requirements change.

What is the difference between prequalification and preapproval?

Prequalification is usually an early estimate based on limited information. Preapproval typically involves a deeper review of income, credit, assets, and debts, but it is still not a final loan guarantee.

How much down payment do I need for a mortgage?

The required down payment depends on the loan program, lender rules, borrower profile, property, and market. Some programs allow low down payments, while others require more. Always compare the total cost, not just the minimum down payment.

What are closing costs?

Closing costs are expenses paid to finalize the loan and real estate transaction. They may include lender charges, appraisal fees, title fees, prepaid taxes and insurance, and other settlement costs.

What is mortgage insurance?

Mortgage insurance protects the lender if the borrower defaults. It is commonly required for certain low-down-payment loans and for FHA loans.

Can I pay off my mortgage early?

Many borrowers can pay extra toward principal to reduce interest and shorten the loan term, but you should confirm whether your loan has any prepayment penalty and whether extra payments are applied correctly.

Is a 15-year mortgage better than a 30-year mortgage?

A 15-year mortgage usually pays off faster and may reduce total interest, but the monthly payment is higher. A 30-year mortgage usually has a lower monthly payment but can cost more interest over time.

What happens if I miss mortgage payments?

Missing payments can lead to late fees, credit damage, loss mitigation processes, and eventually foreclosure if the problem is not resolved. Contact the servicer early if you are struggling.

20. Conclusion: The Best Mortgage Is the One You Understand and Can Afford

A mortgage is more than a monthly payment. It is a long-term financial agreement that combines borrowed money, interest, collateral, legal documents, taxes, insurance, and risk. Understanding how mortgages work helps you compare offers, avoid surprises, and choose a loan that supports your life rather than stretching your finances too thin.

The most important best practices are simple: compare lenders, read official disclosures, understand the full monthly cost, keep an emergency fund, avoid borrowing the maximum just because you qualify, and ask questions before signing. A mortgage can be a powerful tool for buying a home and building stability, but it works best when the payment fits comfortably within a realistic financial plan.

21. Sources Consulted

- Consumer Financial Protection Bureau (CFPB), Loan Estimate Explainer: consumerfinance.gov/owning-a-home/loan-estimate/

- Consumer Financial Protection Bureau (CFPB), Mortgage Key Terms: consumerfinance.gov/consumer-tools/mortgages/answers/key-terms/

- Consumer Financial Protection Bureau (CFPB), Closing Disclosure Explainer: consumerfinance.gov/owning-a-home/closing-disclosure/

- Consumer Financial Protection Bureau (CFPB), Consumer Handbook on Adjustable-Rate Mortgages: files.consumerfinance.gov/f/documents/cfpb_charm_booklet.pdf

- U.S. Department of Housing and Urban Development (HUD), Single Family Mortgage Insurance Premiums: hud.gov/hud-partners/housing-mip

- Federal Reserve Board, Consumer Handbook on Adjustable Rate Mortgages: federalreserve.gov/pubs/arms/armstext_cover2005.pdf

Reader Advice: This article is written for educational purpose only and should not be taken as personalized financial, legal, tax, or mortgage advice. Mortgage rules, lender overlays, interest rates, assistance programs, and eligibility standards can change. Always verify details with licensed mortgage professionals, official program sources, and your lender before making a home-buying decision. Borrowers should compare current lender offers and consult qualified professionals before making a decision.