What Are Student Loans?

Student loans are one of the most important financial decisions many students and families make before, during, and after college. At their best, they help people access education, training, credentials, and career paths that may otherwise be out of reach. At their worst, they can create years of financial pressure when borrowers do not understand the terms, borrow too much, choose the wrong loan, or enter repayment without a plan.

This matters because education borrowing is different from using a credit card or taking a small personal loan. Student loans are tied to school costs, enrollment status, repayment rules, interest accrual, deferment options, credit history, and sometimes government protections. A beginner may see a loan offer and focus only on the amount available, but the real decision is broader: how much will the loan cost, when will repayment begin, what happens if income is low, and what protections exist if life changes?

This article is for students, parents, adult learners, graduate students, and anyone comparing education financing options. It is also for readers who feel overwhelmed by financial aid language and want plain-English answers before signing a loan agreement. You do not need prior financial knowledge to use this guide. By the end, you should understand what student loans are, how they work, what types exist, how to compare them, and how to reduce the chance of costly mistakes.

1. Student Loan Definition in Plain English

A student loan is a borrowing agreement designed to help pay for education. The lender gives money for approved school-related costs, and the borrower promises to repay it later. In most cases, repayment includes the original amount borrowed plus interest, which is the price charged for using the lender's money over time.

The word student loan can refer to federal loans made or backed by a government program, or private loans offered by banks, credit unions, online lenders, state agencies, schools, or other private institutions. The rules can be very different depending on the loan type.

A student loan is not free aid. Grants and scholarships usually do not have to be repaid if the student meets the requirements. Student loans generally must be repaid even if the borrower does not finish school, does not find a high-paying job, changes careers, or is unhappy with the education received.

2. What Student Loans Are Used For

Student loans are intended to cover education-related costs. Schools usually define the total estimated cost through a figure called cost of attendance. Cost of attendance may include direct school bills and other necessary expenses connected with enrollment.

Direct costs are charges paid to the school, such as tuition, mandatory fees, campus housing, and meal plans. Indirect costs are expenses the student may pay outside the school bill, such as books, transportation, off-campus rent, utilities, supplies, or basic technology required for study.

| Expense category | Can student loans usually help pay for it? | Beginner note |

|---|---|---|

| Tuition and required fees | Yes | Usually paid first from financial aid funds. |

| Books and supplies | Often yes | Keep receipts and avoid spending loan refunds on non-school items. |

| Housing and meals | Often yes | Included when reasonable and tied to school attendance. |

| Transportation | Often yes | May include commuting costs, not luxury travel. |

| Laptop or required technology | Sometimes yes | Must be education-related and reasonable. |

| Entertainment or vacations | No | Using loan money this way increases debt without improving education value. |

3. How Student Loans Work

Student loans follow a predictable life cycle. First, the student estimates education costs and applies for aid. Then the school or lender determines eligibility and offers loan options. The borrower accepts some or all of the loan, signs required documents, and the money is disbursed, often directly to the school. If funds remain after school charges are paid, the student may receive a refund for other approved education expenses.

The loan then enters an in-school period while the student is enrolled at least the required level, often half time for many federal student loans. Depending on the loan type, interest may or may not grow during school. After the student graduates, leaves school, or drops below the required enrollment level, a grace period or repayment trigger may begin. Eventually, regular payments become due.

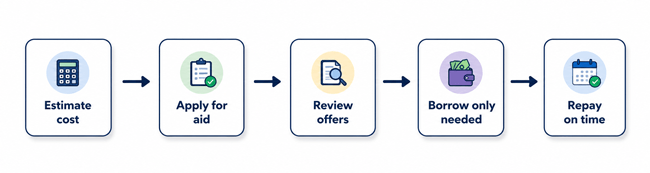

3.1 Student Loan Life Cycle: Step by Step

- Estimate the total cost of attendance, including tuition, fees, housing, books, transportation, and personal school-related expenses.

- Apply for financial aid through the required process, such as the FAFSA for U.S. federal aid, and check school-specific aid requirements.

- Review grants, scholarships, work-study, savings, family contributions, and payment plans before borrowing.

- Compare loan offers by total cost, interest rate, fees, repayment flexibility, and borrower protections.

- Accept only the amount needed, not automatically the full amount offered.

- Complete required loan documents, such as a promissory note and entrance counseling when applicable.

- Use funds only for education-related expenses and track how much has been borrowed each term.

- Prepare for repayment before leaving school by knowing the servicer, due date, repayment plan, and monthly payment estimate.

- Make payments on time, update contact information, and ask for help early if repayment becomes difficult.

4. Types of Student Loans

The two broad categories are federal student loans and private student loans. Federal loans generally have standardized rules and borrower protections. Private loans are lender-specific and often depend heavily on credit history, income, and co-signer strength.

4.1 Federal Student Loans

Federal student loans are education loans offered through government student aid programs. In the United States, current federal Direct Loan categories commonly include Direct Subsidized Loans, Direct Unsubsidized Loans, Direct PLUS Loans for parents or graduate/professional students, and Direct Consolidation Loans. Federal Student Aid explains that subsidized loans are generally available to eligible undergraduate students with financial need, while unsubsidized loans do not require demonstrated financial need.

Federal loans are often the first type of loan students should evaluate because they may offer fixed rates, standardized terms, income-related repayment options, deferment or forbearance options, and certain forgiveness or discharge protections when eligibility rules are met.

4.2 Private Student Loans

Private student loans are offered by private lenders such as banks, credit unions, online lenders, state-based lenders, and sometimes schools. They can help fill a funding gap after grants, scholarships, savings, work income, payment plans, and federal student loans have been considered.

Private loans usually involve underwriting. That means the lender may review credit score, income, debt, school, program, enrollment status, and sometimes the credit profile of a co-signer. Terms vary widely by lender, so comparing offers is essential.

| Loan type | Who it may serve | Key feature | Important caution |

|---|---|---|---|

| Direct Subsidized Loan | Eligible undergraduate students with financial need | Government may cover interest during certain periods | Availability and amount are limited by eligibility rules. |

| Direct Unsubsidized Loan | Undergraduate, graduate, and professional students depending on eligibility | No financial need requirement for eligibility | Interest can accrue while in school. |

| Direct PLUS Loan | Parents of dependent undergraduates and graduate/professional students | Can help cover remaining cost of attendance | May involve credit review and higher total borrowing risk. |

| Direct Consolidation Loan | Borrowers with eligible federal loans | Combines eligible federal loans into one federal loan | May affect repayment progress or benefits; review before consolidating. |

| Private Student Loan | Borrowers with remaining funding gaps | Lender-specific rates and terms | Fewer federal protections; co-signer may share repayment responsibility. |

5. Federal vs. Private Student Loans

For many borrowers, the federal vs. private student loan decision is the most important comparison. Neither option should be chosen blindly. The right choice depends on eligibility, cost, repayment flexibility, credit profile, degree program, family situation, and risk tolerance.

| Feature | Federal student loans | Private student loans |

|---|---|---|

| Lender/source | Government student aid program | Bank, credit union, online lender, state agency, or school-affiliated lender |

| Application path | Often starts with a government financial aid application and school aid office | Direct lender application or lender marketplace |

| Credit requirements | Some federal loans do not require traditional credit underwriting; PLUS loans may involve credit review | Usually credit-based; co-signer may be required |

| Interest rate | Generally fixed and set by law or government program rules for the loan period | Fixed or variable depending on lender and borrower qualifications |

| Repayment flexibility | May include income-related plans, deferment, forbearance, consolidation, and forgiveness options if eligible | Usually more limited and depends on lender policy |

| Co-signer risk | Generally not needed for many federal student loans | Common for students with limited credit or income |

| Best used when | Borrower qualifies and needs education financing after free aid | Borrower still has a responsible funding gap after safer options are reviewed |

6. Student Loan Costs: Principal, Interest, Fees, and Total Repayment

The amount borrowed is only the starting point. The true cost of a student loan is the total amount repaid over time. That total may include principal, interest, origination fees, late fees, returned payment fees, collection costs, and the opportunity cost of having future income committed to debt payments.

Interest is especially important because it can grow while a student is in school, during grace periods, or during payment pauses, depending on the loan type and rules. Some loans capitalize unpaid interest, meaning unpaid interest is added to the principal balance. After capitalization, future interest may be charged on a larger balance.

| Cost term | Plain-English meaning | Why it matters |

|---|---|---|

| Principal | The amount borrowed | The larger the principal, the more debt you must repay. |

| Interest rate | The percentage cost of borrowing | A higher rate increases total repayment cost. |

| Origination fee | A fee deducted from or added to the loan when made | You may receive less than you borrowed or repay more than expected. |

| Capitalization | Unpaid interest added to principal | Can increase the balance used to calculate future interest. |

| Late fee | Charge for missing or delaying payment | Adds cost and may signal credit risk. |

| Total repayment | All payments made over the loan life | Best measure for comparing loan choices. |

If a student borrows $8,000, the final amount repaid will usually be more than $8,000 if interest accrues. A lower interest rate, shorter repayment time, extra payments, and avoiding capitalization can reduce total cost.

7. Benefits of Student Loans

- Access to education when savings and free aid are not enough.

- Ability to invest in a degree, certificate, license, or training program.

- Potential to improve career options and long-term earning capacity.

- Flexible federal repayment options for eligible borrowers.

- Opportunity to build positive credit history by repaying on time.

- Ability to spread education costs over time instead of paying everything upfront.

8. Risks and Drawbacks of Student Loans

- Debt can follow the borrower for years after leaving school.

- Interest can increase the total amount repaid.

- Missed payments can harm credit and lead to fees or collection activity.

- Borrowing too much can delay goals such as renting independently, buying a home, saving, or starting a family.

- Private loans may offer fewer hardship protections than federal loans.

- A co-signer may become legally responsible if the borrower cannot pay.

- Loan obligations may remain even if the student does not complete the program.

| Pros | Cons |

|---|---|

| Can make education possible when cash is limited | Must generally be repaid with interest |

| May support career training and credentials | Can create long-term financial pressure |

| Federal loans may offer borrower protections | Rules can be confusing and change over time |

| On-time payments can support credit history | Missed payments can damage credit |

| Can bridge temporary funding gaps | Easy to overborrow if you accept the full offer |

9. Why Student Loans Matter for Financial Decisions

Student loans affect more than school enrollment. They influence future monthly cash flow, credit history, debt-to-income ratio, career flexibility, and emotional stress. A borrower who understands loan terms can make better decisions about school choice, program length, work during school, living costs, and repayment strategy.

The goal is not to scare students away from borrowing. The goal is to borrow with purpose. A reasonable loan used for a strong program with realistic career outcomes may be a useful investment. A large loan for an uncertain program, without a repayment plan, can become a serious burden.

10. Most Searched Student Loan Questions and Concepts

| Topic people search | What they really want to know |

|---|---|

| How do student loans work? | When money is received, when interest starts, and when repayment begins. |

| Federal vs private student loans | Which type is safer, cheaper, or more flexible. |

| Student loan interest | How borrowing cost grows over time. |

| Student loan forgiveness | Whether some borrowers can have debt canceled under specific rules. |

| Student loan repayment plans | How to choose a payment plan that fits income. |

| Co-signed student loans | What responsibility a co-signer accepts. |

| Student loans and credit score | How borrowing and repayment affect credit. |

| How much should I borrow? | How to avoid taking more debt than needed. |

11. Step-by-Step Process Before Taking a Student Loan

- Start with the school budget. Ask for the full cost of attendance, not just tuition.

- Subtract free aid first. Grants, scholarships, employer tuition assistance, and family help reduce the need to borrow.

- Estimate realistic income. Consider part-time work, internships, paid apprenticeships, or summer employment without harming academic progress.

- Compare schools and programs. A lower-cost accredited program may produce similar career value with less debt.

- Use federal options first when they are available and suitable. Federal loans often provide protections private loans do not match.

- Compare private loans only for the remaining gap. Review APR, fixed vs. variable rate, fees, co-signer terms, deferment options, and repayment support.

- Calculate future monthly payment. Do not wait until graduation to learn what repayment may feel like.

- Borrow by semester or year, not emotionally. Accept only what is needed for that period.

- Keep a loan tracker. Record lender, balance, rate, disbursement date, servicer, login, and repayment start date.

- Review annually. A decision that made sense in year one may not be best in year three.

12. Real-World Student Loan Examples

12.1 Example 1: The careful undergraduate borrower

Maria receives some scholarship aid, works part time, and still has a tuition gap. Instead of accepting the maximum loan offered, she calculates what she needs for tuition, books, and commuting. She borrows a smaller amount and keeps a spreadsheet of her balance. Potential outcome: she graduates with a more manageable payment because she controlled borrowing each year.

12.2 Example 2: The borrower who ignores living costs

Jamal focuses on tuition but forgets rent, utilities, food, and transportation. Midsemester, he relies on credit cards. A better approach would have been to create a full education budget, compare lower-cost housing, and discuss aid options with the financial aid office before borrowing or using high-interest debt.

12.3 Example 3: The private loan with a co-signer

Aisha needs funds after grants and federal loans. A private lender offers approval only with her uncle as co-signer. Before signing, they review whether the rate is fixed or variable, when payments begin, whether co-signer release is available, and what happens if Aisha cannot pay. Potential outcome: both borrower and co-signer understand the shared risk before accepting the loan.

12.4 Example 4: The graduate student comparing career payoff

David is considering a graduate program. He compares total program cost, expected borrowing, likely starting salary, licensing requirements, completion rate, and alternative schools. He decides that a slightly less expensive accredited program leaves more room in his budget after graduation. Potential outcome: the education goal stays intact while debt risk falls.

13. How Student Loan Repayment Works

Repayment begins according to the loan terms. Some loans have a grace period after leaving school; others may require payments immediately or interest-only payments while enrolled. Federal loan servicers and private lenders may provide online accounts showing balance, interest rate, due date, and payment options.

A repayment plan is the schedule that determines how monthly payments are calculated. Federal borrowers may have access to standard, graduated, extended, income-related, or other plans depending on current law and loan eligibility. Private loan repayment choices depend on the lender contract.

| Repayment approach | How it generally works | Best-fit scenario |

|---|---|---|

| Standard repayment | Fixed payments over a set term | Borrower wants predictable payments and faster payoff. |

| Graduated repayment | Payments start lower and increase over time | Borrower expects income to rise but understands later payments will be higher. |

| Income-related repayment | Payment is tied to income under eligible federal rules | Borrower needs affordability and qualifies under current program rules. |

| Extended repayment | Lower monthly payment over longer period | Borrower needs lower payment but may pay more interest over time. |

| Refinancing | New private loan replaces existing loans | Borrower has strong credit and understands potential loss of federal benefits. |

14. Common Student Loan Mistakes to Avoid

- Borrowing the full amount offered: Loan offers can exceed what you truly need. Build a term-by-term budget and decline unnecessary amounts.

- Ignoring interest while in school: Some loans accrue interest before repayment. Know whether interest grows during enrollment and grace periods.

- Choosing a school without comparing total cost: Compare net price, graduation requirements, accreditation, transfer credits, and career outcomes.

- Using loan refunds like income: Refunds are borrowed money. Spending them on lifestyle costs can create expensive future payments.

- Not reading the promissory note: The loan contract explains repayment responsibilities, interest, fees, and borrower obligations.

- Forgetting the co-signer: A co-signer is not just a reference. They may be legally responsible for payment.

- Missing servicer messages: Ignoring mail or email can lead to missed deadlines, lost options, or delinquency.

- Waiting too long to ask for help: Contact the servicer or financial aid office early if school costs or repayment become difficult.

15. Expert Tips for Borrowing Responsibly

- Use grants, scholarships, school aid, employer benefits, and savings before loans.

- Borrow for education value, not lifestyle upgrades.

- Estimate monthly payments before signing, not after graduation.

- Prefer fixed rates when predictability matters.

- Be cautious with variable-rate loans because payments or total cost may rise.

- Consider the likely salary range for your field, but do not rely on best-case income.

- Keep total student debt proportionate to realistic career earnings.

- Review official sources annually because federal rules and repayment options can change.

- Make small interest payments while in school if you can do so without harming basic needs.

- Use auto-pay only if your bank balance is reliable; overdraft fees can create new problems.

16. A Beginner-Friendly Decision Framework

1. Is this education path likely to improve my earning ability or career options?

2. Is this the lowest reasonable cost for the same credential or outcome?

3. Can I explain when repayment starts, what the payment may be, and what help exists if income is low?

| If your answer is... | What to do next |

|---|---|

| Yes to all three | Borrow carefully, document everything, and keep reviewing costs each term. |

| No to the cost question | Compare schools, commute options, transfer pathways, part-time schedules, and payment plans. |

| No to the repayment question | Pause and ask the financial aid office, servicer, or lender for written explanations. |

| No to the career-value question | Consider delaying enrollment, choosing a lower-cost path, or getting career counseling first. |

17. Alternatives to Student Loans

Student loans are sometimes necessary, but they should not be the first or only option. Reducing borrowing by even a small amount can lower future payments and interest costs.

- Grants and scholarships that do not normally require repayment.

- Work-study or part-time work that fits the academic schedule.

- Employer tuition reimbursement or apprenticeship programs.

- Community college transfer pathways.

- In-state public institutions when appropriate.

- Tuition payment plans offered by some schools.

- Living at home or reducing housing costs when practical.

- Used textbooks, open educational resources, and book rental programs.

- Taking a lighter course load only if it reduces costs without harming aid eligibility or completion timeline.

18. Student Loans and Credit Scores

Student loans can affect credit reports because they are debt accounts. On-time payments may support a positive payment history. Late payments, defaults, collections, or charge-offs can damage credit and make future borrowing more expensive. Private student loans may also require a credit check before approval, especially if the student lacks income or credit history.

19. What Happens If You Cannot Pay?

If repayment becomes difficult, the worst move is silence. Borrowers should contact the loan servicer or lender before missing payments. Depending on the loan type and current rules, options may include changing repayment plans, deferment, forbearance, temporary hardship programs, income-related payments, or other assistance. Private lenders may offer fewer options, so borrowers should ask about hardship policies before signing.

- Update your contact information so you do not miss notices.

- Ask for options in writing and save confirmation numbers or emails.

- Do not pay upfront fees to companies promising instant loan forgiveness.

- Use official government and servicer websites for federal loan actions.

- Get nonprofit credit counseling or legal help if you face collections or default.

20. Student Loan Glossary for Beginners

| Term | Meaning |

|---|---|

| Borrower | The person legally responsible for repaying the loan. |

| Co-signer | A person who agrees to repay the loan if the borrower does not. |

| Cost of attendance | The school estimate of total education costs for one academic year. |

| Disbursement | The release of loan funds, often to the school first. |

| Grace period | A limited time after leaving school before payments are due, if provided. |

| Interest | The cost of borrowing money. |

| Loan servicer | The company or organization that manages billing and repayment. |

| Promissory note | The legal document stating the borrower promises to repay. |

| Subsidized | A loan where the government may cover interest during certain periods. |

| Unsubsidized | A loan where the borrower is responsible for interest during all periods. |

21. Quick Action Checklist

- ☐ Ask the school for the full cost of attendance.

- ☐ Apply for grants, scholarships, and other free aid first.

- ☐ Compare net price across schools, not just tuition.

- ☐ Calculate the exact amount needed for the next term.

- ☐ Review federal student loan eligibility before private loans.

- ☐ Compare interest rates, fees, repayment terms, and borrower protections.

- ☐ Estimate monthly payments before accepting the loan.

- ☐ Borrow only what is needed for approved education costs.

- ☐ Keep a written loan tracker with balances and servicer details.

- ☐ Create a repayment plan before graduation or leaving school.

- ☐ Contact your servicer quickly if repayment becomes difficult.

22. Frequently Asked Questions About Student Loans

22.1 What are student loans?

Answer: Student loans are borrowed funds used to pay education-related expenses. They generally must be repaid with interest according to the loan agreement.

22.2 How do student loans work?

Answer: You apply, receive an offer, accept the amount needed, sign required documents, funds are disbursed, and repayment begins according to the loan terms.

22.3 Are student loans free money?

Answer: No. Student loans are debt. Grants and scholarships are usually closer to free aid because they often do not require repayment if requirements are met.

22.4 What is the difference between federal and private student loans?

Answer: Federal student loans are offered through government programs and may include more borrower protections. Private loans are offered by private lenders and vary by credit, income, co-signer, and lender rules.

22.5 Should I use federal or private student loans first?

Answer: Many borrowers review federal options first because they often include standardized protections and repayment flexibility. Private loans may be considered for remaining funding gaps.

22.6 Can student loans pay for rent?

Answer: They may be used for reasonable housing costs included in the school cost of attendance. Borrowers should avoid using loan money for unnecessary lifestyle expenses.

22.7 Do student loans affect credit?

Answer: Yes. Student loans can appear on credit reports. On-time payments can help payment history, while late payments can hurt credit.

22.8 When do student loan payments start?

Answer: It depends on the loan. Some loans offer an in-school period and grace period, while others may require immediate or interest-only payments.

22.9 What is student loan interest?

Answer: Interest is the cost of borrowing. It can increase the total amount repaid, especially if it accrues while in school or is capitalized.

22.10 What is a subsidized student loan?

Answer: A subsidized student loan is a loan where the government may pay interest during certain periods for eligible borrowers.

22.11 What is an unsubsidized student loan?

Answer: An unsubsidized student loan is a loan where the borrower is responsible for interest during all periods, including school and grace periods.

22.12 Can student loans be forgiven?

Answer: Some federal student loans may qualify for forgiveness, discharge, or cancellation under specific rules. Private student loan forgiveness is uncommon.

22.13 How much should I borrow for college?

Answer: Borrow only what is necessary after free aid, savings, income, and lower-cost choices are considered. Do not borrow the full amount just because it is offered.

22.14 Is a co-signer responsible for a student loan?

Answer: Yes. A co-signer generally shares legal responsibility for repayment if the borrower does not pay.

22.15 Can I pay student loans off early?

Answer: Many student loans allow early repayment, but borrowers should check their loan terms. Paying extra toward principal can reduce interest costs.

22.16 What happens if I miss student loan payments?

Answer: Consequences may include fees, credit damage, delinquency, default, collections, and loss of certain options. Contact the servicer or lender before missing payments.

22.17 Are student loans worth it?

Answer: They can be worth it when the education is affordable, the program is credible, the career path is realistic, and the debt is manageable. They are risky when borrowing is high and outcomes are uncertain.

23. Conclusion: Student Loans Can Help, But They Require a Plan

Student loans are education-focused debt. They can open the door to college, career training, graduate education, and professional credentials, but they also create repayment responsibilities that may last long after classes end. The smartest borrowers do not simply ask, 'Can I get this loan?' They ask, 'How much do I truly need, what will it cost, and how will I repay it?'

The best practice is to use free aid first, compare total school costs, understand the difference between federal and private loans, avoid unnecessary borrowing, and build a repayment plan before leaving school. If repayment becomes difficult, act early and use official help channels rather than ignoring the problem.

Used carefully, student loans can be a bridge to opportunity. Used casually, they can become a financial obstacle. A thoughtful borrower treats every loan dollar as future income already spoken for and borrows only when the education value justifies the cost.

23.1 Sources Consulted

Use these sources to verify current rules, programs, rates, eligibility, and borrower rights:

- Federal Student Aid, U.S. Department of Education - Subsidized and Unsubsidized Loans: https://studentaid.gov/understand-aid/types/loans/subsidized-unsubsidized

- Federal Student Aid, U.S. Department of Education - Federal Student Loan Interest Rates: https://studentaid.gov/understand-aid/types/loans/interest-rates

- Federal Student Aid, U.S. Department of Education - Repayment Plans: https://studentaid.gov/manage-loans/repayment/plans

- Consumer Financial Protection Bureau - Student Loans: https://www.consumerfinance.gov/consumer-tools/student-loans/

- U.S. Department of Education - Student loan updates and announcements: https://www.ed.gov/

- Your school financial aid office - for cost of attendance, aid eligibility, disbursement timing, and school-specific requirements.

Reader Advice: This guide is educational, not personalized financial, legal, or tax advice. Student loan rules, rates, fees, eligibility requirements, repayment programs, and forgiveness options can change. Always verify current details with official government sources, your school financial aid office, your loan servicer, and qualified professionals when needed.