Scholarships vs Student Loans: What Students and Families Need to Know

Paying for college often feels like solving a puzzle with pieces that do not look alike. Scholarships, grants, savings, work income, federal student loans, private student loans, payment plans, and family contributions may all appear on the table at the same time. The challenge is not simply finding money. The real challenge is understanding which money helps you move forward and which money creates a future repayment obligation.

Scholarships and student loans are two of the most common college funding tools, but they work very differently. A scholarship is usually gift aid: money awarded for school that generally does not have to be repaid if you follow the award rules. A student loan is borrowed money: it must be repaid, usually with interest, after disbursement or after you leave school, depending on the loan terms.

This matters because two students can receive the same $10,000 in aid and end up in very different financial positions. One student may receive a $10,000 scholarship and lower the price of college without adding debt. Another may borrow $10,000 and later repay more than $10,000 because interest and fees increase the total cost. For a beginner, that difference can shape monthly cash flow, career choices, credit health, and long-term financial flexibility.

This guide is written for high school students, college students, parents, adult learners, graduate students, and anyone comparing financial aid options. It explains how scholarships and loans work, how to read aid offers, when borrowing may still make sense, and how to make a practical college funding decision without being overwhelmed by jargon.

Important NoteFederal Student Aid describes scholarships as monetary gifts that can help pay for college, career school, or trade school and do not need to be repaid, unlike student loans. The Consumer Financial Protection Bureau explains that students may use scholarships, grants, work-study, tuition payment plans, and federal or private student loans to pay for college.

1. Scholarships vs Student Loans: Simple Definitions

Scholarships are financial awards used to help pay education costs. They may be based on grades, talent, financial need, field of study, community service, identity, employer affiliation, military connection, location, or other eligibility rules. In most cases, scholarships do not have to be repaid as long as the student meets the scholarship conditions.

Student loans are borrowed funds used to pay education-related costs. Loans must be repaid according to the loan agreement. Depending on the loan type, interest may begin immediately, after disbursement, while the student is in school, after a grace period, or after a deferment period.

| Feature | Scholarships | Student Loans |

|---|---|---|

| Basic meaning | Gift aid for education expenses. | Borrowed money for education expenses. |

| Repayment | Usually no repayment required if rules are followed. | Repayment required, usually with interest. |

| Cost to student | Generally reduces the cost of college. | Can increase total education cost because of interest and fees. |

| Eligibility | Depends on award criteria such as merit, need, program, background, service, or talent. | Depends on loan type; federal loans generally require FAFSA eligibility, while private loans often depend on credit and income. |

| Best use | First-choice funding source before borrowing. | Gap funding after free aid, savings, work income, and affordable payment options are considered. |

2. Why This Comparison Matters

- It helps families reduce unnecessary debt before the first tuition bill arrives.

- It helps students understand the long-term cost of borrowing, not just the amount borrowed.

- It makes financial aid offers easier to compare across schools.

- It helps students avoid accepting loans automatically when grants, scholarships, work-study, or payment plans may be available.

- It encourages realistic planning for books, housing, transportation, technology, food, and other costs beyond tuition.

A useful rule of thumb is to pursue and accept money in this order when possible: free money first, earned money second, borrowed money last. Federal Student Aid’s guidance on evaluating aid offers similarly recommends considering grants and scholarships first, then work-study, and then student loans.

Reader advice: Federal Student Aid advises students comparing aid offers to consider grants and scholarships first, then work-study funds, and then student loans.

3. What Scholarships Are and How They Work

A scholarship is an award that helps pay for education. Some scholarships are small one-time awards. Others are renewable and may continue for multiple years if the student maintains eligibility. Scholarships may come from colleges, state agencies, nonprofits, employers, foundations, community groups, religious organizations, professional associations, or private donors.

3.1 Common Types of Scholarships

- Merit scholarships: Based on academic performance, test scores, leadership, arts, athletics, or other achievements.

- Need-based scholarships: Based partly or entirely on financial need.

- Program-specific scholarships: For students in certain majors, career paths, or professional programs.

- Identity or community scholarships: For students connected to a community, background, organization, region, employer, or life experience.

- Athletic or talent scholarships: Based on demonstrated ability in sports, music, theater, debate, design, or other fields.

- Local scholarships: Offered by community foundations, civic groups, local businesses, high schools, and regional organizations.

- Employer scholarships: Offered to employees, dependents of employees, or students entering an industry.

3.2 How Scholarship Money Is Paid

Scholarship funds may be sent directly to the school, paid to the student, credited to a student account, or reimbursed after expenses are documented. When money goes to the school, it usually reduces the balance due for tuition, fees, housing, or other school charges. When money goes to the student, the student may need to use it for approved education expenses and keep records.

3.3 Scholarship Rules to Watch

- Minimum GPA requirements.

- Full-time or half-time enrollment requirements.

- Major, program, school, or campus requirements.

- Deadlines for renewal applications.

- Required service, internship, competition, essay, portfolio, or reporting obligations.

- Limits on using funds for housing, transportation, supplies, or non-tuition expenses.

- Tax rules if funds are used for non-qualified expenses.

Reader advice: The IRS explains that scholarship or fellowship grant amounts may be tax-free when used for qualified education expenses by a candidate for a degree, but some amounts may be taxable depending on how the funds are used.

4. Benefits of Scholarships

- They reduce the amount a student needs to pay out of pocket or borrow.

- They usually do not require repayment.

- They can make a more expensive school more affordable.

- They may build a student’s resume by recognizing achievement, service, leadership, or talent.

- They can be combined with grants, savings, work-study, and sometimes loans.

- Renewable scholarships can reduce costs for several years, not just one semester.

5. Risks and Limits of Scholarships

- They are competitive, and receiving one is not guaranteed.

- Some are one-time awards, so they may not solve future-year costs.

- Missing a renewal requirement can cause the scholarship to disappear.

- Outside scholarships can sometimes change the school’s financial aid package, so students should ask how awards are applied.

- Scholarship scams exist; legitimate awards should not require suspicious fees or sensitive information beyond what is needed to apply.

- Scholarship funds used for non-qualified expenses may have tax consequences.

6. What Student Loans Are and How They Work

A student loan is money borrowed to pay education costs. The borrower signs a legal promise to repay the loan. Repayment terms depend on whether the loan is federal or private, whether interest is subsidized, whether a cosigner is involved, and which repayment plan applies.

6.1 Federal Student Loans

Federal student loans are offered through the U.S. Department of Education. To be considered for most federal student aid, students generally complete the Free Application for Federal Student Aid, commonly called the FAFSA. Federal student loans often provide borrower protections that private loans may not offer, such as fixed interest rates, income-driven repayment options, deferment or forbearance options, and potential access to forgiveness programs when eligibility rules are met.

6.2 Private Student Loans

Private student loans are issued by banks, credit unions, online lenders, state-based lenders, or other financial institutions. They may have fixed or variable interest rates, credit requirements, cosigner requirements, different repayment rules, and fewer borrower protections than federal loans. Private loans are often considered only after scholarships, grants, work income, savings, payment plans, and federal loan options have been reviewed.

Reader advice: The Consumer Financial Protection Bureau notes that federal student loans are made and guaranteed by the Department of Education, while private student loans are provided by private lenders and do not offer the same protections for consumers.

6.3 How Student Loan Costs Build Over Time

The amount you borrow is not always the amount you repay. Loan cost can include principal, interest, origination fees, late fees, collection costs, or other charges depending on the loan and borrower behavior. Interest is the price of borrowing money. Even a modest interest rate can add thousands of dollars over time if the balance is large or repayment takes many years.

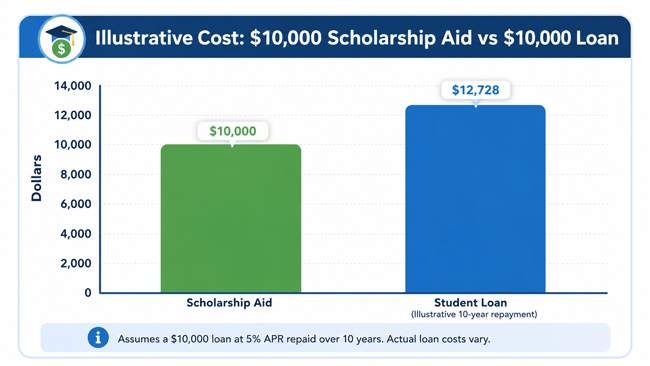

Figure: A simplified illustration showing why scholarship dollars and loan dollars are not financially equal. A scholarship reduces the bill. A loan creates a repayment obligation and may cost more than the amount borrowed.

7. Scholarships vs Student Loans: Detailed Comparison

| Comparison Point | Scholarships | Student Loans | Practical Takeaway |

|---|---|---|---|

| Repayment | Usually no repayment if conditions are met. | Must be repaid under the loan contract. | Prioritize scholarships before borrowing. |

| Interest | No interest because it is not debt. | Interest may accrue depending on loan type and timing. | Loans can cost more than the amount borrowed. |

| Fees | Usually none, but application-related costs can occur for transcripts or portfolios. | Federal and private loans may have fees; private terms vary. | Read the full cost, not just the approval amount. |

| Credit impact | No debt account created. | Can affect credit positively or negatively depending on repayment behavior. | Borrow only what you can realistically manage. |

| Availability | Competitive and deadline-driven. | Often more predictable if eligibility is met, but borrowing limits apply. | Apply early for scholarships and FAFSA. |

| Flexibility | Use may be restricted by award rules. | Can often cover approved cost of attendance gaps, but must be repaid. | Match each funding source to the right expense. |

| Best for | Reducing net price and avoiding debt. | Covering remaining necessary costs after free aid and lower-cost options. | Loans should fill gaps, not replace planning. |

8. Pros and Cons of Scholarships

| Pros | Cons or Limitations |

|---|---|

| Usually do not have to be repaid. | Competitive and not guaranteed. |

| Can reduce or eliminate the need for loans. | May require essays, recommendations, portfolios, interviews, or renewals. |

| Can improve a student’s confidence and resume. | May be restricted to specific expenses, schools, majors, or enrollment levels. |

| Local and niche scholarships can be less crowded than national awards. | One-time awards may not help with sophomore, junior, or senior-year costs. |

| Some scholarships are renewable for several years. | Tax issues may arise if funds are used for non-qualified expenses. |

9. Pros and Cons of Student Loans

| Pros | Cons or Risks |

|---|---|

| Can make college possible when savings and free aid are not enough. | Must be repaid, usually with interest. |

| Federal loans may offer fixed rates and borrower protections. | Monthly payments can limit future cash flow. |

| Can help cover remaining cost of attendance gaps. | Borrowing too much can create long-term financial stress. |

| Responsible repayment can help build credit history. | Late payments, delinquency, or default can damage credit and trigger serious consequences. |

| Some repayment plans may adjust payments based on income for eligible federal loans. | Private loans may have fewer flexible repayment options and may require a cosigner. |

10. Which Is Better: Scholarships or Student Loans?

Scholarships are usually better than student loans because they reduce the cost of college without creating debt. However, the best funding plan often uses more than one source. A student may combine scholarships, grants, family savings, part-time work, tuition payment plans, and a carefully limited federal student loan to cover a realistic education budget.

The better question is not only “Which is better?” but “How much free aid can I get before I borrow, and how little can I borrow while still completing the program?”

10.1 Recommended Order for Paying for College

- Choose an affordable school or program based on net price, not sticker price.

- Use savings and family contributions that do not create financial hardship.

- Apply for grants and scholarships as early and widely as possible.

- Use work-study or part-time work if it does not harm academic performance.

- Consider tuition payment plans for manageable short-term balances.

- Use federal student loans carefully if a gap remains.

- Consider private student loans only after comparing federal options and understanding the risks.

11. Step-by-Step Process: How to Decide Between Scholarships and Student Loans

- Calculate the full cost of attendance. Include tuition, fees, housing, food, books, transportation, supplies, technology, health insurance, and personal expenses.

- Complete the FAFSA as early as possible if you may attend a U.S. eligible institution and want access to federal aid.

- Search for scholarships from the school, local community, employers, nonprofits, professional groups, and trusted scholarship databases.

- Read every scholarship rule before applying. Check eligibility, deadlines, renewal rules, required documents, and permitted expenses.

- Compare financial aid offers by net price. Subtract grants and scholarships from the school’s total cost before comparing loans.

- Separate gift aid from loans. Do not treat a loan as a discount; it is borrowed money.

- Estimate future loan payments before borrowing. Use a loan simulator or repayment calculator to understand monthly payments and total repayment cost.

- Borrow only what is necessary. You do not have to accept the full loan amount offered.

- Ask the financial aid office how outside scholarships affect your aid package.

- Re-check the plan each year because tuition, housing costs, aid eligibility, family income, and scholarship availability can change.

Reader advice: The CFPB states that completing the FAFSA is required to be eligible for federal student loans, work-study, or grants, and Federal Student Aid offers a Loan Simulator for comparing repayment plans and estimated payments.

12. Real-World Examples

12.1 Example 1: The Student Who Reduces Borrowing With Local Scholarships

Maya plans to attend a public university. Her remaining bill after grants is $6,000 for the year. She is offered a $5,500 federal student loan. Instead of accepting the full loan immediately, she applies for local scholarships through her high school counseling office, a community foundation, and a local professional association. She wins two awards totaling $2,000. Maya then borrows only $3,500 instead of $5,500.

Potential outcome: Maya still uses a student loan, but she reduces her first-year debt by $2,000. If she repeats this strategy each year, the long-term difference could be meaningful.

12.2 Example 2: The Student Who Chooses Net Price Over Sticker Price

Jordan is accepted to two colleges. College A has a higher sticker price but offers a strong renewable scholarship. College B has a lower sticker price but offers less gift aid. After comparing net price, College A is actually less expensive for Jordan. He confirms the renewal GPA requirement and chooses the school with the lower four-year estimated cost.

Potential outcome: Jordan avoids choosing based only on published tuition and focuses on the amount his family must actually pay or borrow.

12.3 Example 3: The Student Who Borrows Too Much Because the Loan Was “Available”

Aisha receives a loan offer larger than her actual remaining school bill. She accepts the full amount and uses the refund for nonessential spending. Later, she realizes that every extra dollar became debt. She changes course the next semester by creating a budget, returning unneeded funds when possible, and accepting only the amount required for school expenses.

Potential outcome: Aisha learns that loan availability is not the same as affordability. Borrowed refunds can feel helpful in the moment but can increase repayment stress later.

12.4 Example 4: The Adult Learner Balancing Work, Scholarships, and Loans

Carlos returns to school for a career-focused certificate. He works part time, applies for an employer tuition benefit, receives a small scholarship, and uses a limited federal loan for the remaining tuition. He compares the expected earnings benefit of the credential with the amount he must repay.

Potential outcome: Borrowing may be reasonable when it is limited, tied to a credible career plan, and part of a broader funding strategy rather than the entire plan.

13. Costs and Fees to Understand

13.1 Scholarship Costs

Legitimate scholarships generally do not require repayment and should not require you to pay a large fee to receive an award. However, students may encounter indirect costs such as transcript fees, test score reporting fees, travel for auditions or interviews, portfolio preparation, or tax costs if funds are used for non-qualified expenses.

13.2 Student Loan Costs

- Principal: the amount borrowed.

- Interest: the cost of borrowing, usually expressed as an annual percentage rate.

- Origination fee: a fee deducted from some loans before funds are disbursed or added according to loan terms.

- Capitalized interest: unpaid interest that is added to principal in certain situations, causing interest to accrue on a higher balance.

- Late fees or collection costs: possible costs if payments are missed or the loan defaults.

- Cosigner risk: for private loans, a cosigner may become legally responsible if the borrower does not repay.

14. Scholarship Tax Considerations

Scholarships can be tax-free in certain situations, but they are not automatically tax-free in every case. In general, scholarship funds are more likely to be tax-free when the recipient is a degree candidate and the money is used for qualified education expenses such as tuition and required fees, books, supplies, and equipment. Amounts used for other expenses may be taxable. Because tax rules can be specific, students should keep records and consult official IRS guidance or a qualified tax professional when needed.

Reader advice: IRS Topic No. 421 explains that scholarships, fellowship grants, and other grants may be tax-free when certain conditions are met, including use for qualified education expenses by a degree candidate.

15. Most Searched Questions About Scholarships vs Student Loans

| Question | Direct Answer |

|---|---|

| Are scholarships better than student loans? | Usually yes, because scholarships generally do not have to be repaid and do not accrue interest. |

| Can scholarships reduce student loans? | Yes. Scholarship funds can reduce the amount you need to borrow, but ask your school how outside scholarships affect your aid package. |

| Do scholarships have to be paid back? | Usually no, unless you violate award terms, withdraw, fail to meet renewal rules, or the award has special conditions. |

| Should I accept student loans before applying for scholarships? | Usually no. Apply for scholarships and grants first, then borrow only what you still need. |

| Are private student loans the same as federal student loans? | No. Private loans are made by private lenders and often lack the protections available with federal loans. |

16. Common Mistakes to Avoid

- Mistake 1: Treating loans like scholarships. A loan is not a discount; it is debt that must be repaid.

- Mistake 2: Ignoring small scholarships. Several smaller awards can add up and reduce borrowing.

- Mistake 3: Missing deadlines. Scholarship and FAFSA deadlines can arrive months before the school year begins.

- Mistake 4: Accepting the full loan amount automatically. You may be able to accept a smaller amount.

- Mistake 5: Comparing colleges by sticker price instead of net price. Gift aid can change the real cost dramatically.

- Mistake 6: Forgetting renewal rules. A scholarship that disappears after the first year can create a surprise funding gap.

- Mistake 7: Using loan refunds for lifestyle spending. Refund money may still be borrowed money.

- Mistake 8: Applying only for national scholarships. Local scholarships may have fewer applicants.

- Mistake 9: Not reading private loan terms. Variable rates, cosigner obligations, and limited repayment flexibility can create risk.

- Mistake 10: Failing to ask for help. Financial aid offices can explain aid offers, scholarship displacement policies, and borrowing options.

17. Expert Tips for Choosing Smarter College Funding

- Build a scholarship calendar with deadlines, documents, essay prompts, and renewal dates.

- Reuse strong essay themes, but customize each application for the award criteria.

- Ask your school whether outside scholarships reduce loans first, unmet need first, or other aid first.

- Estimate four-year costs, not just first-year costs.

- Prefer federal student loans over private loans when you must borrow and are eligible, because federal loans generally provide stronger borrower protections.

- Avoid borrowing for expenses you can reasonably reduce through budgeting, used textbooks, housing choices, meal planning, or transportation decisions.

- Keep scholarship award letters, receipts, tuition statements, and tax records in one folder.

- Review your loan balance at least once per semester so debt does not become invisible.

- Before choosing a school, compare likely debt at graduation with realistic early-career income in your field.

- Speak with a financial aid counselor before declining, reducing, or changing aid if you are unsure how it affects your package.

18. Quick Action Checklist

- List every college cost you expect for the year.

- Complete the FAFSA if you may qualify for U.S. federal aid.

- Search school, local, employer, nonprofit, and professional association scholarships.

- Apply for scholarships before accepting unnecessary loans.

- Read award rules and renewal requirements.

- Compare net price across schools after grants and scholarships.

- Separate gift aid from loans in every aid offer.

- Estimate monthly loan payments before borrowing.

- Accept only the loan amount you truly need.

- Repeat the process every year.

19. Decision Guide: When to Use Scholarships, Loans, or Both

| Situation | Best First Move | When Loans May Fit |

|---|---|---|

| You have time before enrollment. | Apply broadly for scholarships and complete financial aid forms early. | Only after free aid and affordable options are reviewed. |

| Your bill is due soon and scholarships are pending. | Contact the financial aid office and billing office about extensions or payment plans. | A small federal loan may help if the program is affordable and borrowing is necessary. |

| You received an outside scholarship. | Ask how it changes your aid package. | Reduce loans first if the school allows it. |

| You are considering a private loan. | Compare federal options, school payment plans, and lower-cost alternatives. | Only if terms are clear, payments are affordable, and no safer option covers the gap. |

| You are choosing between schools. | Compare net price and likely debt at graduation. | Borrow less for a comparable program when possible. |

20. Frequently Asked Questions About Scholarships vs Student Loans

20.1 What is the main difference between scholarships and student loans?

The main difference is repayment. Scholarships are usually gift aid that does not have to be repaid, while student loans are borrowed money that must be repaid, usually with interest. This makes scholarships a lower-cost funding source in most cases.

20.2 Are scholarships always better than student loans?

Usually, yes. Scholarships are generally better because they reduce college costs without creating debt. However, scholarships may not cover every expense, so some students still use loans carefully to fill a remaining gap.

20.3 Do scholarships have to be repaid?

Most scholarships do not have to be repaid if you follow the award rules. Repayment or loss of eligibility may happen if you withdraw, fail to meet renewal requirements, use funds improperly, or violate specific conditions.

20.4 Can scholarships pay for room and board?

Some scholarships can pay for room and board, but others are restricted to tuition, fees, books, or required supplies. Read the award letter carefully and ask the scholarship provider or school if the rules are unclear.

20.5 Can I use scholarships and student loans together?

Yes. Many students use scholarships and loans together. The smart approach is to use scholarships and grants first, then borrow only the amount still needed.

20.6 Can scholarships reduce my financial aid package?

Yes, outside scholarships can affect a school financial aid package. Some schools reduce loans first, while others may reduce other aid. Ask the financial aid office how outside awards are handled.

20.7 Should I accept federal or private student loans first?

If you must borrow and are eligible, federal student loans are often considered before private student loans because they generally offer stronger borrower protections and repayment options. Private loans require careful comparison of rates, fees, cosigner rules, and repayment flexibility.

20.8 Is a scholarship taxable?

A scholarship may be tax-free if it meets IRS rules, such as being used for qualified education expenses by a degree candidate. Amounts used for other expenses may be taxable, so keep records and review IRS guidance.

20.9 Do I need the FAFSA for scholarships?

Sometimes. Many private scholarships do not require the FAFSA, but some school, state, and need-based scholarships may use FAFSA information. Completing the FAFSA can also help you access grants, work-study, and federal student loans.

20.10 How many scholarships should I apply for?

Apply for as many relevant scholarships as you can manage without sacrificing application quality. A focused list of well-matched scholarships is usually better than random applications to awards you barely qualify for.

20.11 What is scholarship displacement?

Scholarship displacement happens when an outside scholarship reduces other financial aid in your package. The impact depends on school policy, so ask whether the scholarship will reduce loans, unmet need, work-study, grants, or institutional aid.

20.12 Should I borrow if I receive a scholarship?

Borrow only if a real funding gap remains after scholarships, grants, savings, work income, and affordable payment options. A scholarship lowers the amount you may need to borrow, but it may not eliminate borrowing completely.

20.13 Can I decline part of a student loan?

In many cases, yes. Students often do not have to accept the full loan amount offered. Contact the school financial aid office to understand how to accept, reduce, or cancel a loan.

20.14 Are scholarships only for students with perfect grades?

No. Many scholarships consider financial need, leadership, service, career goals, location, background, employer affiliation, major, talent, or personal experience. Strong grades can help, but they are not the only path.

20.15 What should I do if scholarships do not cover all college costs?

Compare the remaining net price, ask the school about additional aid or payment plans, consider part-time work, reduce nonessential costs, and evaluate federal student loans before private loans. Borrow only what you can reasonably repay.

21. Conclusion: Use Free Aid First and Borrow With a Plan

Scholarships and student loans can both help pay for education, but they are not equal. Scholarships usually lower the cost of college without creating debt. Student loans can make school possible when free aid is not enough, but they create a repayment obligation that can affect your future budget.

The best practice is simple: search for scholarships early, compare schools by net price, use grants and scholarships first, understand every condition attached to aid, and borrow only what is necessary. When borrowing is unavoidable, federal student loans are often the first place to compare because of their borrower protections, but every loan should be reviewed carefully before acceptance.

A thoughtful college funding plan does not require perfection. It requires awareness, deadlines, realistic numbers, and a willingness to ask questions before signing. The more free aid you secure and the less unnecessary debt you take on, the more financial flexibility you keep after graduation.

21.1 Sources Consulted

- Federal Student Aid, Financial Aid Dictionary and scholarship guidance - https://studentaid.gov/articles/financial-aid-dictionary/

- Federal Student Aid, How To Evaluate Your Aid Offers - https://studentaid.gov/articles/evaluating-financial-aid-offers/

- Federal Student Aid, Direct Subsidized vs. Direct Unsubsidized Loans - https://studentaid.gov/articles/subsidized-vs-unsubsidized-loans/

- Federal Student Aid, Federal Student Loan Interest Rates - https://studentaid.gov/understand-aid/types/loans/interest-rates

- Consumer Financial Protection Bureau, Ways to Pay for College or Graduate School - https://www.consumerfinance.gov/ask-cfpb/what-are-the-different-ways-to-pay-for-college-or-graduate-school-en-545/

- Consumer Financial Protection Bureau, Applying for Financial Aid - https://www.consumerfinance.gov/consumer-tools/student-loans/applying-for-financial-aid/

- Internal Revenue Service, Topic No. 421, Scholarships, Fellowship Grants, and Other Grants - https://www.irs.gov/taxtopics/tc421

- Internal Revenue Service, Publication 970, Tax Benefits for Education - https://www.irs.gov/publications/p970

Reader Advice: This article is for general educational and informational purposes only and does not constitute individualized financial, legal, tax, accounting, or investment advice. Loan rates, APRs, fees, eligibility, underwriting standards, credit reporting practices, and applicable laws may vary by lender, loan type, borrower profile, location, and current regulations.

Always review the official loan agreement and disclosures, compare offers based on APR, fees, monthly payments, and total repayment cost, and verify current terms with the lender, loan servicer, StudentAid.gov, the SBA, or other relevant official sources when applicable.

If you need advice for your specific situation, especially involving debt disputes, lawsuits, foreclosure, wage garnishment, bankruptcy, or tax matters, consult a qualified financial professional, nonprofit credit counselor, tax adviser, accountant, consumer attorney, or legal aid organization.