Parent Loans vs Student Loans: Complete Guide for Families

1. Why This Decision Matters More Than Many Families Realize

When a college financial aid offer does not cover the full cost of attendance, families often face a difficult question: should the student borrow, should the parent borrow, or should both contribute? This is where the choice between parent loans and student loans becomes important.

A student loan is usually borrowed by the student and is legally the student’s responsibility. A parent loan, such as a federal Parent PLUS Loan, is borrowed by the parent and is legally the parent’s responsibility. That difference sounds simple, but it affects credit, repayment options, loan forgiveness access, retirement planning, household cash flow, and family relationships.

This guide is for parents, undergraduate students, guardians, and families trying to make a responsible college financing decision. It is especially useful if you are comparing Parent PLUS loans, federal Direct Subsidized or Unsubsidized Loans, private student loans, private parent loans, or a mix of borrowing options.

The main concern is not only “Can we get approved?” The better question is “Who can safely repay this debt without damaging their future?” A loan that helps a student enroll today can become a serious financial burden later if the borrower misunderstands the cost, repayment rules, or legal responsibility.

| At-a-Glance Comparison | Parent Loans | Student Loans |

|---|---|---|

| Legal borrower | Parent or eligible parent borrower | Student borrower; a cosigner may be involved for private loans |

| Common federal option | Federal Parent PLUS Loan | Direct Subsidized Loan, Direct Unsubsidized Loan, Grad PLUS Loan for graduate/professional students |

| Credit check | Required for Parent PLUS; looks for adverse credit history | No credit check for most federal undergraduate Direct Loans; private loans usually require credit review |

| Repayment responsibility | Parent is responsible, even if the family informally agrees the student will pay | Student is responsible; cosigner may also be responsible on private loans |

| Typical federal repayment flexibility | Less flexible than student Direct Loans; Parent PLUS generally needs consolidation to access ICR | Federal student loans generally have broader repayment and deferment options |

| Best fit | Parents with stable finances who can repay without sacrificing retirement or essentials | Students who need to use federal loan limits before considering parent or private debt |

2. What Are Parent Loans?

Parent loans are education loans borrowed by a parent to help pay for a child’s college costs. The best-known federal parent loan is the Direct Parent PLUS Loan, available to eligible parents of dependent undergraduate students. Private lenders may also offer parent loans.

With a parent loan, the parent is the borrower. The school may use the funds for tuition, fees, housing, meal plans, and other eligible education costs, but the repayment obligation belongs to the parent. An informal promise from the student to help with payments does not remove the parent’s legal responsibility.

2.1 What Is a Federal Parent PLUS Loan?

A Parent PLUS Loan is a federal Direct PLUS Loan that an eligible parent can borrow for a dependent undergraduate student. The parent can generally borrow up to the school-certified cost of attendance minus other financial aid, subject to federal rules and any applicable limits.

- The parent applies separately, usually after the FAFSA and school aid offer are reviewed.

- The parent must not have an adverse credit history, although appeal and endorser options may exist if denied.

- Interest begins accruing when the loan is disbursed.

- Repayment normally begins shortly after final disbursement unless the parent requests deferment while the student is enrolled at least half time.

3. What Are Student Loans?

Student loans are education loans borrowed by the student to pay for college, career school, graduate school, or professional school. Federal student loans are typically the first loans students should evaluate because they usually offer fixed rates, standardized terms, and borrower protections not always available from private lenders.

3.1 Federal Student Loans for Undergraduates

For undergraduate students, the main federal options are Direct Subsidized Loans and Direct Unsubsidized Loans. Subsidized loans are need-based and the government generally pays the interest during certain in-school and deferment periods. Unsubsidized loans are not need-based, and interest begins accruing when the loan is disbursed.

3.2 Private Student Loans

Private student loans are offered by banks, credit unions, online lenders, and some state or school-affiliated programs. They often require a creditworthy borrower or cosigner. Their rates, fees, deferment rules, forbearance options, death or disability discharge terms, and cosigner release policies vary by lender.

4. How Parent Loans and Student Loans Work

- The student completes the FAFSA if seeking federal aid.

- The school sends a financial aid offer showing grants, scholarships, work-study, and federal student loan eligibility.

- The family calculates the remaining funding gap after free aid and affordable cash contributions.

- The student usually considers federal student loans first because undergraduate federal student loans do not require a credit check and have borrower protections.

- If a gap remains, the family compares parent loans, private student loans, payment plans, scholarships, a less expensive school, or reducing expenses.

- The borrower signs required loan documents, such as a Master Promissory Note for federal loans.

- Funds are sent to the school, school charges are paid, and any eligible refund is released according to school policy.

- The borrower repays the loan according to the loan type, repayment plan, and servicer instructions.

5. Parent Loans vs Student Loans: Key Differences

| Feature | Parent Loan | Student Loan | Why It Matters |

|---|---|---|---|

| Borrower identity | Parent | Student | The legal borrower controls repayment decisions and bears the credit consequences. |

| Federal undergraduate availability | Parent PLUS for eligible parents of dependent undergraduates | Direct Subsidized and Unsubsidized Loans for eligible students | Students usually have limited annual federal borrowing amounts; parents may fill a gap. |

| Credit requirement | Parent PLUS requires a credit check for adverse credit history; private parent loans use lender underwriting | Most undergraduate federal student loans do not require a credit check; private student loans often do | Approval should not be confused with affordability. |

| Interest and fees | Parent PLUS loans often have higher rates and fees than undergraduate Direct Loans | Undergraduate Direct Loans usually cost less than Parent PLUS loans | Higher cost can increase total repayment significantly. |

| Repayment flexibility | Parent PLUS has fewer federal repayment options unless consolidated for ICR | Federal student loans generally have more repayment plan options | Flexibility matters if income falls or the borrower faces hardship. |

| Family impact | Can affect parent credit, retirement, mortgage plans, and cash flow | Can affect student credit and early adult financial choices | The right choice depends on who can repay safely. |

6. Current Federal Cost Snapshot: Interest Rates and Origination Fees

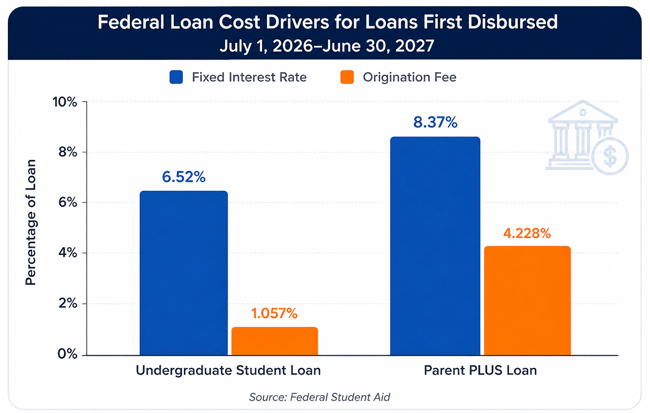

Federal student loan rates are set annually for loans first disbursed during a July 1 to June 30 period. For loans first disbursed on or after July 1, 2026, and before July 1, 2027, Federal Student Aid announced fixed rates of 6.52% for undergraduate Direct Subsidized and Unsubsidized Loans, 8.07% for graduate/professional Direct Unsubsidized Loans, and 9.07% for Direct PLUS Loans.

Federal loan origination fees may also apply and are deducted from loan disbursements. Because rates, fees, and laws can change, borrowers should confirm current terms on StudentAid.gov and with the school’s financial aid office before borrowing.

| Federal loan type | 2026-2027 fixed interest rate | Common borrower | Cost note |

|---|---|---|---|

| Direct Subsidized/Unsubsidized - undergraduate | 6.52% | Student | Usually lower cost than Parent PLUS. |

| Direct Unsubsidized - graduate/professional | 8.07% | Graduate/professional student | Not available to parents for undergraduate education. |

| Direct PLUS - parent or graduate/professional | 9.07% | Parent or graduate/professional student | Often higher rate and higher fee than undergraduate Direct Loans. |

Chart note: Rates shown are federal fixed interest rates for 2026-2027 loans; origination fee examples reflect commonly published federal fee levels in effect for recent Direct Loans. Always verify the current fee before borrowing.

7. Benefits of Parent Loans

- They can help cover a remaining college funding gap after grants, scholarships, savings, income, and student federal loans.

- Parent PLUS Loans have a fixed federal interest rate for the life of that loan.

- A parent may be able to borrow more than the student’s annual federal undergraduate loan limit, subject to school certification and law.

- They keep the debt legally with the parent, which may be appropriate if the parent intentionally wants to pay for part of the education.

- Parents may request in-school deferment, although interest still accrues.

8. Benefits of Student Loans

- Federal undergraduate student loans usually have lower rates than Parent PLUS loans.

- Most federal undergraduate student loans do not require a credit check or cosigner.

- Federal student loans generally offer more repayment flexibility than Parent PLUS loans.

- Borrowing in the student’s name can build responsibility when the amount is reasonable and tied to expected income.

- Subsidized loans can reduce interest costs for eligible students because the government covers interest during certain periods.

9. Risks of Parent Loans vs Student Loans

| Risk | Parent Loan Concern | Student Loan Concern | How to Reduce the Risk |

|---|---|---|---|

| Overborrowing | Parents may borrow large amounts late in their careers. | Students may borrow more than their expected income can support. | Set a total borrowing cap before choosing a school. |

| Retirement pressure | Parent debt can delay retirement savings or force withdrawals. | Student debt can delay housing, saving, or career flexibility. | Protect retirement and emergency savings before borrowing. |

| Repayment shock | Parent PLUS repayment can start soon after disbursement unless deferred. | Student repayment usually starts after leaving school, but interest may accrue. | Estimate payments before signing. |

| Limited flexibility | Parent PLUS has fewer repayment protections than many student Direct Loans. | Private student loans may have fewer protections than federal loans. | Favor federal student loans first and compare repayment options. |

| Family conflict | Parent and student may disagree about who “should” pay later. | Cosigners may be surprised by legal responsibility. | Put family expectations in writing, even if informal. |

10. When Parent Loans May Make Sense

- The student has already used reasonable federal student loan eligibility and a modest gap remains.

- The parent has stable income, strong emergency savings, manageable debt, and retirement planning on track.

- The parent is intentionally choosing to pay part of the education and can afford the monthly payment without relying on the student.

- The family has compared lower-cost schools, scholarships, work income, and payment plans first.

- The parent understands that the loan is legally theirs and may affect their credit and household budget.

11. When Student Loans May Be the Better First Choice

- The student is eligible for federal Direct Subsidized or Unsubsidized Loans.

- The loan amount is modest compared with likely first-year earnings after graduation.

- The student wants access to federal repayment protections and potential federal forgiveness pathways available to eligible student borrowers.

- The parents cannot safely take on debt without harming retirement, housing stability, or essential expenses.

12. Step-by-Step Process to Choose the Right Loan

- Start with the net price, not the sticker price. Subtract grants, scholarships, and gift aid from the total cost of attendance.

- Use free and low-risk funding first. Prioritize grants, scholarships, savings, affordable income, employer benefits, and school payment plans.

- Use federal student loans before Parent PLUS or private loans when appropriate. Undergraduate Direct Loans are often cheaper and more flexible.

- Estimate monthly payments for every borrower. Do not borrow until the parent and student both understand the payment amount.

- Compare total cost, not just the first-year gap. A manageable first-year loan can become unmanageable if repeated for four or more years.

- Test the parent’s budget. Parent loans should not crowd out rent, mortgage, food, medical expenses, emergency savings, or retirement contributions.

- Review repayment options before signing. Parent PLUS repayment options differ from student loan repayment options.

- Avoid private refinancing unless you understand what federal protections you lose. Refinancing federal debt into a private loan is usually irreversible.

- Confirm details with the school financial aid office and StudentAid.gov before accepting loans.

13. Real-World Examples

13.1 Example 1: The Student Uses Federal Loans First

Maya receives scholarships and grants but still has a $5,000 funding gap. She is eligible for federal undergraduate student loans. Her parents are paying for housing but cannot afford new monthly debt. Maya accepts a modest federal student loan, works part time, and reduces optional living expenses. This approach keeps the debt lower-cost and avoids putting her parents’ retirement budget at risk.

13.2 Example 2: A Parent PLUS Loan Covers a Small Final Gap

Daniel’s family has already used scholarships, a school payment plan, summer savings, and his federal student loan eligibility. A $3,000 gap remains. Daniel’s mother has stable income, no high-interest debt, a healthy emergency fund, and retirement contributions on track. She chooses a small Parent PLUS Loan and plans to repay it aggressively. This may be reasonable because the amount is limited and affordable.

13.3 Example 3: The Parent Loan Is Too Risky

A parent is offered a Parent PLUS Loan to cover a large annual gap. The parent is already carrying credit card debt and has little retirement savings. Even if approved, the loan could make the household financially fragile. In this case, the better decision may be to appeal for more aid, choose a less expensive school, start at a community college, increase work income, or delay enrollment rather than borrow beyond capacity.

14. Common Mistakes to Avoid

- Assuming approval means the loan is affordable. A credit approval does not prove the monthly payment fits your budget.

- Letting the parent borrow everything before the student uses reasonable federal student loan eligibility.

- Ignoring interest while loans are deferred. Interest can accrue even when payments are postponed.

- Believing the student is legally responsible for a Parent PLUS Loan. The parent remains responsible unless a private refinance transfers the debt, and that can involve losing federal protections.

- Consolidating Parent PLUS loans with the parent’s own federal student loans without understanding lost repayment options.

- Using credit cards or home equity to pay student loans without carefully comparing risk.

- Borrowing for the dream school without comparing graduation rates, major outcomes, transfer options, and lower-cost alternatives.

- Forgetting that parent debt can affect retirement, mortgage qualification, and family emergency planning.

15. Expert Tips for Safer Borrowing

- Set a four-year borrowing plan before the first semester begins.

- Keep total student borrowing aligned with realistic starting salaries, not optimistic best-case income.

- Parents should treat Parent PLUS payments like any other household debt payment, not as a temporary favor.

- Ask the school if more grant aid, departmental scholarships, emergency aid, resident assistant roles, or tuition payment plans are available.

- Before taking a private loan, compare fixed vs variable rates, cosigner release, deferment, forbearance, death and disability discharge, and default rules.

- Document family expectations. Even a simple written agreement can reduce future conflict.

- Review the loan servicer account soon after disbursement so you know the balance, interest rate, and repayment date.

16. Quick Action Checklist

- Calculate the true remaining gap after scholarships, grants, savings, and affordable cash flow.

- Use the FAFSA and review federal student loan eligibility first.

- Compare Parent PLUS, student federal loans, private loans, and school payment plans side by side.

- Estimate the monthly payment for the parent and the student separately.

- Decide who is legally borrowing and who is expected to help pay.

- Check whether the parent can repay without harming retirement or emergency savings.

- Ask the financial aid office about lower-cost alternatives before borrowing more.

- Save copies of loan terms, interest rates, fees, and repayment dates.

- Revisit the plan every academic year before accepting more debt.

17. Frequently Asked Questions About Parent Loans vs Student Loans

17.1 Are parent loans the same as student loans?

No. Parent loans are borrowed by the parent, while student loans are borrowed by the student. The legal borrower is responsible for repayment.

17.2 Is a Parent PLUS Loan in the parent’s name or the student’s name?

A federal Parent PLUS Loan is in the parent’s name. The parent is legally responsible for repayment, even if the student agrees to help.

17.3 Should students take federal loans before parents take Parent PLUS loans?

Often, yes. Undergraduate federal student loans usually have lower costs and more flexible protections than Parent PLUS loans.

17.4 Can a student repay a Parent PLUS Loan?

A student can voluntarily make payments, but the parent remains legally responsible unless the debt is refinanced into the student’s name through a private lender.

17.5 Can Parent PLUS Loans be forgiven?

Parent PLUS Loans may have limited forgiveness pathways, but rules are narrower than for many student Direct Loans. Parent PLUS borrowers generally need to consolidate to access ICR and then may pursue qualifying forgiveness programs if all requirements are met.

17.6 Do Parent PLUS Loans require a credit check?

Yes. Parent PLUS Loans require a credit check for adverse credit history. This is different from full private-loan underwriting and does not necessarily measure affordability.

17.7 Do federal student loans require a credit check?

Most federal undergraduate Direct Subsidized and Unsubsidized Loans do not require a credit check. Private student loans usually do.

17.8 Which is cheaper: Parent PLUS or student loans?

Federal undergraduate student loans are usually cheaper than Parent PLUS loans because they commonly have lower interest rates and fees.

17.9 Can parents transfer Parent PLUS Loans to the student?

The federal government does not simply transfer Parent PLUS Loans to the student. Some private lenders may refinance the loan into the student’s name if the student qualifies, but federal protections may be lost.

17.10 What happens if a parent cannot pay a Parent PLUS Loan?

The parent should contact the servicer quickly. Options may include deferment, forbearance, consolidation, or ICR after consolidation. Waiting can lead to delinquency, default, collection costs, and credit damage.

17.11 Are private parent loans better than Parent PLUS Loans?

Not automatically. Private parent loans may offer lower rates for highly qualified borrowers, but they may lack federal protections. Compare total cost and hardship options carefully.

17.12 Can both a parent and student borrow for the same year?

Yes. Many families use a combination of student federal loans, parent loans, scholarships, savings, work income, and payment plans.

17.13 How much should parents borrow for college?

Parents should borrow only what they can repay from their own budget without relying on retirement withdrawals, credit cards, or the student’s future income.

17.14 What if a Parent PLUS Loan is denied?

The parent may be able to appeal, use an endorser, or the student may qualify for additional Direct Unsubsidized Loan funds. The family should also speak with the financial aid office.

17.15 What is the safest order to pay for college?

A common safer order is scholarships and grants, affordable savings and income, federal student loans, school payment plans, then carefully evaluated parent or private loans only if needed.

18. Conclusion: The Best Loan Is the One the Right Borrower Can Repay Safely

Parent loans and student loans can both help pay for college, but they are not interchangeable. The borrower’s name, credit risk, repayment options, interest cost, and long-term financial impact can be very different.

For many undergraduate families, the practical starting point is to maximize free aid, compare lower-cost school options, and use reasonable federal student loans before considering Parent PLUS or private loans. Parent loans may make sense for a limited, affordable gap, but they can become dangerous when they threaten retirement, essential expenses, or household stability.

The best decision is not the loan that covers the bill fastest. It is the plan that helps the student complete a valuable education while keeping both the student and parent financially healthy.

18.1 Sources Consulted

- Federal Student Aid. (2026). Interest Rates for Federal Direct Loans First Disbursed Between July 1, 2026 and June 30, 2027. https://fsapartners.ed.gov/knowledge-center/library/electronic-announcements/2026-06-04/interest-rates-federal-direct-loans-first-disbursed-between-july-1-2026-and-june-30-2027

- Federal Student Aid. Parent PLUS Loans. https://studentaid.gov/understand-aid/types/loans/plus/parent

- Consumer Financial Protection Bureau. (2024). Options for repaying your Parent PLUS loans. https://www.consumerfinance.gov/paying-for-college/repay-student-debt/federal-parent-plus-loans/

- Federal Student Aid. PLUS Loans: What to Do if You Are Denied Based on Adverse Credit History. https://studentaid.gov/articles/plus-loans-denied-adverse-credit/

- Consumer Financial Protection Bureau. Student loans key terms. https://www.consumerfinance.gov/consumer-tools/student-loans/answers/key-terms/

Reader Advice: This article is for general educational and informational purposes only and does not constitute individualized financial, legal, tax, accounting, or investment advice. Loan rates, APRs, fees, eligibility, underwriting standards, credit reporting practices, and applicable laws may vary by lender, loan type, borrower profile, location, and current regulations.

Always review the official loan agreement and disclosures, compare offers based on APR, fees, monthly payments, and total repayment cost, and verify current terms with the lender, loan servicer, StudentAid.gov, the SBA, or other relevant official sources when applicable.

If you need advice for your specific situation, especially involving debt disputes, lawsuits, foreclosure, wage garnishment, bankruptcy, or tax matters, consult a qualified financial professional, nonprofit credit counselor, tax adviser, accountant, consumer attorney, or legal aid organization.