Student Loan Interest Rates Explained

1. Why Student Loan Interest Rates Matter

Student loan interest rates affect how much education debt actually costs. The amount you borrow is only the starting point. Interest can determine whether a loan feels manageable after graduation or becomes a long-term financial burden. For beginners, the confusing part is that the rate is not just a number on a loan offer. It affects daily interest charges, monthly payments, total repayment cost, refinancing decisions, and whether a federal or private loan is safer.

This guide is for students, parents, graduate borrowers, cosigners, and anyone already repaying student loans. It explains student loan interest rates in plain English, shows how interest is calculated, compares federal and private rates, and gives practical steps to help you borrow less, compare offers wisely, and avoid expensive mistakes.

The most important concern for many borrowers is simple: “How much will this loan really cost me?” The answer depends on the interest rate, the loan balance, repayment term, fees, whether interest accrues while you are in school, and whether unpaid interest gets added to your principal. Understanding these pieces before signing a loan can save real money and reduce stress later.

2. What Are Student Loan Interest Rates?

A student loan interest rate is the price a lender charges you for borrowing money to pay for education. It is expressed as an annual percentage rate, but most student loan interest accrues daily. In simple terms, the higher the rate and the longer you take to repay, the more the loan costs.

Student loan interest is the cost of borrowing education money. The interest rate determines how quickly interest is added to your loan balance and how much you pay beyond the original amount borrowed.

2.2 Student Loan Interest vs. Principal

| Term | Meaning | Example |

|---|---|---|

| Principal | The amount you originally borrowed, plus any capitalized interest. | $20,000 borrowed for tuition and living costs. |

| Interest | The lender’s charge for lending you money. | A 6.52% rate on a $20,000 balance creates daily interest. |

| Loan fee | A separate charge, often deducted before funds are sent. | Federal Direct Loans may have an origination fee deducted from disbursement. |

| Total repayment cost | Principal plus interest plus fees over time. | A $20,000 loan may cost much more if repaid slowly. |

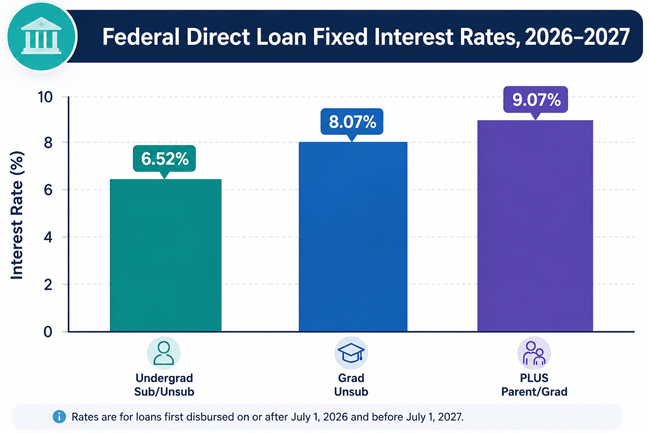

3. Current Federal Student Loan Interest Rates

Federal Direct Loan rates are set by federal law for each academic year. For loans first disbursed on or after July 1, 2026 and before July 1, 2027, Federal Student Aid announced the fixed rates shown below. These rates apply for the life of those specific loans.

| Federal Direct Loan Type | Borrower | Fixed Interest Rate for 2026-2027 |

|---|---|---|

| Direct Subsidized Loans and Direct Unsubsidized Loans | Undergraduate students | 6.52% |

| Direct Unsubsidized Loans | Graduate or professional students | 8.07% |

| Direct PLUS Loans | Parents and graduate/professional students | 9.07% |

Chart: Federal Direct Loan fixed rates for loans first disbursed July 1, 2026 through June 30, 2027. Source: Federal Student Aid electronic announcement, June 4, 2026.

A federal student loan’s rate is tied to the year the loan is first disbursed, not the year you graduate. A freshman could borrow one loan at one rate and another loan the next academic year at a different rate. Each loan keeps its own fixed rate.

4. How Student Loan Interest Rates Work

4.1 Interest Usually Accrues Daily

Most student loans calculate interest using a daily interest formula. A common formula used by federal loan servicers is:

(Current Principal Balance x Interest Rate) / 365.25 = Daily Interest

Example: Suppose your principal balance is $20,000 and your fixed rate is 6.52%. Your approximate daily interest is:

| Calculation Step | Amount |

|---|---|

| Principal balance | $20,000 |

| Interest rate | 6.52% |

| Daily interest formula | ($20,000 x 0.0652) / 365.25 |

| Approximate daily interest | $3.57 per day |

| Approximate 30-day interest | $107.10 |

4.2 Your Monthly Payment First Covers Interest

When you make a student loan payment, the servicer usually applies the payment first to unpaid interest and fees, then to principal. This matters because paying only a small amount may not reduce the balance much. Paying extra toward principal can reduce future interest, but borrowers should confirm how their servicer applies extra payments.

4.3 Interest Can Accrue While You Are in School

Whether interest accrues during school depends on the loan type. Subsidized federal undergraduate loans have a government interest benefit during certain periods. Unsubsidized loans, PLUS loans, and most private loans generally accrue interest from disbursement. If that interest is unpaid, it can increase the cost of repayment.

| Loan Type | Does Interest Usually Accrue During School? | What Borrowers Should Know |

|---|---|---|

| Federal Direct Subsidized Loan | No during eligible in-school periods | Available only to eligible undergraduate students with financial need. |

| Federal Direct Unsubsidized Loan | Yes | Interest can build while in school and during certain deferment periods. |

| Federal Direct PLUS Loan | Yes | Typically higher rates and fees than Direct Subsidized/Unsubsidized Loans. |

| Private Student Loan | Usually yes | Terms vary by lender; read the promissory note carefully. |

4.4 Capitalization Can Make Interest More Expensive

Capitalization means unpaid interest is added to your principal balance. Once interest becomes principal, future interest is calculated on a higher balance. This can happen in certain situations depending on loan type, repayment plan, deferment, forbearance, or consolidation rules. Borrowers should ask their servicer when capitalization may occur for their exact loans.

5. Fixed vs. Variable Student Loan Interest Rates

The difference between fixed and variable rates is one of the most important student loan decisions, especially for private loans.

| Feature | Fixed Interest Rate | Variable Interest Rate |

|---|---|---|

| How it works | The rate stays the same for the life of the loan. | The rate can rise or fall based on a benchmark and lender margin. |

| Payment stability | More predictable. | Payments may change over time. |

| Common with | Federal student loans and many private loans. | Private student loans and refinance loans. |

| Best for | Borrowers who want certainty and plan to repay over many years. | Borrowers who can handle payment changes and may repay quickly. |

| Main risk | Initial rate may be higher than a promotional variable rate. | Rate increases can make the loan more expensive. |

For most beginners, a fixed rate is easier to plan around. A variable rate may look cheaper at first, but it can become more expensive if market rates rise. Private lenders must disclose loan terms, but borrowers still need to compare the annual percentage rate, repayment term, cosigner obligations, and borrower protections.

6. Federal vs. Private Student Loan Interest Rates

Federal and private student loans use different systems to set interest rates. Federal rates are set by law and are the same for eligible borrowers in the same loan category and disbursement year. Private rates are set by lenders and often depend on credit history, income, school, degree program, loan term, and whether a cosigner is included.

| Category | Federal Student Loans | Private Student Loans |

|---|---|---|

| Who sets the rate? | Federal law determines rates annually. | The lender sets the rate based on underwriting and market conditions. |

| Credit check impact | Most Direct Subsidized/Unsubsidized Loans do not require traditional credit underwriting; PLUS Loans require a credit check. | Credit score, income, debt, and cosigner strength often matter. |

| Fixed or variable? | Current federal loans are fixed. | May be fixed or variable. |

| Borrower protections | May include income-driven repayment, deferment, forbearance, forgiveness programs, and federal servicing rights. | Protections vary by lender and are often more limited. |

| When to consider | Usually before private loans. | After grants, scholarships, work-study, savings, and federal options are considered. |

7. Why Student Loan Interest Rates Matter

- They affect your total cost of education, not just your monthly bill.

- They influence whether a lower monthly payment actually saves money or simply extends repayment.

- They determine how much unpaid interest can grow during school, deferment, or forbearance.

- They help you compare federal loans, private loans, refinancing offers, and repayment strategies.

- They can affect major life decisions after graduation, including housing, car purchases, career choices, and savings goals.

8. Real-World Examples of Student Loan Interest

8.1 Example 1: Undergraduate Federal Loan

Maya borrows $5,500 in a federal undergraduate Direct Loan with a 6.52% fixed rate. The loan has a predictable rate for its life. If Maya can afford small interest payments while in school, she may reduce the amount of unpaid interest that could increase her cost later, especially if part of the loan is unsubsidized.

8.2 Example 2: Graduate Borrower Comparing Grad PLUS and Private Loan

Daniel needs additional money for graduate school. A Grad PLUS Loan has a federal fixed rate and federal borrower protections, but the rate may be higher than a private offer. A private lender offers a lower variable rate with a cosigner. Daniel plans to work in public service, so he considers federal protections and possible forgiveness eligibility more valuable than a lower starting private rate.

8.3 Example 3: Parent PLUS Borrower and Total Cost

A parent borrows a PLUS Loan for a child’s final year. The rate is higher than undergraduate Direct Loan rates, and the loan may include a higher origination fee. Before borrowing, the family compares the PLUS Loan with a smaller school balance payment plan, student work income, scholarships, and a reduced housing budget. The final decision is not just about qualifying; it is about keeping long-term repayment affordable.

9. Costs and Fees Connected to Student Loan Interest Rates

Interest is not the only cost. Some student loans also have fees. Federal Direct Loans may include origination fees, which are deducted from the loan before the school receives funds. Private lenders may or may not charge origination, application, late, or other fees. Always compare the annual percentage rate and total repayment cost, not just the advertised interest rate.

| Cost | What It Means | How to Evaluate It |

|---|---|---|

| Interest rate | Annual cost of borrowing shown as a percentage. | Compare fixed vs variable and total repayment cost. |

| Origination fee | A fee charged when the loan is made, often deducted from disbursement. | Ask how much money you receive after the fee. |

| Late fee | Fee for missing or delaying payments. | Understand grace periods and autopay rules. |

| Capitalized interest | Unpaid interest added to principal. | Ask when it can happen and how to avoid it. |

| Cosigner risk | A cosigner is legally responsible if the borrower does not pay. | Understand release options and credit impact. |

10. Step-by-Step Process: How to Compare Student Loan Interest Rates

- Start with free money: scholarships, grants, employer tuition assistance, savings, and school aid.

- Complete the FAFSA if you may qualify for federal aid. Federal loans often come with protections that private loans do not match.

- List each loan offer by loan type, interest rate, fixed or variable status, fees, repayment term, and monthly payment estimate.

- Estimate the total cost, not just the first monthly payment. A longer term may lower the payment but increase total interest.

- Check whether interest accrues while you are in school and whether unpaid interest can capitalize.

- Compare borrower protections, including deferment, forbearance, income-driven repayment, forgiveness options, death/disability discharge, and cosigner release.

- Borrow only what you need. Reducing the amount borrowed is often more powerful than chasing a slightly lower rate.

- Keep records of your rates, servicer, disbursement dates, and repayment terms.

- Before refinancing federal loans, understand that refinancing into a private loan can permanently remove federal protections.

11. Benefits of Understanding Student Loan Interest Rates

- You can compare loans more accurately.

- You can avoid being misled by low introductory variable rates.

- You can decide whether paying interest during school makes sense.

- You can understand why your balance may not fall quickly at the beginning of repayment.

- You can make better decisions about refinancing, repayment plans, and extra payments.

- You can reduce financial stress by knowing what to expect before bills arrive.

12. Risks and Warnings Borrowers Should Know

- Variable rates can rise, which may increase monthly payments and total cost.

- Private loans may lack federal repayment protections.

- Capitalized interest can increase principal and make the loan more expensive.

- Long repayment terms can make a loan look affordable while increasing total interest.

- Refinancing federal loans into private loans can remove federal benefits permanently.

- A cosigner is legally responsible if the borrower cannot pay.

- Skipping payments without contacting the servicer can lead to delinquency, default, credit damage, and collection costs.

13. Expert Tips to Lower Student Loan Interest Costs

- Borrow less before searching for a lower rate. A smaller loan at a slightly higher rate may cost less than a larger loan at a lower rate.

- Pay interest while in school if you can do so without using high-interest credit cards or sacrificing basic needs.

- Use autopay carefully. It may qualify you for a rate reduction, but only if your bank balance can reliably cover payments.

- Make extra principal payments when possible and confirm with the servicer how extra payments are applied.

- Avoid extending repayment just to lower the monthly payment unless you understand the added interest cost.

- Compare private loan offers using the same repayment term so the comparison is fair.

- Keep federal loans federal unless you are certain a private refinance is worth the lost protections.

- Recheck rates and repayment options before graduate school, refinancing, or switching plans.

14. Common Mistakes to Avoid

| Mistake | Why It Hurts | Better Approach |

|---|---|---|

| Choosing the lowest starting payment only | A longer term or variable rate can cost more over time. | Compare total repayment cost. |

| Ignoring whether the rate is fixed or variable | Variable payments can rise. | Stress-test the payment if rates increase. |

| Borrowing the full amount offered | Aid offers may exceed what you truly need. | Build a school-year budget first. |

| Not reading capitalization rules | Unpaid interest can become principal. | Ask when interest can capitalize. |

| Refinancing federal loans too quickly | Federal protections may be lost. | Compare protections, not only rate. |

| Assuming all private loans are similar | Fees, release rules, and hardship options vary. | Compare multiple lenders and disclosures. |

| Missing payments instead of asking for help | Can lead to delinquency or default. | Contact the servicer before you miss payments. |

15. Quick Action Checklist

- Find every loan’s interest rate, balance, servicer, and repayment status.

- Separate federal loans from private loans.

- Identify which rates are fixed and which are variable.

- Calculate approximate daily interest for your largest loans.

- Check whether any unpaid interest may capitalize soon.

- Compare the total cost before accepting a new loan or refinance offer.

- Use autopay only if your cash flow is reliable.

- Pay extra toward the highest-rate loan when possible, while staying current on all loans.

- Contact your servicer or school financial aid office before taking action you do not understand.

16. People Also Ask: Student Loan Interest Rates FAQ

16.1 What is a student loan interest rate?

It is the annual cost of borrowing money for education. The rate determines how much interest accrues on your loan balance over time.

16.2 How are federal student loan interest rates set?

Federal Direct Loan rates are set annually under federal law using a formula tied to the 10-year Treasury note high yield plus a statutory add-on percentage.

16.3 Are federal student loan interest rates fixed?

Yes. Current federal Direct Loans have fixed rates, meaning the rate on each loan does not change for the life of that loan.

16.4 Are private student loan rates fixed or variable?

They can be either fixed or variable. Fixed rates stay the same, while variable rates can change based on market benchmarks and lender terms.

16.5 What is the current federal student loan interest rate for undergraduates?

For federal undergraduate Direct Subsidized and Direct Unsubsidized Loans first disbursed July 1, 2026 through June 30, 2027, the fixed rate is 6.52%.

16.6 What is the current graduate federal student loan interest rate?

For Direct Unsubsidized Loans to graduate and professional students first disbursed July 1, 2026 through June 30, 2027, the fixed rate is 8.07%.

16.7 What is the current Parent PLUS or Grad PLUS interest rate?

For Direct PLUS Loans first disbursed July 1, 2026 through June 30, 2027, the fixed rate is 9.07%.

16.8 Does student loan interest accrue while I am in school?

It depends on the loan. Subsidized federal loans have an interest benefit during eligible in-school periods. Unsubsidized, PLUS, and most private loans generally accrue interest while you are in school.

16.9 What is interest capitalization?

Capitalization is when unpaid interest is added to your principal balance. This can cause future interest to be calculated on a larger amount.

16.10 Is a lower interest rate always better?

Not always. A lower private rate may come with fewer protections, a variable-rate risk, cosigner obligations, or a longer term that increases total interest.

16.11 Should I pay student loan interest while in school?

Paying interest while in school can reduce total cost, especially on unsubsidized or private loans. But it should not come at the expense of necessities or high-interest debt.

16.12 Can I negotiate student loan interest rates?

Federal rates are not negotiable. Private lenders may offer different rates based on credit, income, cosigner strength, term length, and market conditions, so comparing lenders matters.

16.13 Does autopay lower student loan interest rates?

Some servicers and lenders offer an autopay rate reduction. Borrowers should confirm eligibility, dates, and terms with their servicer or lender before relying on the discount.

16.14 What is the difference between APR and interest rate?

The interest rate is the borrowing charge. APR is designed to reflect the broader annual cost of credit, including certain fees, making it useful for comparing loan offers.

16.15 Should I refinance student loans to get a lower rate?

Refinancing may help borrowers with strong credit and stable income, but refinancing federal loans into private loans can permanently remove federal protections. Compare the trade-off carefully.

17. Conclusion: The Smart Way to Think About Student Loan Interest

Student loan interest rates are not just financial fine print. They shape the true cost of college debt, the size of future payments, and the flexibility you have if life does not go exactly as planned. A borrower who understands fixed vs. variable rates, daily interest, capitalization, fees, and repayment terms is in a much stronger position than someone who only looks at the monthly payment.

The best practice is to borrow as little as reasonably possible, use federal options before private loans in most cases, compare total costs, and avoid giving up borrower protections without a clear reason. When you are unsure, ask your school’s financial aid office, your loan servicer, or a qualified financial counselor before signing or refinancing.

A student loan can help open the door to education, but the interest rate determines how expensive that door becomes. The more you understand before borrowing, the more control you have after graduation.

17.1 Sources Consulted

- Federal Student Aid, U.S. Department of Education: Interest Rates for Federal Direct Loans First Disbursed Between July 1, 2026 and June 30, 2027, posted June 4, 2026.

- Federal Student Aid, U.S. Department of Education: Federal Student Loan Interest Rates page.

- Consumer Financial Protection Bureau: “What are the interest rates on my student loans?” last reviewed September 5, 2024.

- Consumer Financial Protection Bureau: “What are private student loans?” last reviewed May 14, 2024.

- Consumer Financial Protection Bureau: “What student loan option is best for me: federal student loans or private student loans?” last reviewed May 28, 2024.

- Federal student loan servicer educational materials on daily interest accrual, capitalization, and payment allocation.

Reader Advice: This article is for general educational and informational purposes only and does not constitute individualized financial, legal, tax, accounting, or investment advice. Loan rates, APRs, fees, eligibility, underwriting standards, credit reporting practices, and applicable laws may vary by lender, loan type, borrower profile, location, and current regulations.

Always review the official loan agreement and disclosures, compare offers based on APR, fees, monthly payments, and total repayment cost, and verify current terms with the lender, loan servicer, StudentAid.gov, the SBA, or other relevant official sources when applicable.

If you need advice for your specific situation, especially involving debt disputes, lawsuits, foreclosure, wage garnishment, bankruptcy, or tax matters, consult a qualified financial professional, nonprofit credit counselor, tax adviser, accountant, consumer attorney, or legal aid organization.