Best SBA Loan Alternatives for Small Businesses

SBA loans are popular because they can offer longer repayment terms, competitive rates, and flexible uses. But they are not always the fastest, easiest, or most realistic choice for every small business. Many owners need funding before an SBA application can be approved, do not meet SBA eligibility requirements, lack sufficient documentation, or simply need a financing product better matched to short-term cash flow.

This guide explains the best SBA loan alternatives for small businesses in plain English. It is written for owners who want practical financing options, not vague promises. You will learn what each option is, how it works, when it makes sense, what it may cost, what can go wrong, and how to compare choices before signing an agreement.

Small business financing can affect cash flow, taxes, credit, ownership control, and the long-term stability of your company. The best alternative to an SBA loan is not always the lowest advertised rate. It is the option that matches your use of funds, repayment ability, timeline, collateral, business stage, and risk tolerance.

1. What Are SBA Loan Alternatives?

SBA loan alternatives are financing options that do not rely on a U.S. Small Business Administration guarantee. They may come from banks, credit unions, community development financial institutions, online lenders, factoring companies, equipment finance companies, grant programs, investors, crowdfunding platforms, or even vendors and suppliers.

An SBA 7(a) loan is the SBA’s primary business loan program and can be used for purposes such as working capital, refinancing business debt, buying equipment, improving real estate, purchasing supplies, or business acquisition. The SBA states that the maximum 7(a) loan amount is $5 million and that borrowers apply through participating lenders, not directly through the SBA. SBA microloans are separate smaller loans of up to $50,000 made through nonprofit intermediary lenders.

Because SBA loans involve lender underwriting and program rules, they can require time, documentation, acceptable credit, repayment capacity, and eligible use of funds. If your business cannot wait, cannot qualify, or does not need a full SBA structure, an alternative may be more practical.

1.1 Why Small Businesses Look for Alternatives to SBA Loans

- You need funds quickly for payroll, inventory, repairs, or a time-sensitive opportunity.

- Your business is new and has limited operating history.

- Your credit profile, collateral, cash flow, or industry creates approval challenges.

- You need a revolving credit line rather than a lump-sum term loan.

- You want financing tied to a specific asset, invoice, purchase order, or revenue stream.

- You were denied for an SBA loan and need a realistic next step.

- You want to avoid a lengthy application or heavy documentation package.

2. Best SBA Loan Alternatives at a Glance

| Alternative | Best for | Typical strength | Main caution |

|---|---|---|---|

| Traditional bank term loan | Established businesses with strong credit and cash flow | Often competitive pricing and predictable payments | Approval can still be strict and slow |

| Business line of credit | Recurring working capital needs and uneven cash flow | Borrow, repay, and reuse funds as needed | Rates may be variable and limits can be reduced |

| Credit union or community bank loan | Local businesses with relationship-based banking needs | Personalized underwriting and local knowledge | May have smaller loan limits or geographic restrictions |

| CDFI or nonprofit lender loan | Underserved communities, startups, thinner credit files | Mission-focused support and business coaching | Funding amounts may be limited |

| Equipment financing | Vehicles, machinery, tools, technology, or fixtures | Equipment often serves as collateral | Less useful for general working capital |

| Invoice financing or factoring | B2B companies with unpaid invoices | Turns receivables into cash faster | Fees reduce margins and customer handling matters |

| Merchant cash advance | Card-heavy businesses needing very fast cash | Fast approval and sales-based collection | Often expensive and risky if sales fall |

| Business credit cards | Small purchases and short-term float | Convenient and useful for rewards or emergencies | High APR if balances are carried |

| Grants | Businesses that qualify for public, nonprofit, or industry programs | Non-dilutive funds that may not require repayment | Competitive, restrictive, and rarely immediate |

| Crowdfunding | Consumer-facing products, community support, pre-sales | Can validate demand and raise visibility | Requires marketing effort and may not fund |

| Revenue-based financing | Growing companies with recurring revenue | Payments adjust with revenue | Can be costly and may reduce growth cash flow |

| Vendor or supplier financing | Inventory, materials, or operating supplies | Can preserve cash without a formal loan | Late payments may damage supplier relationships |

3. How SBA Loan Alternatives Work

Most alternatives fall into one of four categories: debt, asset-based financing, revenue-based financing, or non-debt funding. Understanding the category helps you compare risk instead of focusing only on the monthly payment.

| Category | How it works | Examples | Key question to ask |

|---|---|---|---|

| Debt financing | You borrow money and repay principal plus interest or fees over time. | Term loans, lines of credit, credit cards, CDFI loans | Can my cash flow support the payment even in a slow month? |

| Asset-based financing | Funding is tied to an asset such as equipment, invoices, or inventory. | Equipment financing, invoice factoring, inventory financing | What happens if the asset loses value or customers pay late? |

| Revenue-based financing | Repayment is linked to sales or revenue, often daily, weekly, or monthly. | Merchant cash advances, revenue-based financing | What is the real cost if sales are lower or higher than expected? |

| Non-debt funding | You may receive money without traditional repayment, but there may be restrictions or tradeoffs. | Grants, crowdfunding, equity investment | What obligations, reporting, ownership dilution, or delivery promises come with the money? |

2. The Best SBA Loan Alternatives

2.1 Traditional Bank Term Loans

A traditional bank term loan provides a lump sum that is repaid over a fixed schedule. It can be used for expansion, renovation, inventory, refinancing, or large planned purchases. For a well-established business with strong financial statements, a bank loan may be the closest non-SBA substitute.

How it works

The lender reviews business revenue, profitability, credit history, debt obligations, tax returns, bank statements, collateral, and the purpose of the loan. If approved, you receive funds upfront and repay them in monthly installments.

Best for

- Businesses with at least a few years of operating history.

- Owners with strong personal and business credit.

- Borrowers who can document stable revenue and repayment capacity.

- Projects with a clear return on investment.

Pros and cons

| Pros | Cons |

|---|---|

| Predictable repayment schedule | Can be difficult for startups or weaker credit profiles |

| Potentially lower cost than many online alternatives | May require collateral or a personal guarantee |

| Good fit for planned investments | Approval and funding may take time |

| Can build business credit when reported | Documentation can be extensive |

2.2 Business Line of Credit

A business line of credit is one of the most flexible SBA loan alternatives. Instead of receiving one lump sum, you get access to a credit limit and draw only what you need. You pay interest on the amount used, not usually on the full limit.

How it works

The lender approves a maximum credit limit. You draw funds for short-term needs, repay the balance, and may borrow again during the draw period. Lines of credit may be secured or unsecured, revolving or non-revolving, and bank-based or online.

Best for

- Seasonal businesses with uneven cash flow.

- Companies that need a safety net for payroll, inventory, repairs, or receivables gaps.

- Owners who do not know the exact amount they will need.

Example

A landscaping company has strong spring and summer revenue but slower winter cash flow. Instead of taking a large term loan, it opens a line of credit to cover winter payroll and equipment maintenance. When customer payments arrive, it pays the line down and keeps the limit available for the next seasonal gap.

2.3 Credit Union or Community Bank Loans

Credit unions and community banks can be useful alternatives for borrowers who value local relationships. These lenders may understand regional businesses better than national institutions and may offer more personal service.

Best for

- Local service businesses, retailers, contractors, and professional firms.

- Owners who already maintain deposits with the institution.

- Borrowers who want a relationship lender rather than a purely automated decision.

Reader Advice

Bring a concise loan package even if the lender says the conversation is informal. Include a one-page use-of-funds summary, recent profit-and-loss statement, balance sheet, bank statements, tax returns, and a realistic repayment explanation. Good preparation makes relationship lending easier.

2.4 CDFI and Nonprofit Small Business Loans

Community Development Financial Institutions, nonprofit lenders, and mission-driven community lenders may serve businesses that have trouble qualifying for conventional bank credit. They often focus on underserved communities, smaller loan sizes, technical assistance, and business education.

How it works

A CDFI or nonprofit lender reviews your business model, community impact, cash flow, credit, and ability to repay. Some programs pair financing with coaching, bookkeeping help, marketing support, or financial management training.

Best for

- Startups and very small businesses.

- Borrowers with limited collateral or imperfect credit.

- Businesses in low-income or underserved areas.

- Owners who need guidance along with capital.

Main caution

Mission-driven lenders are not grants. They still expect repayment. Loan amounts may be smaller, and the process may include coaching milestones or documentation requirements.

2.5 Equipment Financing

Equipment financing helps businesses buy vehicles, machinery, computers, medical equipment, restaurant equipment, construction tools, or other business assets. The equipment itself often serves as collateral, which can make approval easier than an unsecured loan.

How it works

The lender or finance company pays for the equipment, and the borrower repays the cost over time with interest or lease payments. In a loan structure, you typically own the equipment after repayment. In a lease structure, you may return it, renew the lease, or buy it depending on the contract.

Best for

- Businesses buying revenue-producing equipment.

- Companies that want to preserve cash.

- Borrowers who can show the equipment will improve productivity, capacity, or revenue.

Example

A bakery needs a commercial oven costing $35,000. Instead of using all cash or applying for an SBA loan, it finances the oven. If the oven increases daily production and wholesale orders, the added revenue may help cover the payment. The owner should still test the numbers using conservative sales assumptions.

2.6 Invoice Financing and Invoice Factoring

Invoice financing and factoring help B2B businesses unlock cash tied up in unpaid customer invoices. These options are common for companies whose customers pay in 30, 45, 60, or 90 days but whose expenses are due sooner.

How it works

With invoice financing, you borrow against outstanding invoices and repay when customers pay. With invoice factoring, you typically sell invoices to a factoring company at a discount. The factor may collect payment directly from your customer, depending on the arrangement.

Best for

- B2B companies with creditworthy customers.

- Wholesalers, staffing firms, trucking companies, manufacturers, agencies, and suppliers.

- Businesses with strong invoices but short-term cash gaps.

Main caution

Invoice financing can be useful, but fees reduce margins. Customer experience also matters. If the financing company contacts your customers, make sure its collection process is professional and consistent with your brand.

2.7 Merchant Cash Advance

A merchant cash advance, or MCA, provides cash upfront in exchange for a portion of future sales or revenue. It is often marketed to businesses with heavy card sales, such as restaurants, salons, retailers, repair shops, and service businesses.

How it works

Instead of a traditional interest rate, MCAs commonly use a factor rate or fixed repayment amount. Payments may be collected daily or weekly from card sales or bank deposits. This can make funding fast, but the effective cost can be high, especially when repayment happens quickly.

When it may make sense

- A true emergency where cheaper financing is unavailable.

- A short-term opportunity with a clear, immediate return.

- A business with volatile sales that understands the repayment mechanics.

Major warning

The Federal Trade Commission has taken action against merchant cash advance providers for deceptive and unfair practices, and state regulators have warned small businesses about unfair, deceptive, or abusive MCA conduct. An MCA should be treated as a high-risk option, not a routine working capital tool.

2.8 Business Credit Cards

Business credit cards can be useful for small purchases, travel, subscriptions, emergency repairs, and short-term cash timing. They are not a good substitute for long-term financing if you expect to carry a balance.

Best for

- Small recurring expenses.

- Short-term float that will be repaid quickly.

- Separating business and personal expenses.

- Earning rewards when spending is controlled.

Main caution

Credit card APRs can be high. If you need months or years to repay, a term loan or line of credit may be safer. Also watch annual fees, cash advance fees, penalty APRs, and personal guarantees.

2.9 Small Business Grants

A grant is funding that generally does not require repayment if you follow the rules. Grants may come from government agencies, economic development groups, nonprofits, corporations, universities, or industry programs.

Best for

- Research, innovation, exporting, energy efficiency, workforce development, training, rural development, and community impact projects.

- Businesses that can meet eligibility rules and reporting requirements.

- Owners who do not need immediate cash.

Reality check

Grants are attractive because they may not need to be repaid, but they are competitive and often restricted. They rarely solve urgent payroll or working capital problems. Treat grants as strategic funding, not emergency financing.

2.10 Crowdfunding

Crowdfunding allows a business to raise money from many supporters. Common models include rewards-based crowdfunding, donation-based crowdfunding, debt crowdfunding, and equity crowdfunding.

Best for

- Consumer products with strong storytelling potential.

- Local businesses with loyal community support.

- Creative projects, pre-sales, or mission-driven campaigns.

Main caution

Crowdfunding is not free money. You may need to create campaign assets, market aggressively, deliver rewards, pay platform fees, handle taxes, and manage customer expectations.

2.11 Revenue-Based Financing

Revenue-based financing provides capital in exchange for a percentage of future revenue until a fixed repayment cap is reached. It is often used by businesses with recurring revenue, software companies, e-commerce brands, and subscription businesses.

Best for

- Companies with predictable monthly revenue.

- Businesses that do not want to give up equity.

- Growth investments such as marketing, inventory, or expansion with measurable returns.

Main caution

Payments tied to revenue may feel flexible, but the total repayment amount can still be expensive. Compare the repayment cap, payment frequency, expected payoff time, and impact on cash flow.

2.12 Vendor Financing and Trade Credit

Vendor financing, supplier terms, and trade credit allow a business to receive goods or services now and pay later. Common terms include net 15, net 30, net 60, or installment plans for inventory and supplies.

Best for

- Inventory purchases.

- Routine supplies.

- Businesses with reliable sales cycles.

- Owners who want to preserve cash without applying for a loan.

Reader Advice

Ask vendors whether they report positive payment history to business credit bureaus. Responsible trade credit can help strengthen a business credit profile, but late payments can damage supplier relationships quickly.

3. Comparison: SBA Loan vs. Common Alternatives

| Feature | SBA loan | Bank term loan | Line of credit | Equipment financing | Invoice financing | MCA |

|---|---|---|---|---|---|---|

| Primary use | Broad business purposes | Planned investment | Working capital gaps | Asset purchase | Cash tied in invoices | Fast cash against sales |

| Speed | Often slower | Moderate to slow | Moderate to fast | Moderate | Fast | Very fast |

| Documentation | High | Moderate to high | Moderate | Moderate | Invoice/customer focused | Often lighter |

| Cost potential | Often competitive | Competitive for strong borrowers | Variable | Moderate | Fee-based | Often high |

| Collateral | May be required | Often required | May be required | Equipment | Invoices | Future sales/deposits |

| Best borrower | Qualified business with time to apply | Established business | Business with recurring cash gaps | Needs equipment | B2B invoices | Urgent need, limited options |

| Main risk | Delay or denial | Strict underwriting | Overuse and variable rates | Asset repossession | Margin compression | Cash flow strain |

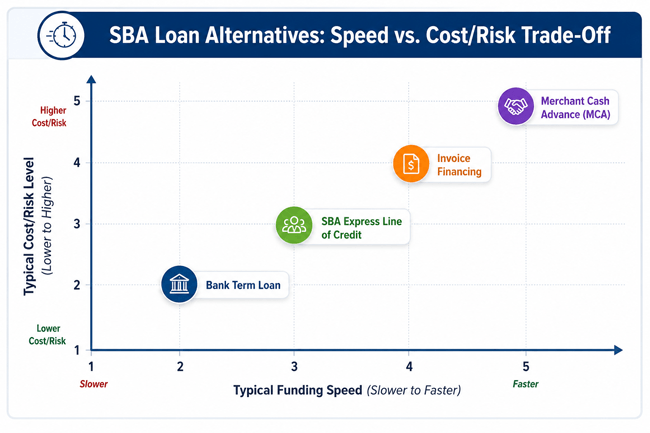

Figure: Higher speed often comes with higher cost or risk. This chart is a general decision aid, not a quote or guarantee.

4. How to Choose the Best SBA Loan Alternative

Choosing the best alternative starts with the business problem, not the product name. A loan that is excellent for buying equipment may be wrong for covering payroll. A fast advance that solves a one-week emergency may be dangerous if daily payments drain cash for months.

Step-by-Step Process

- Define the exact use of funds. Write down whether the money is for working capital, equipment, inventory, invoices, marketing, payroll, refinancing, expansion, or emergency expenses.

- Calculate how much you truly need. Borrowing too little may not solve the problem; borrowing too much may create unnecessary cost.

- Match repayment to the benefit period. Long-term assets can justify longer repayment. Short-term inventory or receivables should usually be financed with short-term tools.

- Estimate conservative cash flow. Use a slow-sales scenario, not only your best month, to test whether payments are affordable.

- Compare total cost, not only monthly payment. Include interest, origination fees, draw fees, maintenance fees, factor rates, late fees, prepayment penalties, and required insurance.

- Check collateral and personal guarantee requirements. Understand what assets or personal obligations are at risk.

- Review the contract carefully. Look for daily repayment, confession of judgment language, blanket liens, automatic renewals, minimum usage fees, and default triggers.

- Apply to the best-fit options first. Too many scattered applications can waste time and may affect credit if hard inquiries occur.

- Build a backup plan. Decide what you will do if revenue drops, invoices are late, or the funding arrives after the opportunity passes.

5. Costs and Fees to Compare

Financing cost is more than the stated rate. Some products use APR, some use simple interest, some use factor rates, and some quote fees as a percentage of invoices or daily sales. Ask every provider to show the total dollar cost and payment schedule before you sign.

| Cost or fee | Where it appears | Why it matters |

|---|---|---|

| Interest rate or APR | Term loans, lines of credit, credit cards | Helps compare annualized borrowing cost |

| Origination fee | Bank, online, and some term loans | Reduces net proceeds or increases total cost |

| Draw fee | Lines of credit | Charged when funds are drawn |

| Maintenance or unused line fee | Lines of credit | Can apply even if you do not borrow |

| Factor fee or discount fee | Invoice factoring and MCAs | Can obscure the effective annual cost |

| Late payment fee | Most debt products | Signals cash-flow risk if payments are tight |

| Prepayment penalty | Some loans and leases | Can make early payoff less valuable |

| Broker fee | Brokered financing | May increase cost or create conflicts of interest |

| UCC filing fee | Secured loans and lines | Indicates a lien on business assets |

| Legal or documentation fee | Some commercial loans | Adds closing cost and should be disclosed |

6. Real-World Financing Scenarios

Scenario 1: Restaurant Needs Emergency Repairs

A restaurant’s walk-in cooler fails before a busy weekend. An SBA loan is too slow. The owner compares a business credit card, equipment financing, and a merchant cash advance. Equipment financing may be best if the cooler is expensive and the vendor can install quickly. A credit card may work if the repair is small and can be paid off within the billing cycle. An MCA may fund quickly, but daily payments could hurt cash flow during slow weeks.

Scenario 2: Consulting Firm Has $80,000 in Unpaid Invoices

A consulting firm is profitable but waits 60 days for corporate clients to pay. A term loan may add unnecessary debt. Invoice financing could convert part of the receivables into cash while matching repayment to customer payments. The owner should compare fees and confirm whether clients will be contacted.

Scenario 3: Startup Retail Brand Is Not Ready for a Bank Loan

A new retail brand has early sales but limited operating history. A bank loan may be unlikely. The founder considers crowdfunding, vendor terms, a small CDFI loan, and a business credit card for controlled purchases. The best mix may be crowdfunding for demand validation, vendor terms for inventory, and a small credit line once revenue becomes consistent.

Scenario 4: Contractor Needs a Truck

A contractor needs a reliable truck to accept larger jobs. Equipment or vehicle financing may be more appropriate than a general working capital loan because the asset supports revenue and can serve as collateral. The contractor should compare down payment, term, insurance requirements, mileage limits if leased, and resale value.

7. Benefits of Using SBA Loan Alternatives

- Faster access to funds for urgent needs.

- More flexible qualification paths for startups, thin credit files, or asset-rich businesses.

- Products tailored to specific needs such as invoices, equipment, inventory, or seasonal cash flow.

- Potential to build banking relationships and business credit.

- Less paperwork in some cases compared with SBA loan applications.

- Ability to use multiple funding tools strategically instead of relying on one large loan.

8. Risks and Drawbacks to Consider

- Higher cost: Some online loans, MCAs, invoice products, and credit cards can cost significantly more than SBA-backed financing.

- Cash-flow pressure: Daily, weekly, or short-term payments can strain operations.

- Personal liability: Many products require a personal guarantee, even when marketed as business financing.

- Collateral risk: Secured loans can put equipment, inventory, receivables, or broader business assets at risk.

- Contract complexity: Factor rates, holdbacks, default clauses, liens, and renewal terms can be confusing.

- Overborrowing: Easy access to fast capital can hide an underlying profitability or pricing problem.

- Customer relationship risk: Invoice factoring may involve third-party contact with customers.

9. Common Mistakes to Avoid

| Mistake | Why it hurts | How to avoid it |

|---|---|---|

| Choosing the fastest offer without comparing cost | Speed can hide expensive repayment terms | Get at least two or three comparable quotes when possible |

| Confusing factor rate with APR | A low-looking factor rate may still be costly | Ask for total dollar cost and estimated APR |

| Borrowing for losses instead of fixing operations | Debt can delay, not solve, a margin problem | Review pricing, expenses, and cash conversion cycle |

| Using long-term debt for short-term needs or vice versa | Mismatch can create cash flow stress | Match repayment term to the useful life of the purchase |

| Ignoring personal guarantees and liens | Owner assets may be at risk | Read security agreements and guarantee language |

| Not checking prepayment rules | Early payoff may not save as much as expected | Ask how payoff is calculated before signing |

| Stacking multiple advances | Payments can become unmanageable | Consolidate only with a clear cash-flow plan |

| Failing to prepare documents | Weak preparation slows approval | Keep financial statements, tax returns, and bank statements organized |

| Treating grants as immediate funding | Grant timelines and restrictions can be long | Use grants as strategic funding, not emergency cash |

| Not asking why an SBA loan was denied | You may repeat the same issue elsewhere | Request the reason and fix credit, cash flow, documentation, or collateral gaps |

10. Expert Tips for Safer Small Business Financing

- Build a financing stack. Use a line of credit for short-term working capital, equipment financing for equipment, and grants or crowdfunding for specific eligible projects.

- Know your break-even payment. Calculate the maximum monthly payment your business can afford after payroll, rent, taxes, inventory, and owner compensation.

- Ask for the all-in cost in dollars. A clear lender should be able to show how much you receive, how much you repay, and when payments are due.

- Protect your cash conversion cycle. If customers pay in 60 days, avoid repayment structures that drain cash daily unless margins are strong.

- Keep clean financial records. Better bookkeeping improves approval odds and helps you avoid borrowing blindly.

- Use financing for growth or stability, not avoidance. If the business is consistently losing money, fix the operating problem before adding debt.

- Watch for pressure tactics. Be cautious if a provider pushes same-day signing, discourages legal review, or will not explain fees plainly.

- Build relationships before you need money. Banks, credit unions, CDFIs, vendors, and local business centers are easier to work with before a crisis.

11. Quick Action Checklist

- Write down the exact funding need and deadline.

- Separate urgent needs from strategic growth needs.

- Calculate the amount required and the maximum affordable payment.

- Gather bank statements, tax returns, profit-and-loss statements, balance sheet, accounts receivable aging, and debt schedule.

- Check personal and business credit reports for errors.

- Compare at least three options by total dollar cost, payment frequency, term, collateral, and guarantee requirements.

- Ask whether the rate is APR, simple interest, discount fee, or factor rate.

- Read default clauses, renewal terms, lien language, and prepayment provisions.

- Confirm how quickly funds are available and whether there are conditions before funding.

- Choose the option that solves the business problem with the least long-term risk.

12. Frequently Asked Questions

12.1 What is the best alternative to an SBA loan?

The best alternative depends on your need. A bank term loan may be best for established businesses, a line of credit for recurring working capital, equipment financing for asset purchases, invoice financing for unpaid B2B invoices, and CDFI financing for borrowers who need flexible underwriting.

12.2 What can I do if I was denied for an SBA loan?

Ask the lender for the reason, then address the gap. Common next steps include improving documentation, reducing debt, strengthening cash flow, applying with a CDFI, using equipment or invoice financing, or building credit before reapplying.

12.3 Are SBA loan alternatives more expensive?

Many are more expensive than SBA-backed loans, but not always. Strong borrowers may qualify for competitive bank or credit union loans. Fast funding products, merchant cash advances, and some online loans can be significantly costlier.

12.4 What is the fastest alternative to an SBA loan?

Merchant cash advances, invoice financing, some online lines of credit, and business credit cards are often faster than traditional loans. Speed should be weighed against total cost and repayment pressure.

12.5 Can a startup get an SBA loan alternative?

Yes. Startups may consider CDFI loans, microloans, business credit cards, crowdfunding, grants, vendor financing, equipment financing, or personal investment. Options depend on credit, collateral, revenue, and the strength of the business plan.

12.6 Which alternative is best for bad credit?

CDFI loans, secured equipment financing, invoice factoring, and some revenue-based products may be more accessible than bank loans. However, bad-credit financing can be expensive, so compare total cost carefully.

12.7 Is invoice financing better than a business loan?

Invoice financing can be better when the problem is delayed customer payment rather than a long-term need. It is less ideal if your margins are thin, customers are unreliable, or you need funds unrelated to receivables.

12.8 Is a merchant cash advance a loan?

Many MCAs are structured as purchases of future receivables rather than traditional loans. Regardless of the legal structure, they function like financing and can place heavy pressure on cash flow.

12.9 Are grants a realistic SBA loan alternative?

Grants can help, but they are not usually a direct substitute for a loan. They are competitive, restricted, and slow. They work best for eligible projects, not immediate working capital emergencies.

12.10 Should I use a business credit card instead of a loan?

A business credit card can work for small short-term expenses that you can repay quickly. It is risky for long-term financing because interest costs can rise quickly when balances are carried.

12.11 What is the safest small business financing option?

The safest option is the one with affordable payments, transparent terms, a clear use of funds, and no unnecessary collateral or personal risk. For many established businesses, this may be a bank loan or line of credit. For asset purchases, equipment financing may be safer.

12.12 How do I compare a factor rate to an interest rate?

Ask the provider for the total dollar repayment, payment frequency, expected payoff time, and estimated APR. A factor rate does not show time value clearly, so it can make short-term financing look cheaper than it is.

12.13 Can I combine multiple SBA loan alternatives?

Yes, but do it carefully. A business may use vendor terms for inventory, a line of credit for seasonal gaps, and equipment financing for machinery. Avoid stacking high-cost advances without a repayment plan.

12.14 Do SBA loan alternatives require a personal guarantee?

Many do. Even when financing is for a business, lenders may require the owner to personally guarantee repayment. Always read the guarantee language before signing.

12.15 When should I wait and apply for an SBA loan instead?

Consider waiting if you qualify, your funding need is not urgent, and you want longer terms or potentially lower cost. SBA loans may be worth the process for major expansion, real estate, business acquisition, or large working capital needs.

13. Conclusion: Choose Financing That Fits the Business Problem

SBA loans can be excellent tools, but they are not the only path to small business funding. The best SBA loan alternative depends on why you need money, how quickly you need it, how predictable your cash flow is, what assets or invoices you can finance, and how much risk you are willing to accept.

For established businesses, bank loans, credit union loans, and lines of credit may be strong substitutes. For asset purchases, equipment financing can be more targeted. For B2B receivables, invoice financing may solve timing gaps. For underserved or newer businesses, CDFIs and nonprofit lenders may offer a more realistic starting point. Grants and crowdfunding can help in the right situation, while merchant cash advances should be approached with caution because speed can come with high cost and repayment stress.

The most practical next step is to define the funding problem, calculate the affordable payment, compare total cost, read the contract, and choose the least risky option that actually solves the need. Good financing should strengthen your business, not trap it.

13.1 Sources Consulted

- U.S. Small Business Administration. 7(a) Loans. https://www.sba.gov/funding-programs/loans/7a-loans

- U.S. Small Business Administration. Microloans. https://www.sba.gov/funding-programs/loans/microloans

- U.S. Small Business Administration. Loans. https://www.sba.gov/funding-programs/loans

- U.S. Small Business Administration. Types of 7(a) Loans. https://www.sba.gov/partners/lenders/7a-loan-program/types-7a-loans

- Federal Trade Commission. Protecting small businesses seeking financing. https://www.ftc.gov/business-guidance/blog/2020/08/protecting-small-businesses-seeking-financing-during-pandemic

- Federal Trade Commission. Merchant cash advance providers banned from industry. https://www.ftc.gov/news-events/news/press-releases/2022/01/merchant-cash-advance-providers-banned-industry-ordered-redress-small-businesses

- Consumer Financial Protection Bureau. Small business lending rulemaking. https://www.consumerfinance.gov/1071-rule/

- California Department of Financial Protection and Innovation. Advisory to small businesses about merchant cash advances. https://dfpi.ca.gov/alert/advisory-to-small-businesses-speak-up-about-merchant-cash-advances/

Reader Advice: This article is for general educational and informational purposes only and does not constitute individualized financial, legal, tax, accounting, or investment advice. Loan rates, APRs, fees, eligibility, underwriting standards, credit reporting practices, and applicable laws may vary by lender, loan type, borrower profile, location, and current regulations.

Always review the official loan agreement and disclosures, compare offers based on APR, fees, monthly payments, and total repayment cost, and verify current terms with the lender, loan servicer, StudentAid.gov, the SBA, or other relevant official sources when applicable.

If you need advice for your specific situation, especially involving debt disputes, lawsuits, foreclosure, wage garnishment, bankruptcy, or tax matters, consult a qualified financial professional, nonprofit credit counselor, tax adviser, accountant, consumer attorney, or legal aid organization.