Best Small Business Loans

Choosing the best small business loan is not just about finding the lowest advertised interest rate. The best loan is the one that fits your business purpose, cash flow, credit strength, repayment ability, timeline, and risk tolerance. A loan that helps one business grow can strain another business if payments arrive before the borrowed money produces results.

Small business owners usually look for financing when they need working capital, want to buy equipment, plan to expand, need to cover seasonal gaps, or are trying to survive a difficult cash-flow period. The decision matters because loan terms affect profit, flexibility, ownership, and sometimes personal assets. Many business loans require a personal guarantee, collateral, or automatic payments from a business bank account. That means the “best” loan must be judged by total cost, repayment structure, lender reliability, and whether the loan actually solves the business problem.

This guide is for beginners, new business owners, freelancers, local shop owners, service businesses, online sellers, contractors, and growing companies that want practical guidance before applying. It explains the main loan options, how they work, when each one makes sense, what costs to compare, how to prepare an application, and what mistakes to avoid.

1. What Is a Small Business Loan?

A small business loan is borrowed money that a business receives from a lender and repays over time, usually with interest and fees. The money may come from a bank, credit union, online lender, nonprofit lender, community development financial institution, equipment finance company, invoice finance company, or an SBA-approved lender.

Small business loans can be used for many legitimate business purposes, including inventory, payroll, equipment, marketing, repairs, expansion, real estate, refinancing business debt, and short-term operating expenses. Some loans are general-purpose, while others are tied to a specific asset or need.

2. Best Small Business Loans at a Glance

| Loan Type | Best For | Typical Strength | Main Caution |

|---|---|---|---|

| SBA 7(a) loan | Established businesses that need flexible funding | Large loan amounts, longer terms, broad use of funds | Can take longer and requires strong documentation |

| SBA 504 loan | Commercial real estate, major equipment, expansion projects | Long-term fixed-rate financing for major assets | Not designed for ordinary working capital |

| SBA microloan | Startups, very small businesses, community-based borrowers | Smaller loans with technical assistance | Loan amounts are limited |

| Bank or credit union term loan | Profitable businesses with strong credit and financial records | Competitive rates and stable repayment schedule | Harder to qualify for than many online options |

| Business line of credit | Seasonal cash flow, short-term gaps, emergency flexibility | Borrow only what you need up to a limit | Variable rates and fees can add up |

| Equipment financing | Buying vehicles, machinery, computers, or tools | Equipment often serves as collateral | Loan may outlast the useful life of the asset |

| Invoice financing | B2B businesses waiting on customer payments | Turns unpaid invoices into faster cash | Costs can be high if customers pay slowly |

| Online term loan | Fast funding for businesses that cannot wait | Speed and easier access | Often more expensive than bank or SBA financing |

| Merchant cash advance | Businesses with card sales and no better options | Fast cash with flexible remittance tied to sales | Can be very costly and risky; compare carefully |

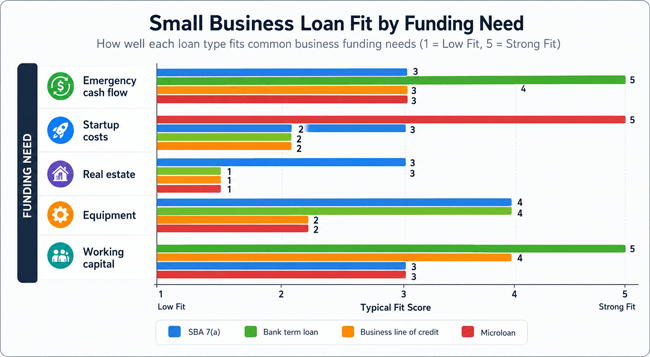

3. Chart: Which Loan Fits Which Business Need?

The chart below is a practical decision aid. It is not a guarantee of approval or cost. A higher score means the loan type is commonly a stronger fit for that funding need, assuming the borrower qualifies.

4. How Small Business Loans Work

Most small business loans follow a basic process: the business applies, the lender reviews risk, the lender approves or denies the request, funds are disbursed, and the borrower repays according to the agreement. What changes from one loan to another is how the lender evaluates the business and how repayment is structured.

- You identify a clear funding purpose, such as inventory, payroll, equipment, or expansion.

- You estimate the amount needed and compare it with what the business can safely repay.

- You choose a loan type and lender that match the purpose, timeline, and qualifications.

- You submit an application with financial statements, tax returns, bank statements, ownership information, and sometimes a business plan.

- The lender evaluates credit, revenue, cash flow, debt, collateral, industry risk, and time in business.

- If approved, you review the offer, including APR, term, fees, repayment frequency, collateral, default rules, and personal guarantee language.

- After funding, you use the money for the stated purpose and make payments until the loan is repaid.

5. Why Finding the Best Small Business Loan Matters

Business financing can create growth, stability, and opportunity. It can also create pressure if payments are too high or the loan is used for the wrong problem. The Federal Reserve Small Business Credit Survey reported that many employer firms sought financing for operating expenses or expansion opportunities, and not all applicants received the full amount they requested. This shows why preparation, realistic expectations, and careful loan selection matter.

The right loan can help a business buy productive assets, smooth cash flow, accept larger orders, hire staff, or refinance expensive debt. The wrong loan can drain cash, force repeated borrowing, or put personal assets at risk.

6. Main Types of Small Business Loans

6.1 SBA 7(a) Loans

SBA 7(a) loans are among the most well-known small business financing options in the United States. The SBA does not usually lend directly; instead, it sets loan guidelines and reduces lender risk through a government guarantee. According to the SBA, the maximum 7(a) loan amount is $5 million. These loans may be used for working capital, equipment, business acquisition, expansion, refinancing certain debt, and other approved business purposes.

Best for: established businesses that want flexible use of funds and can handle a documentation-heavy application.

Not ideal for: borrowers who need money immediately, cannot document revenue, or do not meet SBA/lender eligibility standards.

6.2 SBA 504 Loans

SBA 504 loans are designed for major fixed assets that support business growth and job creation. They are commonly used for owner-occupied commercial real estate, major building improvements, and heavy equipment. The SBA states that the maximum 504 loan amount is generally $5.5 million. These loans are offered through Certified Development Companies and participating lenders.

Best for: buying or improving major fixed assets such as property or long-life equipment.

Not ideal for: routine working capital, inventory, marketing, or payroll needs.

6.3 SBA Microloans

SBA microloans provide smaller loans through nonprofit intermediary lenders. The SBA says microloans can be up to $50,000 and are intended to help small businesses and certain nonprofit childcare centers start up and expand. Microloans can be especially helpful for startups, underserved borrowers, and very small businesses that need modest capital plus guidance.

Best for: small startup costs, inventory, supplies, furniture, fixtures, or working capital.

Not ideal for: large expansion projects or borrowers who need more than the program limit.

6.4 Traditional Bank or Credit Union Term Loans

A term loan gives a business a lump sum that is repaid over a set period. Banks and credit unions may offer competitive pricing to businesses with strong credit, steady revenue, profitability, and organized records. These loans are often used for expansion, equipment, inventory, refinancing, or long-term working capital.

Best for: established businesses with strong financial statements and enough time to complete a standard application.

Not ideal for: very new businesses, owners with poor credit, or businesses with unstable cash flow.

6.5 Business Lines of Credit

A business line of credit works more like a flexible borrowing limit than a one-time loan. You can draw funds when needed, repay them, and borrow again up to the approved limit. Lines of credit are often useful for seasonal businesses, uneven customer payments, short-term inventory purchases, or emergency cash-flow gaps.

Best for: flexible working capital and short-term needs.

Not ideal for: long-term projects that require predictable fixed payments.

6.6 Equipment Financing

Equipment financing is used to buy business equipment such as vehicles, machinery, computers, kitchen equipment, medical equipment, tools, or manufacturing assets. The equipment often serves as collateral, which may make approval easier than an unsecured loan. The key is to make sure the equipment will generate or protect enough cash flow to justify the payment.

Best for: assets that are necessary, durable, and revenue-producing.

Not ideal for: equipment that becomes obsolete quickly or does not improve revenue or efficiency.

6.7 Invoice Financing and Invoice Factoring

Invoice financing helps businesses access cash tied up in unpaid customer invoices. It is most common for business-to-business companies that invoice other businesses or government clients. With invoice financing, the invoice acts as support for the advance. With factoring, the finance company may purchase the invoice and collect from the customer.

Best for: businesses with reliable customers but slow payment cycles.

Not ideal for: businesses that sell mainly to consumers or have weak invoice quality.

6.8 Online Business Loans

Online lenders often provide faster applications and quicker funding than traditional banks. They may be more flexible about credit or time in business, but that convenience can come with higher rates, shorter repayment terms, more frequent payments, or larger fees. Online loans can be useful, but they require careful comparison.

Best for: speed, short-term opportunities, or businesses that cannot qualify elsewhere yet.

Not ideal for: long-term borrowing when lower-cost options are available.

6.9 Merchant Cash Advances

A merchant cash advance is not a traditional loan. It is usually an advance repaid through a percentage of future sales or daily/weekly withdrawals. It may be easy to obtain, but the total cost can be difficult to understand and may be high. The FTC has taken action against deceptive practices in the merchant cash advance industry, so business owners should be especially cautious.

Best for: rare situations where a business has strong card sales, a short-term need, and no safer affordable option.

Not ideal for: businesses already struggling with cash flow or relying on repeated advances.

7. Comparison: Best Small Business Loan Options by Situation

| Business Situation | Often Best Loan Type | Why It Fits | What to Check First |

|---|---|---|---|

| Need cash for seasonal inventory | Business line of credit or short-term working capital loan | Flexible access before sales revenue arrives | Can projected sales repay the draw quickly? |

| Buying a delivery van or machinery | Equipment financing or SBA 7(a) | The asset may support the loan and generate income | Useful life, maintenance cost, insurance, down payment |

| Buying owner-occupied commercial property | SBA 504 or commercial real estate loan | Long-term asset needs long-term financing | Occupancy rules, appraisal, down payment, closing costs |

| Startup needs modest funds | SBA microloan, nonprofit lender, community lender | Smaller loan sizes and support may fit early-stage needs | Business plan, owner credit, realistic sales forecast |

| Waiting on unpaid B2B invoices | Invoice financing or factoring | Advances cash already earned but not collected | Customer payment history and fee structure |

| Strong established business wants low cost | Bank loan, credit union loan, SBA 7(a) | Better qualifications may unlock better terms | Collateral, documentation, personal guarantee |

| Need money very quickly | Online loan or line of credit | Speed and lighter application may help | APR, payment frequency, default terms, renewals |

8. How to Choose the Best Small Business Loan

The best way to choose a loan is to start with the business problem, not the product name. A working capital shortage, a long-term equipment purchase, and a real estate expansion all require different repayment structures.

- Define the purpose of the loan in one sentence.

- Calculate the exact amount needed, including taxes, shipping, installation, reserves, and fees.

- Estimate the monthly or weekly payment your business can safely afford.

- Match the loan term to the useful life of what you are financing.

- Compare total cost, not just the advertised rate.

- Check whether the loan requires collateral, a lien, or a personal guarantee.

- Review repayment frequency: monthly payments are usually easier to manage than daily withdrawals.

- Ask whether there are prepayment penalties, maintenance fees, draw fees, late fees, or packaging fees.

- Compare at least two or three offers when possible.

- Read the contract carefully before signing.

9. Costs and Fees to Compare

Small business loan costs can appear in several forms. A low interest rate does not always mean the cheapest loan if the fees are high or the repayment term is too short.

| Cost or Fee | What It Means | Why It Matters |

|---|---|---|

| Interest rate | The cost of borrowing expressed as a rate | Affects payment and total interest |

| APR | Annual percentage rate including certain costs | Helps compare loans with different fees |

| Origination fee | A fee charged to process or fund the loan | Reduces net funds received or increases total cost |

| Guarantee fee | A fee sometimes associated with guaranteed loans | May be paid upfront or financed into the loan |

| Closing costs | Legal, appraisal, title, filing, or documentation costs | Common with real estate and larger loans |

| Draw fee | A charge for using a line of credit | Can raise the cost of frequent borrowing |

| Maintenance fee | A recurring fee for keeping credit available | Matters even if you do not borrow often |

| Prepayment penalty | A charge for paying off early | Can reduce flexibility if cash improves |

| Late fee/default charges | Costs triggered by missed payments | Can quickly worsen a cash-flow problem |

10. Simple Example: Comparing Two Loan Offers

Imagine a bakery needs $40,000 to buy ovens and improve production. Offer A has a lower payment but a longer term. Offer B has a higher payment but a shorter term. The owner should not choose based on the payment alone.

| Feature | Offer A | Offer B |

|---|---|---|

| Loan amount | $40,000 | $40,000 |

| Repayment term | 5 years | 2 years |

| Payment size | Lower | Higher |

| Total interest paid | Usually higher because the term is longer | Usually lower if the rate is similar |

| Cash-flow pressure | Lower each month | Higher each month |

| Best fit | Business needs breathing room | Business has strong predictable cash flow |

The better choice depends on monthly cash flow, not pride or optimism. If Offer B would force the bakery to delay payroll or inventory purchases, Offer A may be safer even if the total interest is higher. If the bakery has stable sales and wants to reduce total interest, Offer B may be better.

11. Business Loan Requirements: What Lenders Usually Review

Requirements vary by lender and loan type, but most lenders look at a common set of risk factors.

- Personal and business credit history

- Time in business

- Monthly or annual revenue

- Profitability and cash flow

- Existing debt obligations

- Business bank statements

- Tax returns and financial statements

- Loan purpose and use of funds

- Collateral or business assets

- Industry risk

- Owner experience

- Legal formation documents and ownership details

A lender is asking one central question: can this business repay the loan on time without creating an unreasonable risk of default? Strong applications answer that question with clear numbers and organized records.

12. Step-by-Step Process to Apply for a Small Business Loan

- Clarify the business need. Decide whether the loan is for working capital, equipment, inventory, real estate, expansion, refinancing, or emergency support.

- Prepare a borrowing amount. Avoid guessing. Build a budget that includes the project cost, fees, reserves, and a cushion for delays.

- Check your repayment ability. Review bank statements, profit margins, debt payments, and seasonal patterns.

- Choose the right loan type. Match short-term needs with short-term financing and long-term assets with longer-term financing.

- Gather documents. Prepare tax returns, financial statements, bank statements, business licenses, ownership records, debt schedules, and a business plan if required.

- Compare lenders. Consider banks, credit unions, SBA lenders, CDFIs, nonprofit lenders, and online lenders.

- Submit applications carefully. Make sure names, tax IDs, revenue figures, and ownership details are consistent across documents.

- Review offers side by side. Compare APR, fees, term, payment frequency, collateral, guarantees, and default language.

- Ask questions before signing. Request clarification in writing if any fee, repayment rule, or guarantee is unclear.

- Use the funds according to plan. Track spending and monitor whether the loan is producing the intended result.

13. Benefits of Small Business Loans

- Access to capital without selling ownership in the business.

- Ability to buy equipment, inventory, or property sooner than saving cash alone would allow.

- Improved cash-flow timing during seasonal or uneven revenue periods.

- Opportunity to accept larger orders or expand into new markets.

- Potential to build business credit through responsible repayment.

- More predictable costs than some forms of equity financing or informal borrowing.

14. Risks and Warnings

- Debt payments can strain cash flow if sales are lower than expected.

- Personal guarantees may put the owner personally responsible for repayment.

- Collateral may be at risk if the business defaults.

- Variable rates can make borrowing more expensive over time.

- Daily or weekly withdrawals can create pressure on operating cash.

- Expensive short-term loans can lead to repeated refinancing or debt stacking.

- Borrowing to cover ongoing losses may delay a necessary business correction.

15. Expert Tips for Choosing Wisely

- Borrow for a measurable business purpose, not vague optimism.

- Use long-term financing for long-term assets and short-term financing for short-term needs.

- Ask for the APR, total repayment amount, and payment schedule in writing.

- Compare the loan payment with conservative revenue projections, not best-case sales.

- Keep at least some cash reserve after funding; do not spend every dollar immediately.

- Be careful with loans that require daily withdrawals from your bank account.

- Do not sign a contract you do not understand. Ask a qualified accountant, attorney, or business advisor to review confusing terms.

- Use free or low-cost counseling resources such as SBA resource partners, SCORE, Small Business Development Centers, or local community business organizations.

16. Real-World Examples

16.1 Example 1: Retail Store Needs Seasonal Inventory

A small clothing shop needs extra inventory before the holiday season. A business line of credit may be better than a long-term loan because the owner can draw funds for inventory, repay after sales come in, and reuse the credit line next season. The risk is overbuying inventory that does not sell, leaving the business with debt and unsold stock.

16.2 Example 2: Contractor Needs a Work Truck

A plumbing contractor needs a reliable truck to serve more customers. Equipment or vehicle financing may fit because the asset directly supports revenue. The owner should compare the loan payment with expected additional monthly profit after insurance, fuel, repairs, and registration.

16.3 Example 3: Startup Needs $20,000 for Supplies and Fixtures

A new home-based bakery wants to buy mixers, packaging, permits, and initial supplies. A microloan or community lender may be more realistic than a large bank loan because the business has limited operating history. The owner should prepare a simple business plan and conservative sales forecast before applying.

16.4 Example 4: Consulting Firm Has Slow-Paying Clients

A consulting firm has completed work but waits 45 to 60 days for invoices to be paid. Invoice financing could provide cash sooner, but the owner should compare the fee against the profit margin on those invoices. If the fee consumes too much of the margin, improving payment terms or requiring deposits may be better.

17. Pros and Cons of Small Business Loans

| Pros | Cons |

|---|---|

| Can fund growth without giving up ownership | Creates fixed repayment obligations |

| Can improve cash flow timing | May require personal guarantee or collateral |

| Can help build business credit | Approval is not guaranteed |

| Can finance productive equipment or property | Fees and interest reduce profit |

| Can help businesses handle seasonal cycles | Wrong loan type can worsen cash-flow stress |

| Multiple options exist for different needs | Loan contracts can be complex |

18. Common Mistakes to Avoid

- Borrowing without a clear repayment plan.

- Choosing the fastest loan without comparing the total cost.

- Using short-term financing for a long-term project.

- Ignoring fees, prepayment penalties, or daily repayment schedules.

- Borrowing more than the business can safely repay.

- Assuming approval is guaranteed because the business is profitable.

- Applying with inconsistent financial records.

- Using loan funds to cover ongoing losses without fixing the underlying problem.

- Signing a personal guarantee without understanding the consequences.

- Taking multiple loans at once without calculating combined debt payments.

19. Quick Action Checklist

- Write down the exact business purpose for the loan.

- Estimate the total amount needed and include fees or setup costs.

- Review your last 6 to 12 months of business bank statements.

- Calculate the payment your business can afford in a normal month, not a perfect month.

- Pick the loan type that matches the use of funds.

- Prepare tax returns, financial statements, bank statements, and ownership documents.

- Check your personal and business credit reports when possible.

- Compare at least two lenders or loan offers.

- Ask for APR, total repayment amount, payment frequency, and fees.

- Read personal guarantee, collateral, default, and prepayment terms before signing.

20. Frequently Asked Questions About the Best Small Business Loans

20.1 What is the best small business loan overall?

The best small business loan depends on your purpose, qualifications, and repayment ability. SBA loans may be strong for many established businesses, bank loans may be cost-effective for strong borrowers, lines of credit may fit working capital, and equipment financing may fit asset purchases.

20.2 What is the easiest small business loan to get?

Online loans, merchant cash advances, and some microloans may be easier to access than bank loans, but easier approval often comes with higher costs or stricter repayment terms. Do not choose a loan only because it is easy.

20.3 Are SBA loans the best option for small businesses?

SBA loans can be excellent for qualified borrowers because they may offer larger amounts, longer terms, and structured underwriting. They are not always best for businesses that need very fast funding or do not meet SBA/lender requirements.

20.4 Can a startup get a small business loan?

Yes, some startups can get financing, especially through microloans, community lenders, equipment financing, personal investment, or SBA-backed options where eligible. Startups should expect lenders to review owner credit, business plan, experience, collateral, and realistic projections.

20.5 What credit score is needed for a small business loan?

There is no single required score for all business loans. Banks and SBA lenders usually prefer stronger credit, while some online or community lenders may consider lower scores. Revenue, cash flow, collateral, and time in business also matter.

20.6 How much can I borrow for a small business loan?

Borrowing limits depend on loan type, lender, revenue, cash flow, collateral, and loan purpose. SBA 7(a) loans can go up to $5 million, SBA 504 loans can generally go up to $5.5 million, and SBA microloans can go up to $50,000, but approval depends on eligibility and underwriting.

20.7 Is a business line of credit better than a term loan?

A line of credit is usually better for flexible short-term needs. A term loan is usually better for a defined purchase or project with a clear cost. The better choice depends on how and when you need the money.

20.8 What is the best loan for buying equipment?

Equipment financing is often a strong fit because the equipment can serve as collateral. SBA 7(a) loans may also work for equipment purchases, especially when the business needs additional working capital with the purchase.

20.9 What is the best loan for working capital?

Business lines of credit, SBA 7(a) loans, short-term working capital loans, and some microloans can all be used for working capital. The best choice depends on how long you need the funds and how predictable your cash flow is.

20.10 Are online business loans safe?

Many online lenders are legitimate, but terms vary widely. Review APR, fees, payment frequency, total repayment amount, renewal rules, and default terms. Be cautious with pressure tactics and unclear pricing.

20.11 Should I use a merchant cash advance?

A merchant cash advance should usually be considered only after comparing safer and more transparent options. It may provide fast cash, but the total cost and repayment pressure can be high.

20.12 Can I get a small business loan with bad credit?

It may be possible, but options are usually more limited and expensive. Consider improving cash flow, reducing debt, adding collateral, applying with a community lender, or starting with a smaller loan.

20.13 Do small business loans require collateral?

Some do and some do not. Equipment loans may use the equipment as collateral, real estate loans use property, and some unsecured loans rely more on credit and cash flow. Many lenders still require a personal guarantee.

20.14 How long does it take to get a small business loan?

Timing varies. Online loans may fund quickly, while bank and SBA loans can take longer because they require more documentation and underwriting. Complex real estate or large equipment loans usually take more time.

20.15 How do I avoid a bad business loan?

Compare total cost, payment frequency, fees, collateral, guarantees, and default terms. Avoid pressure sales, vague pricing, unaffordable payments, and borrowing without a clear plan for repayment.

21. Conclusion: The Best Loan Is the One Your Business Can Repay Comfortably

The best small business loan is not automatically the largest loan, the fastest loan, or the one with the most attractive headline rate. It is the loan that fits the business purpose, has a repayment schedule your cash flow can handle, comes from a trustworthy lender, and improves the business more than it costs.

Start with the problem you are trying to solve. Match the loan to the useful life of the need. Compare total costs, not just interest rates. Read the contract carefully. When in doubt, speak with a qualified accountant, attorney, SBA resource partner, or nonprofit business advisor before signing. Used wisely, small business financing can support growth, stability, and opportunity while keeping risk under control.

21.1 Sources Consulted

- U.S. Small Business Administration, 7(a) loans: https://www.sba.gov/funding-programs/loans/7a-loans

- U.S. Small Business Administration, 504 loans: https://www.sba.gov/funding-programs/loans/504-loans

- U.S. Small Business Administration, Microloans: https://www.sba.gov/funding-programs/loans/microloans

- U.S. Small Business Administration, Loans and Lender Match: https://www.sba.gov/funding-programs/loans

- Federal Reserve Small Business Credit Survey, 2026 Report on Employer Firms: https://www.fedsmallbusiness.org/reports/survey/2026/2026-report-on-employer-firms

- Consumer Financial Protection Bureau, Small business lending rulemaking: https://www.consumerfinance.gov/1071-rule/

- Federal Trade Commission, small business financing and deceptive practices guidance/actions: https://www.ftc.gov/business-guidance/blog/2020/08/protecting-small-businesses-seeking-financing-during-pandemic and https://www.ftc.gov/news-events/news/press-releases/2023/10/ftc-case-leads-permanent-ban-against-merchant-cash-advance-owner-deceiving-small-businesses-seizing

Reader Advice: This article is for general educational and informational purposes only and does not constitute individualized financial, legal, tax, accounting, or investment advice. Loan rates, APRs, fees, eligibility, underwriting standards, credit reporting practices, and applicable laws may vary by lender, loan type, borrower profile, location, and current regulations.

Always review the official loan agreement and disclosures, compare offers based on APR, fees, monthly payments, and total repayment cost, and verify current terms with the lender, loan servicer, StudentAid.gov, the SBA, or other relevant official sources when applicable.

If you need advice for your specific situation, especially involving debt disputes, lawsuits, foreclosure, wage garnishment, bankruptcy, or tax matters, consult a qualified financial professional, nonprofit credit counselor, tax adviser, accountant, consumer attorney, or legal aid organization.