Mortgage Calculator Guide

A mortgage calculator looks simple: enter a home price, down payment, interest rate, and loan term, then get a monthly payment. But for a real buyer, the number on the screen can shape one of the biggest financial decisions of their life. Used well, a mortgage calculator helps you slow down, test different scenarios, and understand what a home may actually cost each month. Used carelessly, it can make a house look affordable when the full cost is much higher.

This guide is for first-time buyers, homeowners considering a refinance, renters comparing buying versus renting, and anyone trying to understand the math behind a home loan. You do not need finance experience. The goal is to help you read calculator results like a thoughtful borrower instead of treating them as a final approval number.

The most important thing to know is that many calculators show only principal and interest by default. Your real monthly housing cost may also include property taxes, homeowners insurance, private mortgage insurance, homeowners association dues, flood insurance, utilities, maintenance, and reserves for repairs. A good mortgage calculator is not just a payment tool. It is a decision-making tool.

1. What Is a Mortgage Calculator?

A mortgage calculator is an online or spreadsheet-based tool that estimates the cost of a home loan. At its simplest, it calculates the monthly principal-and-interest payment based on the loan amount, interest rate, and repayment term. More advanced calculators can also estimate property taxes, homeowners insurance, private mortgage insurance, HOA dues, extra payments, and amortization over time.

A mortgage calculator is not a loan approval, a guarantee of a rate, or a substitute for a written Loan Estimate from a lender. It is an estimate. The result is only as reliable as the numbers you enter.

2. Why Mortgage Calculators Matter Before You Buy a Home

A calculator helps you translate a home price into a monthly obligation. That matters because most buyers do not pay for a home all at once. They commit to years of payments, and the difference between a comfortable payment and a stressful payment can affect savings, retirement contributions, emergency funds, and everyday quality of life.

The Consumer Financial Protection Bureau encourages buyers to estimate taxes and homeowners insurance when deciding how much they want to spend on a home, then subtract those costs from a target monthly payment to understand how much is left for principal and interest. That is exactly the kind of practical planning a good calculator can support.

3. What a Mortgage Calculator Usually Includes

Most mortgage calculators ask for a few core inputs. More complete tools include advanced fields that bring the estimate closer to real life.

| Input | What It Means | Why It Matters |

|---|---|---|

| Home price | The purchase price of the property. | A higher price usually means a higher loan amount, taxes, insurance, and cash needed at closing. |

| Down payment | The cash you pay upfront toward the purchase. | A larger down payment lowers the loan amount and may reduce or eliminate PMI. |

| Loan amount | Home price minus down payment, plus any financed costs if allowed. | This is the balance used to calculate principal and interest. |

| Interest rate | The annual cost of borrowing expressed as a percentage. | Even a small rate difference can change the monthly payment and total interest paid. |

| Loan term | How long you have to repay the loan, often 15 or 30 years. | Longer terms lower monthly payments but usually increase total interest. |

| Property taxes | Local taxes charged by the city, county, or other authority. | Taxes can materially change the total monthly payment and may rise over time. |

| Homeowners insurance | Insurance that protects the home and belongings against covered losses. | Lenders usually require insurance, and premiums vary by property and location. |

| PMI | Private mortgage insurance on many conventional loans with a smaller down payment. | PMI protects the lender, not the borrower, and increases the monthly cost. |

| HOA dues | Monthly or periodic homeowners association charges. | HOA dues can affect affordability even though they are not part of principal and interest. |

| Extra payment | Additional money paid toward principal. | Extra principal can shorten the loan and reduce interest, but it should fit your broader financial plan. |

4. How a Mortgage Calculator Works

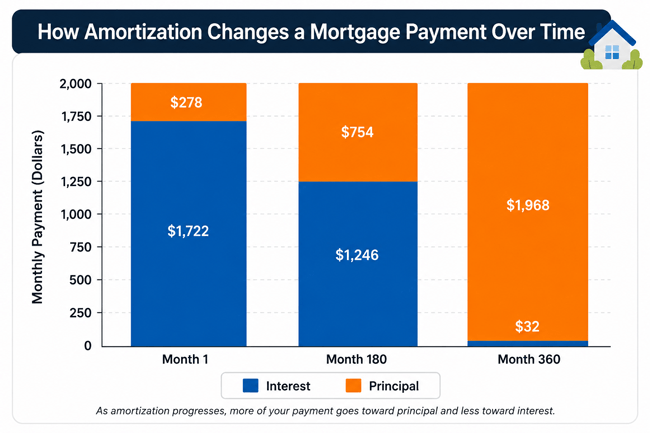

For a fixed-rate mortgage, the calculator uses an amortization formula. Amortization means each scheduled payment is split between interest and principal. At the beginning of the loan, more of the payment goes to interest because the outstanding balance is large. Over time, more goes to principal as the balance falls.

The basic principal-and-interest formula is: Monthly payment = L x [c(1 + c)^n] / [(1 + c)^n - 1]. In plain English, L is the loan amount, c is the monthly interest rate, and n is the total number of monthly payments. A 30-year loan has 360 monthly payments. A 15-year loan has 180.

That formula estimates only principal and interest. To estimate the total housing payment, add monthly property taxes, monthly homeowners insurance, PMI if applicable, HOA dues if applicable, and any other recurring housing charges.

5. Principal and Interest vs. Total Monthly Housing Payment

One of the most common beginner mistakes is confusing the principal-and-interest payment with the full monthly housing cost. The principal-and-interest payment is the loan payment. The total monthly housing payment is the practical household budget number.

| Payment Version | Usually Includes | Best Used For |

|---|---|---|

| Principal and interest only | Loan principal and loan interest. | Comparing loan amounts, interest rates, and loan terms. |

| PITI | Principal, interest, property taxes, and homeowners insurance. | Estimating the core monthly cost of owning a mortgaged home. |

| Full housing payment | PITI plus PMI, HOA dues, flood insurance, special assessments, utilities, maintenance reserves, or other property costs. | Deciding whether the home is realistically affordable. |

6. Real-World Example: Estimating a Mortgage Payment

Imagine a buyer is considering a $400,000 home with an $80,000 down payment. That leaves a $320,000 loan. The buyer is comparing a 30-year fixed mortgage at 6.5% with estimated property taxes, homeowners insurance, PMI, and HOA dues.

Using the standard amortization formula, the estimated principal-and-interest payment is about $2,023 per month. But the buyer should not stop there. If taxes are $420 per month, insurance is $140 per month, PMI is $110 per month, and HOA dues are $75 per month, the more realistic estimated housing payment becomes about $2,768 per month.

This example shows why a calculator is most useful when it includes taxes, insurance, PMI, and HOA dues. A buyer who budgets only for principal and interest may be surprised by the real monthly obligation.

| Item | Estimated Monthly Cost |

|---|---|

| Principal and interest | $2,023 |

| Property taxes | $420 |

| Homeowners insurance | $140 |

| PMI | $110 |

| HOA dues | $75 |

| Estimated full housing payment | $2,768 |

Chart: In a fixed-rate amortizing mortgage, the scheduled payment stays level, but the interest portion generally shrinks while the principal portion grows over time.

7. How to Use a Mortgage Calculator Step by Step

- Start with a realistic home price: Use the price range you are actually considering, not the maximum price a listing site suggests.

- Enter your planned down payment: Use dollars or a percentage. Remember to keep separate cash for closing costs and emergency savings.

- Choose the loan term: Compare 30-year, 20-year, and 15-year options if available. A shorter term usually costs more per month but less in total interest.

- Enter a current rate estimate: Use a rate from a lender quote, mortgage rate survey, or prequalification estimate. Do not rely on an outdated rate.

- Add property taxes: Look at local tax history, listing details, county records, or ask a real estate professional. Taxes can change after purchase.

- Add homeowners insurance: Ask insurers for quotes before assuming a number, especially in areas exposed to storm, wildfire, flood, or earthquake risk.

- Add PMI if your down payment is below 20%: For conventional loans, lenders often require PMI when the down payment is not large enough. PMI rules and cancellation rights depend on the loan and circumstances.

- Include HOA dues and special assessments: A condo or planned community can have dues that materially affect affordability.

- Review the amortization schedule: Look beyond the first monthly payment. Check total interest, balance after five years, and payoff timing.

- Stress-test the result: Test a higher interest rate, higher taxes, higher insurance, or lower income to see whether the payment still fits your budget.

8. Mortgage Calculator vs. Affordability Calculator

These tools overlap, but they answer different questions.

| Tool | Question It Answers | Best For |

|---|---|---|

| Mortgage calculator | What would this loan or home cost each month? | Comparing home prices, down payments, rates, terms, taxes, insurance, and PMI. |

| Affordability calculator | How much house might fit my income and debts? | Setting an initial price range before shopping. |

9. 15-Year vs. 30-Year Mortgage Calculator Comparison

Changing the loan term is one of the fastest ways to see the tradeoff between monthly cash flow and total interest.

| Feature | 15-Year Mortgage | 30-Year Mortgage |

|---|---|---|

| Monthly payment | Usually higher. | Usually lower. |

| Total interest | Usually lower because the loan is paid faster. | Usually higher because interest accrues over a longer period. |

| Equity building | Faster. | Slower in the early years. |

| Budget flexibility | Less flexible because payment is larger. | More flexible because payment is smaller. |

| Best fit | Borrowers with stable income and room in the budget. | Borrowers prioritizing monthly affordability and cash reserves. |

10. Fixed-Rate vs. Adjustable-Rate Mortgage Calculator Inputs

Some calculators let you model adjustable-rate mortgages, but estimates are less certain because future rates can change.

| Feature | Fixed-Rate Mortgage | Adjustable-Rate Mortgage |

|---|---|---|

| Payment predictability | Principal and interest stay the same if the loan is fully amortizing. | Payment may change after the initial fixed period. |

| Calculator reliability | Easier to estimate. | Depends on assumptions about future index values, margins, caps, and adjustment dates. |

| Main risk | You may pay more if you lock in at a high rate and do not refinance. | Future payments may rise. |

11. Benefits of Using a Mortgage Calculator

- It makes home prices easier to understand in monthly terms.

- It helps you compare scenarios before speaking with lenders.

- It shows how down payment size affects the loan amount and possibly PMI.

- It helps reveal the cost of a longer loan term.

- It can show the impact of extra principal payments.

- It encourages better conversations with lenders, agents, and housing counselors.

12. Limitations and Risks of Mortgage Calculators

- Calculator results are estimates, not approvals.

- Advertised rates may not match your actual quote.

- Taxes and insurance can change after you buy.

- Some calculators exclude PMI, HOA dues, flood insurance, or maintenance.

- APR, points, lender fees, and closing costs may not be fully reflected in a simple monthly payment.

- A comfortable payment depends on your full financial life, not just the calculator output.

13. Costs and Fees to Consider Beyond the Calculator

- Closing costs: lender fees, title fees, appraisal fees, recording fees, prepaid taxes, prepaid insurance, and escrow deposits.

- Discount points: optional upfront fees that may lower the interest rate.

- Mortgage insurance: PMI for some conventional loans, or different mortgage insurance structures for government-backed loans.

- Escrow changes: tax and insurance estimates can be adjusted after annual escrow analysis.

- Maintenance and repairs: a calculator usually does not reserve money for roofs, appliances, plumbing, landscaping, or emergency repairs.

- Moving and setup costs: movers, utility deposits, furniture, security systems, and immediate home improvements.

14. Common Mortgage Calculator Mistakes to Avoid

- Using the purchase price instead of the loan amount when the calculator asks for principal.

- Forgetting taxes, insurance, PMI, and HOA dues.

- Assuming the calculator payment equals a lender approval.

- Using an interest rate that is not current or not realistic for your credit profile.

- Ignoring total interest paid over the life of the loan.

- Comparing loans only by monthly payment instead of APR, fees, cash to close, and total cost.

- Forgetting that a lower payment can still be risky if it leaves no emergency cushion.

- Not checking whether extra payments go directly to principal.

15. Expert Tips for Better Mortgage Calculator Results

- Run three scenarios: conservative, realistic, and stretch. The conservative scenario should include higher taxes, higher insurance, and a slightly higher interest rate.

- Use the full housing payment for budgeting, not just principal and interest.

- Compare total interest, not only monthly payment.

- Keep cash reserves after closing. A lower down payment with reserves may be safer than a bigger down payment that drains savings.

- Ask lenders for a Loan Estimate so you can compare real quoted costs, not just calculator assumptions.

- Talk with a HUD-approved housing counselor if you are unsure what payment is safe or if you are already struggling with housing costs.

16. Practical Scenarios: How Buyers Use a Mortgage Calculator

| Scenario | What to Test | Decision Insight |

|---|---|---|

| First-time buyer setting a budget | Try home prices $25,000 apart and include estimated taxes and insurance. | Find a comfortable price range before touring homes. |

| Buyer with limited cash | Compare 5%, 10%, and 20% down payments. | Understand payment differences, PMI impact, and how much cash remains after closing. |

| Borrower choosing loan term | Compare 15-year, 20-year, and 30-year payments. | Balance monthly flexibility against lifetime interest. |

| Homeowner considering refinance | Enter current balance, new rate, new term, and closing costs. | Estimate monthly savings and whether the break-even timeline makes sense. |

| Borrower planning extra payments | Add $100, $250, or $500 extra per month. | Estimate interest savings and payoff acceleration. |

17. Quick Action Checklist

☐ Choose a target monthly housing payment before shopping.

☐ Enter the loan amount, not just the home price.

☐ Use current rate quotes or realistic rate assumptions.

☐ Add property taxes, homeowners insurance, PMI, and HOA dues.

☐ Compare at least three down payment options.

☐ Compare 15-year and 30-year terms if your budget allows.

☐ Review the amortization schedule and total interest.

☐ Stress-test the payment for higher taxes, higher insurance, or income changes.

☐ Keep money available for closing costs, repairs, and emergencies.

☐ Use calculator results as a planning tool, then verify numbers with lender disclosures and professional advice.

18. Frequently Asked Questions About Mortgage Calculators

18.1 What does a mortgage calculator tell you?

A mortgage calculator estimates your monthly mortgage payment based on the loan amount, interest rate, term, and sometimes taxes, insurance, PMI, and HOA dues. It helps you compare options, but it does not guarantee loan approval.

18.2 What is the difference between mortgage payment and total housing payment?

The mortgage payment often means principal and interest. Total housing payment includes principal, interest, taxes, insurance, mortgage insurance, HOA dues, and other ongoing property costs.

18.3 How accurate is a mortgage calculator?

It can be useful for planning, but accuracy depends on the inputs. Taxes, insurance, PMI, closing costs, and your final lender rate can differ from the estimate.

18.4 Should I include taxes and insurance in a mortgage calculator?

Yes. Including taxes and insurance gives a more realistic monthly housing estimate. Many affordability mistakes happen when buyers look only at principal and interest.

18.5 What is PMI in a mortgage calculator?

PMI stands for private mortgage insurance. It is commonly required on conventional loans when the buyer makes a smaller down payment. It protects the lender if the borrower defaults.

18.6 What is escrow in a mortgage payment?

An escrow account is an account a servicer uses to collect and pay certain property-related charges such as taxes and insurance. Escrow can make the monthly payment higher than principal and interest alone.

18.7 Why does a 30-year mortgage have a lower payment than a 15-year mortgage?

A 30-year loan spreads repayment over more months. That lowers the monthly payment but usually increases total interest paid over the life of the loan.

18.8 Can a mortgage calculator show how much house I can afford?

It can help, but an affordability calculator is better for starting with income, debts, down payment, and budget. A mortgage calculator is best for testing the payment on a specific home price or loan amount.

18.9 What interest rate should I enter?

Use a current rate quote from a lender if you have one. If not, use a realistic current estimate and test higher-rate scenarios so you do not plan too tightly.

18.10 Does APR matter in a mortgage calculator?

Yes, but APR is different from the interest rate. The interest rate helps calculate the monthly principal-and-interest payment, while APR reflects broader loan costs. Compare both when reviewing lender offers.

18.11 Can extra payments reduce mortgage interest?

Yes. Extra payments applied to principal can reduce the balance faster and lower total interest. Make sure your lender applies extra payments to principal and check whether your loan has any restrictions.

18.12 Why do calculator results differ from lender estimates?

Different tools use different assumptions for taxes, insurance, PMI, fees, rounding, and start dates. Lender estimates are based on your application, credit, property, and loan terms.

18.13 Is the cheapest monthly payment always the best option?

No. A lower monthly payment may come from a longer term, higher fees, points, or a loan structure that costs more over time. Compare total cost, flexibility, risk, and cash reserves.

18.14 Can I use a mortgage calculator for refinancing?

Yes. Enter your remaining balance, new rate, new term, and closing costs if the calculator allows. Compare monthly savings with the cost and time needed to break even.

18.15 What should I do after using a mortgage calculator?

Use the results to set a budget, compare loan scenarios, gather lender quotes, request Loan Estimates, and decide whether the payment fits your income, debts, savings, and long-term goals.

19. Conclusion: Use the Calculator as a Decision Tool, Not a Permission Slip

A mortgage calculator can help you make a calmer, more informed homebuying decision. It shows how loan amount, down payment, interest rate, term, taxes, insurance, PMI, HOA dues, and extra payments interact. The best use of the tool is not to justify the most expensive home you can possibly buy. It is to find a payment that supports a stable life after closing.

Before you rely on any result, include the full housing payment, stress-test your assumptions, compare multiple scenarios, and leave room for emergencies. Then confirm the numbers with lender disclosures, insurance quotes, tax estimates, and trusted guidance. A calculator cannot make the decision for you, but it can help you ask better questions and avoid expensive surprises.

19.1 Sources Consulted

- Consumer Financial Protection Bureau (CFPB), Mortgages consumer tools and homebuying guidance, including guidance to estimate taxes and homeowners insurance when planning a monthly payment.

- CFPB Regulation X, Section 1024.17, definition and rules related to escrow accounts for taxes, insurance premiums, and related charges.

- Office of the Comptroller of the Currency (OCC), consumer information on mortgages and private mortgage insurance cancellation under the Homeowners Protection Act.

- Federal Reserve Bank of Dallas, payment calculator for mortgages, car loans, and other term loans.

Reader Advice: This article is written for educational purpose only and should not be taken as personalized financial, legal, tax, or mortgage advice. Mortgage rules, lender overlays, interest rates, assistance programs, and eligibility standards can change. Always verify details with licensed mortgage professionals, official program sources, and your lender before making a home-buying decision. Borrowers should compare current lender offers and consult qualified professionals before making a decision.