Fixed vs Adjustable Mortgage

Choosing between a fixed-rate mortgage and an adjustable-rate mortgage is one of the most important decisions a home buyer makes. Both loans can help you buy a home, but they handle interest rates very differently. A fixed-rate mortgage gives you a rate that stays the same for the life of the loan. An adjustable-rate mortgage, often called an ARM, usually starts with a fixed introductory rate and later changes based on the loan terms and market conditions.

This choice matters because your mortgage payment is not just another monthly bill. For many households, it is the largest long-term financial commitment they will ever take on. The loan structure you choose can affect your monthly budget, your ability to handle future rate changes, your refinancing options, and your overall financial stress.

This guide is for first-time buyers, repeat buyers, homeowners thinking about refinancing, and anyone comparing mortgage offers. You may be wondering whether an ARM is too risky, whether a fixed-rate mortgage is worth a higher starting payment, or whether you can save money by choosing an adjustable loan and refinancing later. Those are real concerns, and the right answer depends on your time horizon, income stability, risk tolerance, and backup plan.

The goal is not to declare one mortgage type universally better. The goal is to help you understand how each option works so you can compare loan offers with confidence and avoid surprises after closing.

1. Fixed vs Adjustable Mortgage: Definition

A fixed-rate mortgage is a home loan with an interest rate that does not change during the loan term. Your principal-and-interest payment stays the same, although taxes, homeowners insurance, and mortgage insurance may still change.

An adjustable-rate mortgage is a home loan with an interest rate that can change after an initial fixed period. The adjusted rate is usually based on an index plus a lender margin, subject to rate caps and other loan rules.

2. What Is a Fixed-Rate Mortgage?

A fixed-rate mortgage is designed for stability. When you close on the loan, the interest rate is set. Whether market rates rise or fall later, your note rate remains the same unless you refinance into a new loan.

2.1 How a fixed-rate mortgage works

- You apply for a mortgage and choose a loan term, often 15, 20, or 30 years.

- The lender approves a fixed interest rate based on your credit profile, down payment, loan type, market rates, and other factors.

- Your monthly principal-and-interest payment is calculated using that rate and term.

- You make the same principal-and-interest payment each month until the loan is paid off, sold, or refinanced.

- The payment gradually shifts over time: early payments are interest-heavy, while later payments pay down more principal.

2.2 Why borrowers choose fixed-rate mortgages

- They want predictable payments.

- They plan to keep the home for many years.

- They do not want to worry about future interest-rate increases.

- They have a tight budget and need payment certainty.

- They prefer a simpler mortgage structure.

3. What Is an Adjustable-Rate Mortgage (ARM)?

An adjustable-rate mortgage starts with an interest rate that is fixed for a limited period. After that period ends, the rate can adjust at scheduled intervals. Common examples include 5/1, 5/6, 7/6, and 10/6 ARMs. The first number usually shows the length of the initial fixed period. The second number shows how often the rate adjusts after that period, such as once per year or every six months.

3.1 How an ARM works

- The loan begins with an introductory fixed-rate period, such as five, seven, or ten years.

- During that period, the interest rate and principal-and-interest payment are usually fixed.

- After the introductory period, the rate adjusts according to the loan contract.

- The new rate is commonly calculated using an index plus a fixed margin.

- Rate caps limit how much the interest rate can increase at the first adjustment, each later adjustment, and over the life of the loan.

- Your payment may rise or fall after each adjustment depending on the rate, remaining balance, and loan terms.

3.2 Important ARM terms beginners must know

| Term | Plain-English Meaning | Why It Matters |

|---|---|---|

| Initial rate | The starting rate during the first fixed period. | It may make the loan look cheaper at first, but it is not always the long-term rate. |

| Index | A benchmark rate used to calculate future ARM changes. | If the index rises, your adjusted rate may rise too. |

| Margin | A fixed percentage added to the index. | The margin usually stays with the loan and affects future rates. |

| Adjustment period | How often the rate can change after the fixed period ends. | A 5/6 ARM may adjust every six months after year five. |

| Initial adjustment cap | Limit on how much the rate can change at the first adjustment. | This helps define your first major payment shock risk. |

| Periodic adjustment cap | Limit on each later adjustment. | This controls how fast the payment may continue rising. |

| Lifetime cap | Maximum rate increase over the life of the loan. | This is the worst-case rate ceiling you should test before accepting an ARM. |

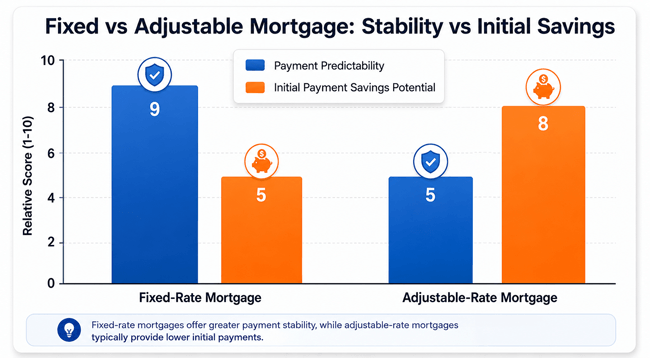

4. Fixed-Rate Mortgage vs ARM: Side-by-Side Comparison

| Feature | Fixed-Rate Mortgage | Adjustable-Rate Mortgage |

|---|---|---|

| Interest rate | Stays the same for the entire loan term. | Fixed at first, then can rise or fall after the introductory period. |

| Payment predictability | High. Principal-and-interest payment is stable. | Lower after the fixed period because payments can change. |

| Starting payment | Often higher than comparable ARM starting payments. | Often lower during the introductory period, though not always. |

| Risk | Less interest-rate risk for the borrower. | More interest-rate risk after adjustments begin. |

| Best fit | Long-term owners, risk-averse buyers, and households needing budget certainty. | Shorter-term owners, buyers expecting income growth, or borrowers with a clear refinance/sale plan. |

| Complexity | Simple and easy to compare. | More complex because you must review index, margin, caps, and adjustment schedule. |

| Main danger | You may pay more initially if rates later fall and you do not refinance. | Payment shock if rates rise or refinancing is unavailable. |

Chart: A simplified comparison of payment predictability and initial savings potential. Actual loan offers vary by lender, market conditions, credit profile, and loan terms.

5. Why the Choice Matters

The difference between a fixed mortgage and an ARM is not just technical. It changes how much uncertainty you carry as a homeowner. With a fixed loan, the lender takes more of the future rate risk. With an ARM, you accept some future rate risk in exchange for possible lower initial costs.

- Monthly cash flow: A lower starting ARM payment can help at the beginning, but future payments can increase.

- Long-term affordability: A fixed loan protects against rate increases if you stay in the home for many years.

- Refinancing risk: Many borrowers choose an ARM assuming they can refinance later, but refinancing depends on rates, credit, income, home value, and lender rules.

- Life changes: Job changes, family growth, medical costs, or relocation plans can make payment stability more valuable.

- Decision stress: A simple fixed-rate loan may be easier to manage for beginners who do not want to track future adjustment dates.

6. Benefits of a Fixed-Rate Mortgage

- Stable principal-and-interest payment for the full loan term.

- Easier budgeting because the rate does not change.

- Protection if market interest rates rise.

- Simple structure that is easier for beginners to understand.

- Good fit for homeowners who expect to stay in the home long term.

- Less need to time the refinance market.

6.1 Potential downsides of a fixed-rate mortgage

- The starting interest rate may be higher than an ARM introductory rate.

- You may pay more in the early years if you sell quickly and never benefit from long-term stability.

- If rates fall, you may need to refinance and pay closing costs to get a lower rate.

7. Benefits of an Adjustable-Rate Mortgage

- Potentially lower initial interest rate and payment.

- Can be useful for buyers who plan to sell before the first adjustment.

- May help borrowers manage short-term cash flow if they fully understand the risk.

- Can be reasonable when the borrower has strong savings, rising income, and a clear backup plan.

- May allow flexibility for people who know the home is temporary.

7.1 Potential downsides of an ARM

- Payments can increase after the introductory period.

- The loan is harder to compare because you must review caps, index, margin, and adjustment frequency.

- The borrower may underestimate worst-case payments.

- Refinancing may not be possible when you want it.

- A lower starting payment can tempt buyers to purchase more home than they can safely afford.

8. Real-World Examples

8.1 Example 1: The long-term homeowner

Maria and Daniel plan to raise their children in the same home for at least 12 years. Their budget is steady but not flexible. A fixed-rate mortgage may fit them better because the predictable payment helps them plan around school costs, repairs, and retirement savings.

8.2 Example 2: The likely mover

Aisha expects to relocate for work within four to five years. She compares a 30-year fixed mortgage with a 7-year ARM. If the ARM has a meaningfully lower starting payment and she is confident she will sell before the first adjustment, the ARM may be worth considering. She still needs to check the worst-case payment in case plans change.

8.3 Example 3: The refinance assumption

Omar chooses a 5/6 ARM because he expects to refinance before year five. But in year five, rates are higher, his income has changed, and his home value has not risen enough. This is the classic ARM risk: refinancing is a strategy, not a guarantee.

8.4 Example 4: The income-growth borrower

Sana is early in a stable career path and expects her income to grow. She has strong emergency savings and compares the maximum ARM payment against her future budget. An ARM may be possible, but only if she can afford the loan even if the rate increases.

9. Step-by-Step Process: How to Choose Between a Fixed Mortgage and an ARM

- Start with your time horizon. Estimate how long you realistically expect to keep the home and the loan.

- Compare actual lender quotes. Do not compare generic averages; compare Loan Estimates for the same loan amount, points, term, and closing-cost assumptions.

- Calculate the monthly payment difference. Identify how much the ARM saves during the initial fixed period, if anything.

- Read the ARM terms. Review the index, margin, first adjustment cap, periodic cap, lifetime cap, and adjustment frequency.

- Stress-test the worst-case payment. Ask whether you could afford the payment if the ARM rose to the first cap or lifetime cap.

- Consider your backup plan. Would you sell, refinance, make extra payments, or absorb the higher payment?

- Factor in closing costs and refinancing costs. Do not assume switching loans later will be free.

- Check your risk tolerance. If payment uncertainty would keep you up at night, the fixed loan may be worth the higher initial payment.

- Ask a housing counselor or trusted financial professional to review the loan terms if you feel unsure.

10. Cost and Fee Considerations

Fixed-rate mortgages and ARMs can both include typical mortgage costs. The exact amounts vary by lender, loan type, location, credit profile, and transaction. Review your Loan Estimate rather than relying on a general rule of thumb.

| Cost or Fee | Applies to Fixed Mortgage? | Applies to ARM? | What to Watch |

|---|---|---|---|

| Interest rate | Yes | Yes | Compare the rate and annual percentage rate (APR). |

| Discount points | Sometimes | Sometimes | Points lower the rate but increase upfront cost. |

| Origination or lender fees | Sometimes | Sometimes | Compare total lender charges, not just the rate. |

| Appraisal and title costs | Usually | Usually | Third-party costs can differ by location and transaction. |

| Mortgage insurance | May apply | May apply | Often depends on down payment, loan type, and equity. |

| Refinance costs | Only if you refinance | Often relevant if you plan to exit the ARM | A refinance plan should include break-even math. |

| Future payment increases | No rate-driven increase on principal and interest | Possible after adjustment | Review caps and worst-case payment. |

11. Risks to Understand Before Choosing

11.1 Fixed-rate mortgage risks

- Opportunity cost: You may start with a higher payment than an ARM.

- Refinance cost risk: If rates fall, getting a lower rate usually requires a new loan with closing costs.

- Overconfidence risk: A fixed payment does not mean the total housing payment can never rise, because taxes, insurance, HOA dues, and maintenance can increase.

11.2 Adjustable-rate mortgage risks

- Payment shock: The payment can rise after the introductory period.

- Market-rate risk: Your rate may adjust upward when rates are higher.

- Refinance risk: You may not qualify to refinance when you need to.

- Home-value risk: Falling or flat home values can limit refinance options.

- Complexity risk: Misunderstanding index, margin, and caps can lead to expensive surprises.

- Behavior risk: A lower initial payment may encourage overborrowing.

12. Common Mistakes to Avoid

| Mistake | Why It Hurts | How to Avoid It |

|---|---|---|

| Choosing only by the starting payment | The ARM may become unaffordable later. | Compare both the starting payment and worst-case payment. |

| Assuming you will refinance before the ARM adjusts | Refinancing depends on rates, credit, income, and home value. | Create a backup plan that does not rely on perfect market timing. |

| Ignoring the margin | The margin affects future adjusted rates. | Find the margin on the Loan Estimate and ask the lender to explain it. |

| Not reading rate caps | Caps define how high the rate can move. | Review initial, periodic, and lifetime caps before signing. |

| Comparing loans with different points or fees | A lower rate may hide higher upfront costs. | Compare APR, total closing costs, and cash to close. |

| Buying too much house | A low introductory payment can mask affordability problems. | Budget based on stable income and emergency savings. |

| Forgetting taxes and insurance | Even fixed-rate mortgage payments can change due to escrow items. | Budget for full housing cost, not just principal and interest. |

13. Expert Tips for Comparing Mortgage Offers

- Ask every lender for the same loan amount, term, down payment, and points structure so comparisons are fair.

- Use the Loan Estimate to compare projected payments, closing costs, and whether the rate can increase after closing.

- For an ARM, ask the lender to show the maximum possible payment at the first adjustment and over the life of the loan.

- Do not treat refinancing as guaranteed. Treat it as a possible exit strategy with costs and qualification risk.

- Keep emergency savings after closing. The safest mortgage is not only the one with the lowest payment; it is the one you can keep paying during stress.

- If you are a first-time buyer, consider speaking with a HUD-approved housing counselor before choosing a complex loan.

14. When a Fixed-Rate Mortgage May Be Better

- You plan to live in the home for many years.

- You want payment stability and simple budgeting.

- Your income is stable but not expected to rise quickly.

- You have limited emergency savings after closing.

- You would be financially stressed by a higher future payment.

- You do not want to monitor rate adjustments or refinance timing.

15. When an Adjustable-Rate Mortgage May Be Better

- You are likely to sell before the first adjustment period ends.

- The ARM offers meaningful initial savings compared with the fixed-rate option.

- You can afford the payment even if the rate adjusts upward.

- You have strong savings and a clear backup plan.

- Your income is likely to increase and your job situation is stable.

- You understand the index, margin, caps, and adjustment schedule.

16. Quick Decision Table

| Your Situation | Usually Lean Toward | Reason |

|---|---|---|

| You expect to keep the home 10+ years | Fixed-rate mortgage | Long-term payment stability usually matters more. |

| You expect to move within 3-7 years | ARM may be worth comparing | Initial savings may matter if you sell before adjustment. |

| Your budget is tight | Fixed-rate mortgage | Future payment increases could be risky. |

| You have strong savings and flexible income | Either, depending on terms | You may be able to manage ARM uncertainty. |

| You dislike financial uncertainty | Fixed-rate mortgage | Peace of mind has real value. |

| You are choosing only because the ARM payment is lower | Pause and stress-test | The lower payment may hide future risk. |

17. Quick Action Checklist

- Get at least three written Loan Estimates from different lenders.

- Compare fixed-rate and ARM offers using the same loan amount and down payment.

- Write down the ARM index, margin, adjustment period, and all caps.

- Calculate the payment at the first possible adjustment cap.

- Calculate whether ARM savings during the fixed period justify the risk.

- Ask what happens if you cannot refinance before the ARM adjusts.

- Keep enough emergency savings after closing.

- Choose the loan that fits your real life, not the one that only looks cheapest today.

18. Frequently Asked Questions

18.1 What is the main difference between a fixed and adjustable mortgage?

A fixed mortgage keeps the same interest rate for the loan term. An adjustable mortgage starts with a fixed period and then can change based on the loan terms. The key difference is payment certainty versus rate-change risk.

18.2 Is a fixed-rate mortgage safer than an ARM?

Usually, yes for borrowers who need stable payments. A fixed-rate mortgage reduces interest-rate risk because the rate does not change. An ARM can still be appropriate, but only if the borrower understands and can handle possible payment increases.

18.3 Why would anyone choose an adjustable-rate mortgage?

Some borrowers choose an ARM because it may offer a lower starting rate or payment. It can make sense for someone who plans to sell before the first adjustment or has strong financial flexibility.

18.4 What does 5/1 ARM mean?

A 5/1 ARM usually has a fixed rate for the first five years and then adjusts once per year after that. Always verify the exact adjustment schedule in the loan documents.

18.5 What does 5/6 ARM mean?

A 5/6 ARM usually has a fixed rate for five years and then adjusts every six months. The “6” refers to six-month adjustment intervals.

18.6 Can my ARM payment go down?

Yes, it can go down if the loan terms allow it and the index decreases. However, borrowers should not choose an ARM only because they hope payments will fall.

18.7 How high can an ARM rate go?

The maximum depends on the loan’s rate caps. Review the initial adjustment cap, periodic cap, and lifetime cap to understand the highest possible rate.

18.8 Can I refinance an ARM into a fixed-rate mortgage?

Often yes, if you qualify and market conditions make sense. But refinancing is not guaranteed because approval depends on credit, income, debt, home value, and available rates.

18.9 Is an ARM good for first-time home buyers?

It can be, but beginners should be cautious. First-time buyers may benefit from the simplicity of a fixed-rate mortgage unless they clearly understand ARM risks and have a strong exit plan.

18.10 Do fixed mortgage payments ever change?

The principal-and-interest portion does not change on a fixed-rate mortgage. But the total monthly payment can change if property taxes, homeowners insurance, HOA dues, or mortgage insurance change.

18.11 Is a lower ARM rate always a better deal?

No. A lower starting rate may not be better if the payment could rise sharply later. Compare savings during the fixed period against worst-case future payments.

18.12 Which mortgage is better if I plan to sell soon?

An ARM may be worth comparing if you are very likely to sell before the first adjustment. Still, plans can change, so you should test whether you could afford the loan after adjustment.

18.13 What should I ask a lender before accepting an ARM?

Ask about the initial fixed period, index, margin, adjustment frequency, initial cap, periodic cap, lifetime cap, maximum payment, and whether there are prepayment penalties.

18.14 What is the biggest ARM mistake?

The biggest mistake is assuming you can refinance before the rate adjusts. Refinancing may be unavailable or unattractive when you need it.

18.15 Should I choose a fixed mortgage or ARM in a high-rate market?

It depends on the spread between fixed and ARM rates, your timeline, and your ability to handle risk. Do not choose an ARM only because fixed rates feel high. Choose it only if the numbers and backup plan work.

19. Conclusion: Which Mortgage Should You Choose?

A fixed-rate mortgage is usually the better fit when you value stability, plan to stay in the home for a long time, or cannot comfortably absorb payment increases. It is simple, predictable, and easier to budget around.

An adjustable-rate mortgage can be useful when the initial savings are meaningful, your time in the home is likely short, and you have a realistic plan for what happens if the rate adjusts. But an ARM should never be chosen casually. The lowest starting payment is not always the safest or cheapest long-term choice.

The best mortgage is the one that lets you buy a home without putting your future budget at risk. Compare written offers, stress-test the payment, understand the loan terms, and choose based on your actual life plan rather than hope or pressure.

19.1 Sources Consulted

This educational article was prepared using general mortgage guidance from authoritative sources, including:

- Consumer Financial Protection Bureau (CFPB): consumer explanations of fixed-rate and adjustable-rate mortgages, Loan Estimate disclosures, and ARM concepts.

- CFPB Consumer Handbook on Adjustable Rate Mortgages: ARM index, margin, adjustment periods, caps, and borrower comparison questions.

- U.S. Department of Housing and Urban Development (HUD): adjustable-rate mortgage overview and borrower considerations.

- Fannie Mae Selling Guide: conventional adjustable-rate mortgage terminology and secondary-market context.

Reader Advice: This article is written for educational purpose only and should not be taken as personalized financial, legal, tax, or mortgage advice. Mortgage rules, lender overlays, interest rates, assistance programs, and eligibility standards can change. Always verify details with licensed mortgage professionals, official program sources, and your lender before making a home-buying decision. Borrowers should compare current lender offers and consult qualified professionals before making a decision.