How to Create a Debt Repayment Plan That Works

Debt can feel confusing because the problem is rarely just one bill. Many people are juggling credit cards, medical balances, personal loans, student loans, buy-now-pay-later payments, overdrafts, collection notices, or past-due utility bills at the same time. A debt repayment plan turns that confusion into a written system: what you owe, what you can afford, which debt gets priority, and what you will do each month until the balances are gone.

This matters because debt decisions affect more than your bank account. A good plan can reduce stress, prevent missed payments, protect your credit where possible, and help you avoid expensive mistakes such as taking a new loan without changing the habits that created the debt. It also helps you see when a do-it-yourself payoff plan is realistic and when you may need help from a nonprofit credit counselor, attorney, lender, or financial coach.

This guide is written for beginners and for anyone who feels behind, overwhelmed, or unsure where to start. You do not need advanced math or perfect credit. You need a clear list, an honest budget, a method you can stick with, and a plan for handling setbacks.

1. What Is a Debt Repayment Plan?

A debt repayment plan is a written strategy for paying down debt over time. It lists each debt, its balance, interest rate, minimum payment, due date, account status, and priority. It also explains how much money you will pay each month and which payoff method you will use.

In plain English, it is your roadmap from “I owe money” to “I know exactly what to pay next.”

1.1 A strong plan usually includes:

- A complete debt inventory

- A realistic monthly payment amount

- A priority order for debts

- A payoff method, such as debt snowball or debt avalanche

- A small emergency buffer so one surprise expense does not break the plan

- A review schedule to track progress and adjust when life changes

2. How a Debt Repayment Plan Works

A repayment plan works by combining budgeting, prioritization, and consistent monthly action. First, you find out exactly what you owe. Next, you compare your income and essential expenses to see how much extra money can go toward debt. Then you choose a strategy and make payments in a specific order.

2.1 Most plans follow this basic formula:

- Pay at least the minimum on every active account to avoid late fees and additional credit damage.

- Put any extra repayment money toward one target debt.

- When the target debt is paid off, roll that payment into the next debt.

- Repeat until all priority debts are paid or until your situation requires a different solution.

3. Why Creating a Debt Repayment Plan Matters

Without a plan, debt repayment often becomes emotional and random. You may pay whichever creditor is loudest, make extra payments without checking interest rates, or use a new credit card after paying down an old one. A written plan helps you make decisions based on numbers instead of panic.

The Federal Trade Commission advises consumers who are struggling with debt to contact creditors directly, ask about lower interest rates, and propose affordable payment plans. It also warns that you do not need to pay a company to talk to creditors on your behalf. The Consumer Financial Protection Bureau explains that nonprofit credit counseling organizations generally advise and educate people on managing money and debts, while many debt settlement, consolidation, or credit repair companies are for-profit businesses that may charge for actions consumers can often do themselves. Sources: FTC Consumer Advice; CFPB Ask CFPB.

4. Debt Repayment Plan vs Debt Management Plan vs Debt Consolidation

| Option | What it means | Best for | Watch out for |

|---|---|---|---|

| Debt repayment plan | A do-it-yourself written plan for paying debts using your budget and chosen strategy. | People who can afford minimum payments and some extra amount each month. | Requires consistency and honest budgeting. |

| Debt management plan | A structured repayment program often arranged through a nonprofit credit counseling agency. | People with unsecured debts who need help negotiating rates or organizing payments. | May include monthly fees and usually requires closing or limiting credit accounts. |

| Debt consolidation | Combining multiple debts into one new loan, balance transfer, or credit line. | People who qualify for a lower interest rate and can avoid taking on new debt. | Can backfire if fees are high or spending habits do not change. |

| Debt settlement | Trying to settle debts for less than owed, often after accounts are delinquent. | Some severely distressed borrowers who cannot repay in full. | Can damage credit, create tax issues, and involve fees or scams. |

5. Debt Snowball vs Debt Avalanche: Which Payoff Method Works Best?

Two of the most searched debt payoff methods are the debt snowball and debt avalanche. Both can work. The best choice is the one you can follow long enough to finish.

| Method | How it works | Main benefit | Possible downside |

|---|---|---|---|

| Debt snowball | Pay minimums on all debts, then put extra money toward the smallest balance first. | Builds motivation through quick wins. | May cost more interest if large high-rate debts are paid later. |

| Debt avalanche | Pay minimums on all debts, then put extra money toward the highest interest rate first. | Usually saves the most interest mathematically. | Progress can feel slow if the first target balance is large. |

| Hybrid method | Start with one small debt for momentum, then switch to highest-interest debts. | Balances motivation and savings. | Requires a little more tracking. |

6. Step-by-Step: How to Create a Debt Repayment Plan That Works

6.1 Make a complete list of every debt

Start with a debt inventory. Do not rely on memory. Check recent statements, lender portals, credit reports, collection letters, medical bills, loan documents, and bank records.

| Debt | Balance | Interest rate | Minimum payment | Due date | Status |

|---|---|---|---|---|---|

| Credit card A | $3,200 | 24.99% | $95 | 5th | Current |

| Personal loan | $5,800 | 13.50% | $210 | 12th | Current |

| Medical bill | $900 | 0% | $50 | 20th | Payment plan |

| Store card | $650 | 29.99% | $35 | 28th | Current |

6.2 Separate urgent debts from non-urgent debts

Not every debt has the same consequences. Some debts can put your housing, transportation, utilities, or legal stability at risk. These should be reviewed before focusing on ordinary credit card payoff speed.

| Priority level | Examples | Why it matters |

|---|---|---|

| High priority | Rent or mortgage arrears, car loan needed for work, utilities, taxes, court-ordered obligations | Nonpayment may lead to eviction, repossession, shutoff, penalties, or legal problems. |

| Medium priority | Active credit cards, personal loans, medical payment plans | Late payments can trigger fees, interest, collection activity, and credit damage. |

| Lower priority | Old collection accounts near legal expiration, disputed debts, very low-interest debts | Still important, but may require verification or a different strategy. |

6.3 Build a realistic monthly budget

A repayment plan fails when it is built on money you do not actually have. List monthly net income, then subtract essentials such as housing, utilities, food, transportation, insurance, minimum debt payments, medication, childcare, and basic savings for irregular expenses.

Your extra debt payment is not your income minus optimism. It is income minus real life.

6.4 Choose your monthly debt repayment amount

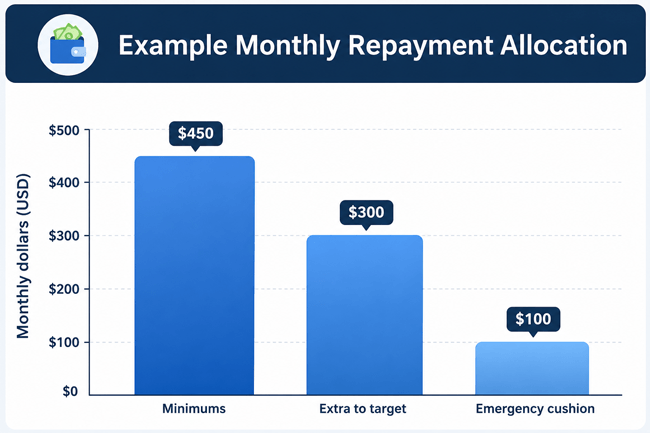

After minimum payments and necessities, decide how much extra you can reliably pay. It is better to commit to a smaller amount you can repeat than a large amount that forces you to use credit again two weeks later.

Example allocation:

6.5 Pick a payoff strategy

Choose debt snowball if motivation is your biggest obstacle. Choose debt avalanche if interest savings are your biggest priority. Choose a hybrid approach if you need an early win but also want to reduce expensive interest.

6.6 Automate minimum payments and manually direct extra payments

Automation helps prevent missed due dates. However, extra payments should be directed carefully. For loans, confirm whether extra payments reduce principal or advance the next due date. For credit cards, make sure you continue paying at least the minimum by the due date even if you made an earlier extra payment.

6.7 Create a small emergency buffer

A small emergency buffer can keep your debt plan from collapsing when a tire blows, a prescription changes, or a utility bill is higher than expected. Even a modest cushion can reduce the chance of adding new debt while trying to pay off old debt.

6.8 Track progress monthly

Once a month, update balances, payments, interest rates, and due dates. This gives you momentum and helps you catch problems early, such as a promotional rate ending or a payment not posting correctly.

7. Real-World Example: Building a Plan From Scratch

Scenario: Maya brings home $3,600 per month. Her essential expenses are $2,650. Her minimum debt payments are $390. That leaves about $560 before irregular expenses. She decides to put $350 extra toward debt and keep $150 for irregular costs and a small emergency buffer.

| Debt | Balance | APR | Minimum | Snowball order | Avalanche order |

|---|---|---|---|---|---|

| Store card | $650 | 29.99% | $35 | 1 | 1 |

| Medical bill | $900 | 0% | $50 | 2 | 4 |

| Credit card | $3,200 | 24.99% | $95 | 3 | 2 |

| Personal loan | $5,800 | 13.50% | $210 | 4 | 3 |

Maya chooses a hybrid strategy. She pays off the store card first because it is both small and expensive. Then she switches to the credit card because its interest rate is high. This gives her an early win and also reduces high-cost debt quickly.

8. Benefits of a Debt Repayment Plan

- Clarity: You know exactly what you owe and what to pay next.

- Lower stress: A written plan reduces guesswork and panic payments.

- Fewer missed payments: Due dates and minimums are built into the system.

- Potential interest savings: Prioritizing high-rate debt can reduce total interest.

- Better decision-making: You can compare payoff options before taking action.

- Progress tracking: Seeing balances fall can improve motivation.

9. Risks and Limitations to Understand

A debt repayment plan is powerful, but it is not magic. It depends on your income, expenses, account status, interest rates, and creditor behavior.

- If you cannot afford minimum payments, a standard DIY plan may not be enough.

- If interest rates are very high, balances may fall slowly unless you negotiate rates or increase payments.

- If accounts are already in collections, you may need debt validation, settlement advice, or legal guidance.

- If you use credit again while repaying debt, progress can disappear quickly.

- If you ignore priority debts, you may create bigger problems even while paying smaller debts.

10. Costs and Fees to Consider

Creating your own debt repayment plan is free. Costs may appear if you use outside services or financial products.

| Possible cost | Where it may appear | What to check |

|---|---|---|

| Late fees | Missed or delayed payments | Ask creditors whether fees can be waived after bringing the account current. |

| Balance transfer fee | Credit card balance transfer | Compare the fee, promotional period, and post-promo APR. |

| Loan origination fee | Debt consolidation loan | Calculate the total cost, not just the monthly payment. |

| Credit counseling DMP fee | Debt management plan | Ask for setup fees, monthly fees, and written terms before enrolling. |

| Settlement fee | Debt settlement company | Be cautious; understand credit, tax, and collection consequences. |

11. Expert Tips for Making Your Plan Work

- Use one debt tracker, not five. A spreadsheet, notebook, or budgeting app is enough if you update it consistently.

- Keep minimum payments on autopay when possible, but review statements every month.

- Call creditors early if you cannot pay. Ask about hardship programs, lower interest rates, waived fees, or revised due dates.

- Avoid closing every paid-off account automatically. Consider credit utilization, fees, temptation, and your overall credit goals.

- Do not use debt consolidation as a substitute for budgeting. A lower payment can help, but only if it reduces total cost or improves stability.

- Build a “no new debt” rule for everyday spending unless borrowing is necessary and planned.

- Celebrate milestones, such as every $500 paid off or every account closed, without using credit to reward yourself.

12. Common Mistakes to Avoid

12.1 Not listing every debt

A plan based on incomplete numbers gives false confidence. Include debts you feel embarrassed about, debts in collections, medical bills, family loans, and small recurring balances.

12.2 Paying extra while missing minimums elsewhere

Extra payments are useful only after required payments are covered. Missing a minimum payment can create late fees, penalty rates, and credit damage.

12.3 Choosing the “best” method but not sticking with it

The avalanche method may save more interest, but the snowball method may be better if quick wins keep you engaged. The best plan is mathematically sound and behaviorally realistic.

12.4 Ignoring interest rates and promotional deadlines

Promotional credit card rates, deferred interest offers, and introductory balance transfer periods can change the payoff order. Put key dates on your calendar.

12.5 Using all available cash for debt

Paying debt aggressively feels productive, but having no cash cushion can push you back into borrowing. Keep a small buffer while you repay.

12.6 Trusting debt relief promises without checking the details

The FTC warns consumers to get details in writing and be cautious of companies that make promises before reviewing your full situation. Reputable credit counseling organizations should explain services, fees, time frames, and consequences clearly.

13. Quick Action Checklist

- Gather statements, credit reports, collection letters, and loan documents.

- List every debt with balance, APR, minimum payment, due date, and status.

- Identify urgent debts that could affect housing, transportation, utilities, taxes, or legal obligations.

- Create a realistic monthly budget using take-home pay and essential expenses.

- Choose a monthly extra payment amount you can repeat.

- Pick snowball, avalanche, or hybrid payoff method.

- Automate minimum payments when possible.

- Direct extra payments to one target debt at a time.

- Build a small emergency buffer.

- Review progress monthly and adjust the plan when income, expenses, or interest rates change.

- Contact creditors or a nonprofit credit counselor if you cannot afford minimum payments.

14. Frequently Asked Questions

14.1 What is the best way to create a debt repayment plan?

The best way is to list every debt, build a realistic budget, pay minimums on all accounts, choose one target debt, and apply extra money consistently until it is paid off.

14.2 Should I use the debt snowball or debt avalanche method?

Use snowball if motivation matters most. Use avalanche if saving interest matters most. A hybrid method can also work.

14.3 How much should I pay toward debt each month?

Pay at least the minimums, then add an extra amount you can afford without using new debt for essentials. The right number is sustainable, not extreme.

14.4 Should I save money or pay off debt first?

Do both if possible. Keep a small emergency buffer while paying debt so unexpected expenses do not force new borrowing.

14.5 Can I negotiate with creditors myself?

Yes. The FTC says consumers can contact credit card companies directly to ask for lower interest rates or affordable payment plans.

14.6 What debts should I pay first?

Pay urgent debts first if nonpayment threatens housing, transportation, utilities, taxes, or legal stability. After that, use snowball, avalanche, or a hybrid strategy.

14.7 Is debt consolidation the same as a debt repayment plan?

No. Debt consolidation uses a new loan or credit product to combine debts. A repayment plan is the broader strategy for paying debts down.

14.8 Will a debt repayment plan hurt my credit score?

A DIY repayment plan does not hurt credit by itself. Missed payments, high balances, new credit applications, and account closures may affect credit.

14.9 What if I cannot afford minimum payments?

Contact creditors early and ask about hardship options. You may also consider nonprofit credit counseling, legal aid, or other debt relief options.

14.10 How often should I review my debt repayment plan?

Review it at least monthly. Update balances, check payment posting, monitor interest rates, and adjust for income or expense changes.

14.11 Should I pay collections before current accounts?

It depends. Current priority debts and active accounts may need attention first. For collection accounts, verify the debt, understand your rights, and consider legal or credit counseling guidance.

14.12 Can a debt repayment plan include medical debt?

Yes. Medical debt can be included in your overall plan, but you may also be able to negotiate a payment plan, financial assistance, or billing correction with the provider.

14.13 What is the fastest way to pay off debt?

The fastest way is to reduce expenses, increase income, avoid new debt, pay minimums on all accounts, and direct every extra dollar toward one target debt.

14.14 When should I get professional help?

Get help if you cannot afford minimum payments, face lawsuits or garnishment, are considering bankruptcy, or feel pressured by a debt relief company you do not understand.

14.15 What tools do I need to track debt?

A simple spreadsheet, notebook, or budgeting app is enough. The best tool is one you will actually update every month.

15. Conclusion: A Debt Repayment Plan Should Fit Real Life

A debt repayment plan that works is not just a list of balances. It is a practical system for deciding what to pay, when to pay it, and how to keep going when life gets messy. Start by listing every debt, protecting essential needs, choosing a payoff method, and making consistent payments. Use the debt snowball for momentum, the debt avalanche for interest savings, or a hybrid strategy if that best fits your situation.

The most important warning is this: do not let shame, pressure, or unrealistic promises drive your decisions. If you can afford minimum payments and some extra amount, a DIY plan may be enough. If you cannot, contact creditors early and consider reputable nonprofit credit counseling or qualified legal help. Progress may start small, but a clear plan turns debt repayment from a stressful guessing game into a series of manageable steps.

Reader Advice: This article is for general educational and informational purposes only and does not constitute individualized financial, legal, tax, accounting, or investment advice. Loan rates, APRs, fees, eligibility, underwriting standards, credit reporting practices, and applicable laws may vary by lender, loan type, borrower profile, location, and current regulations.

Always review the official loan agreement and disclosures, compare offers based on APR, fees, monthly payments, and total repayment cost, and verify current terms with the lender, loan servicer, StudentAid.gov, the SBA, or other relevant official sources when applicable.

If you need advice for your specific situation, especially involving debt disputes, lawsuits, foreclosure, wage garnishment, bankruptcy, or tax matters, consult a qualified financial professional, nonprofit credit counselor, tax adviser, accountant, consumer attorney, or legal aid organization.

Sources Consulted

- Federal Trade Commission, Consumer Advice: How To Get Out of Debt.

- Federal Trade Commission, Consumer Advice: Coping With Debt and Choosing a Credit Counselor.

- Consumer Financial Protection Bureau: Debt Collection resources and Ask CFPB guidance on credit counseling, debt settlement, debt consolidation, and credit repair.

- U.S. Department of Justice, U.S. Trustee Program: Approved credit counseling agencies for bankruptcy-related counseling.