Debt-to-Income Ratio Explained: Why It Matters

Your debt-to-income ratio, often called DTI, is one of the simplest ways to see whether your monthly debt payments are taking up too much of your income. It compares what you owe each month with what you earn before taxes. Lenders use it because a person can have a decent income and still be financially stretched if too much of that income is already promised to credit cards, student loans, car payments, personal loans, child support, or a mortgage.

DTI matters because it affects real decisions: whether you can qualify for a mortgage, refinance a loan, get a personal loan, consolidate debt, or safely take on a new monthly payment. It also matters even when you are not applying for credit. A rising DTI can be an early warning sign that your budget has less room for emergencies, savings, groceries, insurance, rent increases, or income interruptions.

This guide is written for beginners, borrowers preparing for a loan application, homeowners thinking about refinancing, people trying to pay down credit card debt, and anyone who wants a clearer way to measure debt pressure. You will learn what DTI is, how to calculate it, which payments count, what different DTI levels may mean, and how to improve your ratio without falling for risky shortcuts.

1. What Is Debt-to-Income Ratio?

Debt-to-income ratio is a percentage that shows how much of your gross monthly income goes toward required monthly debt payments. The Consumer Financial Protection Bureau defines DTI as all monthly debt payments divided by gross monthly income, and notes that lenders use it to measure your ability to manage payments and repay money you plan to borrow.

Gross monthly income means income before taxes and deductions. Monthly debt payments means required debt obligations, not every bill you pay. That distinction is important because groceries, utilities, gas, health insurance, and subscriptions affect your budget, but they usually are not counted as debt payments in a lender’s DTI calculation.

1.1 Why DTI Is Different From a Budget

A budget measures all income and spending. DTI measures only income compared with required debt payments. A person can have a “good” DTI but still struggle if rent, childcare, medical costs, or other living expenses are high. A person can also have a high DTI but stay current temporarily by cutting savings or relying on credit cards. That is why DTI should be used with a full budget, not as a replacement for one.

2. How to Calculate Debt-to-Income Ratio

The formula is simple:

DTI = (Total monthly debt payments ÷ Gross monthly income) × 100

2.1 Step-by-Step DTI Calculation

- List every recurring monthly debt payment, including credit card minimums, auto loans, personal loans, student loans, mortgage or rent-related housing debt where applicable, alimony or child support if required, and other installment debts.

- Add those monthly debt payments together.

- Find your gross monthly income before taxes and deductions. If your income varies, use a realistic average based on reliable documentation.

- Divide total monthly debt payments by gross monthly income.

- Multiply the result by 100 to convert it to a percentage.

- Recalculate after adding any proposed new loan payment, because lenders often evaluate whether you can afford the new debt, not just your current debts.

2.2 Real-World Example: Calculating DTI Before a Loan Application

Imagine Maya earns $5,000 per month before taxes. Her required monthly debt payments are:

| Debt payment | Monthly amount |

|---|---|

| Car loan | $420 |

| Student loan | $280 |

| Credit card minimum payments | $180 |

| Personal loan | $220 |

| Total monthly debt payments | $1,100 |

Maya’s current DTI is $1,100 ÷ $5,000 × 100 = 22%. If she applies for a mortgage with an estimated full housing payment of $1,650, her new total debt payments would be $2,750. Her projected DTI would become $2,750 ÷ $5,000 × 100 = 55%. That higher projected DTI may make approval harder and may also leave Maya with less room for emergencies and savings.

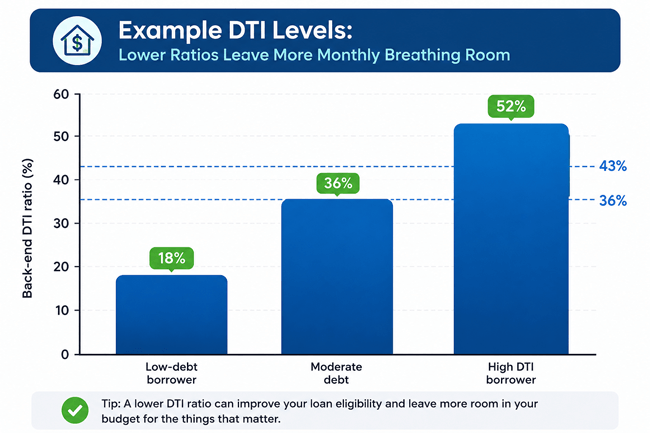

3. Visual Chart: How DTI Levels Compare

Chart uses hypothetical borrower examples for educational purposes. It is not an approval guideline.

4. What Counts as Debt in Your DTI Ratio?

Lenders may calculate DTI differently depending on the loan type, documentation, and underwriting rules. However, the following categories commonly matter.

| Usually included in DTI | Usually not included in DTI |

|---|---|

| Minimum credit card payments | Groceries and household supplies |

| Auto loan or lease payments | Utility bills such as electricity, gas, or water |

| Student loan payments | Streaming subscriptions and memberships |

| Personal loans and debt consolidation loans | Mobile phone bills unless tied to financing or collections |

| Mortgage payment including principal, interest, taxes, insurance, and association dues when applicable | Regular savings contributions |

| Alimony, child support, or court-ordered payments when applicable | Discretionary spending such as dining out or entertainment |

Even if a bill is not included in lender DTI, it still matters to your real-life affordability. For example, childcare may not appear in a traditional DTI formula, but it can affect how safely you can take on a new payment.

5. Front-End DTI vs Back-End DTI

| Type | What it measures | Simple example | Why it matters |

|---|---|---|---|

| Front-end DTI | Housing costs compared with gross monthly income | $1,400 housing payment ÷ $5,000 income = 28% | Often used in mortgage affordability because housing is usually the largest fixed expense. |

| Back-end DTI | All monthly debt payments, including housing, compared with gross monthly income | $2,000 total debt payments ÷ $5,000 income = 40% | Shows the broader debt burden and is commonly emphasized by lenders. |

For renters applying for non-mortgage credit, lenders may focus more on total recurring debts and verified income. For mortgage borrowers, lenders often evaluate a proposed housing payment along with existing debts.

6. What Is a Good Debt-to-Income Ratio?

There is no single DTI number that guarantees approval because lenders also consider credit history, payment history, down payment, savings, loan type, interest rate, employment stability, and the accuracy of your documentation. Still, DTI ranges can help you interpret your situation.

| DTI range | What it may suggest | Practical next step |

|---|---|---|

| Under 20% | Debt payments may be very manageable relative to income. | Keep borrowing cautious and prioritize savings, emergency funds, and retirement contributions. |

| 20% to 35% | Often a manageable range for many borrowers, depending on living costs. | Review whether a new payment would still leave enough room for essentials and savings. |

| 36% to 43% | May be acceptable for some lenders or loan types, but budget flexibility may be tighter. | Avoid adding debt until you test the payment against your full budget. |

| 44% to 50% | May require stronger credit, reserves, compensating factors, or a specific loan program. | Pay down debt, increase income, or consider a smaller loan amount. |

| Above 50% | Can signal serious affordability pressure and may limit borrowing options. | Pause new borrowing if possible and build a debt reduction plan. |

Fannie Mae guidance indicates that a recalculated DTI above 45% for a manually underwritten loan or 50% for a Desktop Underwriter loan casefile is not eligible for delivery to Fannie Mae. FHA-related guidance commonly references 31% front-end and 43% back-end ratios, with exceptions based on compensating factors. VA materials often discuss 41% as a key benchmark, while also considering residual income. These are not universal rules for every borrower or lender.

7. Why Debt-to-Income Ratio Matters

7.1 It Helps Lenders Evaluate Ability to Repay

DTI gives lenders a quick way to compare your required monthly debt payments with your income. A lower ratio suggests more room for a new payment; a higher ratio may suggest a higher risk of missed payments if income drops or expenses rise.

7.2 It Can Affect Loan Approval and Loan Amount

A high DTI can reduce the loan amount you qualify for or result in a denial, even if you have made payments on time. Lenders want to know not only whether you have paid past debts, but whether you can handle the next payment.

7.3 It Can Influence Interest Rates and Terms

DTI is one part of a broader risk profile. A borrower with lower debt pressure, strong credit, and stable income may have more loan options than a borrower whose income is already heavily committed to existing debts.

7.4 It Reveals Budget Stress Before It Becomes a Crisis

A rising DTI can show that debt payments are crowding out savings, insurance, repairs, medical costs, and emergency funds. This gives you time to adjust before missed payments or collections happen.

7.5 It Helps Compare Financial Decisions

DTI can help you decide whether to buy a car, accept a larger mortgage, refinance debt, consolidate balances, or delay borrowing until your finances are stronger.

8. Benefits and Limitations of Using DTI

| Pros of tracking DTI | Limitations and risks |

|---|---|

| Easy to calculate with basic income and debt numbers. | Does not include all living expenses, such as groceries, utilities, childcare, or medical costs. |

| Helps you estimate borrowing readiness before applying. | Lender calculations may differ from your personal calculation. |

| Shows whether debt payments are becoming too large relative to income. | Gross income can make affordability look better than take-home pay actually feels. |

| Useful for comparing debt payoff strategies. | Does not measure credit score, savings, job security, or emergency readiness. |

| Can help prevent overborrowing. | A “passing” DTI does not automatically mean a payment is wise. |

9. Does DTI Affect Your Credit Score?

Your debt-to-income ratio does not directly affect your credit score because income is not part of credit scoring models. Experian explains that DTI has no direct impact on credit scores, although debt balances and payment behavior can affect credit reports and scores. This means you can have a high DTI and a strong credit score, or a low DTI and a weak credit score, depending on payment history, credit utilization, account age, and other credit factors.

However, DTI can still affect your ability to borrow. Lenders may review income, debt payments, credit reports, bank statements, and other documents together. So while DTI is not a credit score factor, it is still a lending and affordability factor.

10. How to Lower Your Debt-to-Income Ratio

There are only two mathematical ways to lower DTI: reduce monthly debt payments or increase gross monthly income. The best approach depends on your situation.

| Strategy | How it lowers DTI | Best for | Important caution |

|---|---|---|---|

| Pay off small debts | Removes monthly minimum payments from the calculation. | Borrowers with small balances and multiple monthly payments. | Do not drain your emergency fund completely. |

| Pay down high-payment loans | Reduces or eliminates large recurring obligations. | People with auto, personal, or installment loans. | Some loans may not lower the monthly payment unless refinanced or paid off. |

| Increase income | Raises the denominator in the DTI formula. | People who can document a raise, second job, overtime, or stable freelance income. | Lenders may require proof and may average variable income. |

| Refinance or consolidate debt | May reduce monthly payments by lowering interest or extending repayment. | Borrowers with high-interest debt and strong discipline. | Extending repayment can increase total interest cost. |

| Avoid new debt | Prevents DTI from rising before a major application. | Mortgage, auto loan, or refinance applicants. | Even small new payments can affect approval. |

| Choose a smaller loan amount | Keeps the proposed new payment lower. | Homebuyers, car buyers, and personal loan applicants. | Lower payment should still fit your real budget, not just lender limits. |

10.1 Step-by-Step Plan to Improve Your DTI

- Calculate your current back-end DTI using required monthly debt payments and gross monthly income.

- Calculate your projected DTI with any new loan payment you are considering.

- Identify payments that can be eliminated fastest, especially small debts with monthly minimums.

- Stop taking on new debt while preparing for a loan application.

- Review whether consolidation or refinancing would reduce monthly payments without creating a worse long-term cost.

- Increase documented income where realistic, such as stable overtime, a raise, or a second income source.

- Recalculate DTI monthly until the ratio and your real budget both improve.

11. Real-World Scenarios

11.1 Scenario 1: Preparing for a Mortgage

Jordan wants to buy a home but has a car payment, student loan, and credit card minimums. Before applying, Jordan calculates current DTI and then adds the estimated mortgage payment. The projected DTI is too high, so Jordan pays off two small credit cards and postpones buying a more expensive car. The result is a lower monthly debt total and a more realistic home budget.

11.2 Scenario 2: Considering Debt Consolidation

Ava has several credit cards with high minimum payments. A debt consolidation loan could reduce her monthly payment, which may lower DTI. But Ava compares the total repayment cost, fees, interest rate, and loan term. She chooses consolidation only if it reduces pressure without encouraging new credit card spending.

11.3 Scenario 3: High Income, High Debt

Sam earns a strong salary but has a large auto loan, student loans, and personal loan payments. Sam’s income looks good, but DTI shows that much of each month is already committed. Sam uses DTI as a reality check before taking on a new mortgage payment.

12. Costs and Fees Related to DTI Decisions

Calculating DTI is free. The costs appear when you use financial products to change your DTI or borrow with a high DTI. Review these carefully:

- Loan origination fees on personal loans, mortgage loans, or refinances.

- Balance transfer fees if using a credit card promotion to manage debt.

- Closing costs on a mortgage refinance.

- Prepayment penalties on some loans, if applicable.

- Higher total interest if you lower monthly payments by extending the repayment term.

- Late fees or penalty interest if a repayment plan is unrealistic.

The Federal Trade Commission warns that debt settlement programs can be risky and that some debt relief companies may not be able to settle debts as promised. The FTC also notes restrictions on advance fees for certain debt relief services sold by phone. Be especially cautious with any company that promises fast debt elimination or asks for large upfront fees.

13. Common Mistakes to Avoid

13.1 Mistake 1: Using take-home pay instead of gross income

For lender-style DTI, use gross monthly income before taxes. For your personal budget, also test affordability using take-home pay.

13.2 Mistake 2: Forgetting the new payment

A current DTI can look manageable until you add the mortgage, auto loan, or personal loan you plan to take on.

13.3 Mistake 3: Counting only minimum credit card payments

Minimums may be used in DTI, but paying only minimums can keep you in debt longer and cost more interest.

13.4 Mistake 4: Ignoring non-debt expenses

Utilities, childcare, groceries, medical costs, and insurance may not count in DTI, but they still affect whether a payment is safe.

13.5 Mistake 5: Taking on new debt before applying

A new credit card, furniture financing, or auto loan can raise DTI and weaken a mortgage or refinance application.

13.6 Mistake 6: Assuming one lender’s limit applies everywhere

DTI rules vary by loan product, lender, underwriting system, compensating factors, and documentation.

13.7 Mistake 7: Lowering payments at any cost

A lower monthly payment can help DTI, but extending a loan may increase total interest. Always compare total cost, not just the monthly bill.

14. Expert Tips for Managing DTI Wisely

- Calculate DTI before you shop for a home, car, or personal loan, not after you find something you want.

- Use projected DTI with the new payment included when deciding what you can afford.

- Keep an emergency fund separate from debt payoff money so one surprise bill does not push you back into borrowing.

- Before applying for a mortgage, avoid new financing for cars, furniture, appliances, or large purchases.

- If your DTI is high, ask whether the problem is too much debt, too little income, or both.

- Compare DTI with your savings rate. A low DTI is stronger when you are also saving consistently.

- Use nonprofit credit counseling if debt payments are becoming unmanageable. Be cautious with for-profit debt relief promises.

15. Quick Action Checklist

- Write down your gross monthly income.

- List every required monthly debt payment.

- Calculate current DTI using the formula.

- Add any proposed new payment and calculate projected DTI.

- Review whether your take-home pay can still cover essentials, savings, and emergencies.

- Pay off or reduce debts that create the largest monthly payment relief.

- Avoid new debt before major loan applications.

- Check your credit reports for debts or payments that may be inaccurate.

- Compare loan offers by total cost, not only monthly payment.

- Recalculate DTI every month during your debt payoff plan.

16. Frequently Asked Questions About Debt-to-Income Ratio

16.1 What is debt-to-income ratio in simple terms?

Debt-to-income ratio is the share of your monthly income that goes toward debt payments. If you earn $4,000 per month and pay $1,200 toward debts, your DTI is 30%.

16.2 How do I calculate my DTI ratio?

Add your monthly debt payments, divide by gross monthly income, and multiply by 100. The formula is: monthly debt payments ÷ gross monthly income × 100.

16.3 What is a good debt-to-income ratio?

A lower DTI is generally better. Many borrowers aim to stay under the mid-30% range when possible, but acceptable ratios vary by loan type, lender, and overall financial profile.

16.4 Is rent included in debt-to-income ratio?

For many non-mortgage calculations, rent may be considered in affordability but is not always treated as debt. For mortgage underwriting, the proposed housing payment is central to the calculation.

16.5 Are utilities included in DTI?

Utilities are usually not included in traditional lender DTI calculations, but they should still be included in your personal budget.

16.6 Do credit card balances count in DTI?

Lenders commonly use required minimum monthly credit card payments, not the full balance, when calculating DTI. However, high balances can still hurt affordability and credit utilization.

16.7 Does DTI affect my credit score?

No. DTI does not directly affect credit scores because income is not used in credit scoring models. Debt balances and payment history can affect credit scores.

16.8 Can I get a loan with a high DTI?

Possibly, depending on the loan type, lender, credit profile, savings, income stability, collateral, and compensating factors. A high DTI can make approval harder and may limit your options.

16.9 How can I lower DTI quickly?

The fastest ways are to pay off debts with monthly payments, reduce required payments through careful refinancing or consolidation, increase documented income, or choose a smaller new loan.

16.10 Is front-end or back-end DTI more important?

Back-end DTI is often more comprehensive because it includes all monthly debt payments. Front-end DTI is especially relevant for mortgage affordability because it focuses on housing costs.

16.11 Should I include my spouse’s income?

Only include income that will be used and documented for the application or household plan. If a spouse is not on a loan, lender treatment may vary by loan type and state rules.

16.12 Does student loan debt count in DTI?

Yes, student loan payments commonly count. If payments are deferred or income-driven, lenders may apply specific rules to estimate the monthly obligation.

16.13 Can debt consolidation improve DTI?

It can if it lowers required monthly payments. But it may increase total interest if the repayment term is longer, and it can backfire if you run up new balances.

16.14 How often should I calculate DTI?

Calculate it before applying for credit, after any major income or debt change, and monthly while paying down debt.

16.15 Is DTI the same as credit utilization?

No. DTI compares monthly debt payments with income. Credit utilization compares credit card balances with credit limits. Utilization affects credit scores more directly; DTI affects affordability and lending decisions.

17. Conclusion: Use DTI as a Borrowing and Budget Reality Check

Debt-to-income ratio is not complicated, but it is powerful. It helps you understand how much of your income is already committed to debt and whether a new payment could create pressure. Lenders use DTI because it gives them a practical way to evaluate ability to repay, but you should use it for your own protection too.

The best practice is to calculate both current and projected DTI, compare the result with your real take-home budget, avoid unnecessary new debt, and improve the ratio before applying for major credit. A lower DTI can make borrowing easier, but more importantly, it can give you more financial breathing room.

The positive takeaway: you do not need to fix everything at once. Start by calculating your ratio, identify the payments that create the most pressure, and take one practical step this month to reduce debt or strengthen income. Small improvements can make future financial decisions safer and more confident.

17.1 Sources Consulted

- Consumer Financial Protection Bureau (CFPB), “What is a debt-to-income ratio?” https://www.consumerfinance.gov/ask-cfpb/what-is-a-debt-to-income-ratio-en-1791/

- CFPB, “Qualified Mortgage Definition under the Truth in Lending Act (Regulation Z): General QM Loan Definition.” https://www.consumerfinance.gov/rules-policy/final-rules/qualified-mortgage-definition-under-truth-lending-act-regulation-z-general-qm-loan-definition/

- Fannie Mae Selling Guide, “Debt-to-Income Ratios.” https://selling-guide.fanniemae.com/sel/b3-6-02/debt-income-ratios

- U.S. Department of Housing and Urban Development (HUD), FHA borrower qualifying ratios guidance. https://www.hud.gov/sites/documents/4155-1_4_secf.pdf

- U.S. Department of Veterans Affairs, “Debt-To-Income Ratio: Does it Make Any Difference to VA Loans?” https://news.va.gov/6371/debt-to-income-ratio-does-it-make-any-difference-to-va-loans/

- Experian, “What Is Debt-to-Income Ratio?” https://www.experian.com/blogs/ask-experian/credit-education/debt-to-income-ratio/

- Federal Trade Commission (FTC), “How To Get Out of Debt.” https://consumer.ftc.gov/articles/how-get-out-debt

- FTC, “Coping With Debt.” https://consumer.ftc.gov/sites/default/files/articles/pdf/pdf-0037-coping-with-debt.pdf

Reader Advice: This article is for general educational and informational purposes only and does not constitute individualized financial, legal, tax, accounting, or investment advice. Loan rates, APRs, fees, eligibility, underwriting standards, credit reporting practices, and applicable laws may vary by lender, loan type, borrower profile, location, and current regulations.

Always review the official loan agreement and disclosures, compare offers based on APR, fees, monthly payments, and total repayment cost, and verify current terms with the lender, loan servicer, StudentAid.gov, the SBA, or other relevant official sources when applicable.

If you need advice for your specific situation, especially involving debt disputes, lawsuits, foreclosure, wage garnishment, bankruptcy, or tax matters, consult a qualified financial professional, nonprofit credit counselor, tax adviser, accountant, consumer attorney, or legal aid organization.