Business Loan Calculator Guide: How to Estimate Monthly Payments

A business loan calculator helps you estimate what a loan may cost before you apply or sign an agreement. For a small business owner, that estimate can be the difference between choosing financing that supports growth and choosing a payment that strains cash flow. The calculator does not approve a loan, set your final rate, or replace a lender quote. Its purpose is to help you understand the likely monthly payment, total interest, repayment schedule, and whether the debt fits your business budget.

This guide is for beginners, startup founders, freelancers, contractors, LLC owners, and established businesses comparing loan options. It explains what each calculator input means, how the math works, which fees can change the real cost, and how to interpret the result in practical business terms.

A borrower should care about more than the monthly payment. A low payment may look affordable because the term is long, but it can also mean paying more interest over time. A short term may reduce total interest, but it can create a payment that is too high for seasonal or uneven revenue. The best calculation considers payment amount, total cost, timing of cash flow, fees, loan purpose, and risk.

1. Quick Definition: What Is a Business Loan Calculator?

A business loan calculator is a financial tool that estimates loan payments and borrowing costs using inputs such as loan amount, interest rate, repayment term, payment frequency, and fees. Most calculators use an amortization formula for installment loans, meaning each payment includes both interest and principal.

The most common result is the estimated monthly payment. Better calculators also show total interest, total repayment amount, APR or estimated APR, and an amortization schedule showing how each payment reduces the balance.

| Calculator Input | What It Means | Why It Matters |

|---|---|---|

| Loan amount | The principal you borrow before fees and interest. | Higher principal usually means a higher payment and more total interest. |

| Interest rate | The annual rate charged by the lender, often shown as APR or simple interest rate. | A small rate difference can significantly change long-term cost. |

| Loan term | How long you have to repay, usually in months or years. | Longer terms lower payments but often increase total interest. |

| Payment frequency | Monthly, weekly, biweekly, daily, or seasonal payments. | More frequent payments affect cash flow and may change effective cost. |

| Fees | Origination fees, packaging fees, guarantee fees, closing costs, or service charges. | Fees can make the real cost higher than the stated interest rate. |

| Repayment type | Amortizing, interest-only, balloon, line of credit, or factor-rate financing. | The wrong calculator can produce misleading results. |

2. How a Business Loan Calculator Works

For a standard term loan, a calculator estimates a fixed payment that fully repays the loan by the end of the term. The payment is based on the loan amount, periodic interest rate, and number of payments. Each payment is split between interest and principal. Early payments usually contain more interest because the outstanding balance is higher. Later payments contain more principal because the balance has declined.

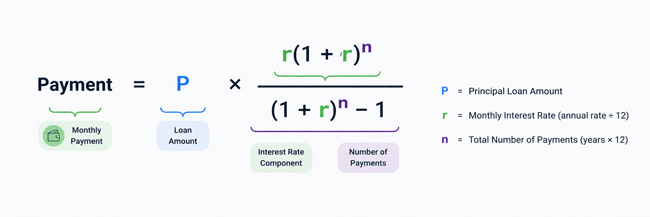

The standard monthly payment formula is:

Monthly payment = P × [r(1 + r)ⁿ] / [(1 + r)ⁿ − 1]

Where P is the loan principal, r is the monthly interest rate, and n is the total number of monthly payments. For example, if the annual interest rate is 12%, the monthly rate is 1% because 12% divided by 12 months equals 1%.

You do not need to memorize the formula to use a calculator. But understanding the logic helps you spot unrealistic results, compare offers, and ask better questions before accepting financing.

3. Why Estimating Monthly Business Loan Payments Matters

A loan payment is not just a number on a screen. It becomes a recurring obligation that competes with payroll, rent, inventory, taxes, supplier bills, marketing, insurance, and emergency reserves. Estimating payments before applying helps you decide whether the loan solves a cash flow problem or creates a new one.

- It helps you compare loan offers with different rates, fees, and repayment terms.

- It shows whether a payment fits your monthly cash flow and profit margins.

- It helps you estimate total interest, not just the headline payment.

- It can reveal whether a longer term is worth the extra cost.

- It helps you avoid borrowing more than the business can reasonably support.

4. Key Inputs You Need Before Using a Business Loan Calculator

A calculator is only as accurate as the information you enter. Before relying on the result, gather the following inputs.

4.1 Loan Amount

Start with the amount you actually need, not the largest amount you may qualify for. Borrowing too little may leave the project underfunded, while borrowing too much can create unnecessary interest expense. If the lender deducts fees from the loan proceeds, calculate whether the net cash received will still cover the business need.

4.2 Interest Rate or APR

The interest rate is the cost of borrowing expressed as a percentage. APR is usually more useful for comparing loans because it may include certain fees in the cost calculation. For small business financing, lenders may describe costs in different ways, including interest rate, APR, factor rate, discount rate, or flat fee. Compare offers using the same cost basis whenever possible.

4.3 Loan Term

The term is the repayment period. A three-year term generally creates a higher monthly payment than a five-year term on the same loan amount and rate, but it usually costs less in total interest. Match the term to the useful life of what you are financing. Equipment that will generate value for five years may fit a longer term better than a short-term inventory purchase.

4.4 Payment Frequency

Many traditional loans use monthly payments. Some online loans, merchant cash advances, and short-term working capital products use weekly, daily, or revenue-based payments. A monthly calculator may understate the cash pressure of daily or weekly withdrawals, especially if sales fluctuate.

4.5 Fees and Closing Costs

Fees can include origination fees, documentation fees, underwriting fees, SBA guarantee fees, servicing fees, prepayment penalties, late fees, appraisal fees, legal fees, or closing costs. Some fees are paid upfront, some are deducted from proceeds, and some are financed into the loan. Each treatment affects cash flow differently.

4.6 Repayment Structure

Do not assume every business financing product amortizes like a traditional loan. A line of credit, invoice financing arrangement, equipment lease, merchant cash advance, or balloon loan may require a different calculation. Use a calculator designed for the specific product.

5. Step-by-Step: How to Estimate Monthly Payments

- Define the purpose of the loan. Decide whether the loan is for equipment, working capital, expansion, inventory, real estate, refinancing, or another business need.

- Estimate the exact amount needed. Include purchase costs, taxes, setup expenses, installation, shipping, working capital cushion, and any lender fees that reduce net proceeds.

- Enter a realistic interest rate or APR. Use a lender quote if available. If not, test several scenarios instead of relying on a single optimistic rate.

- Choose the repayment term. Compare a shorter term and a longer term to see the trade-off between monthly payment and total interest.

- Add fees. Include origination fees, guarantee fees, closing costs, and any financed charges when the calculator allows them.

- Review the monthly payment. Ask whether the business can pay it during slow months, not only during strong months.

- Review total interest and total repayment. A payment may look manageable while the total cost is still too high.

- Create a cash flow stress test. Recalculate using lower revenue, higher rate, delayed sales, or unexpected expenses.

- Compare multiple offers on the same assumptions. A fair comparison uses the same loan amount, term, payment frequency, and fee treatment.

- Confirm the final numbers with the lender. Calculator results are estimates; your loan agreement controls the real obligation.

6. Business Loan Calculator Example: Monthly Payment Estimate

Suppose a business wants to borrow $100,000 for equipment. The lender offers a five-year term at 10% annual interest with monthly payments. Using the standard amortization formula, the estimated monthly payment is about $2,124.70. Over 60 months, the borrower would repay about $127,482, before considering any additional fees. That means estimated total interest is about $27,482.

| Scenario | Loan Amount | APR / Rate | Term | Estimated Monthly Payment | Estimated Total Interest |

|---|---|---|---|---|---|

| Base case | $100,000 | 10% | 60 months | $2,124.70 | $27,482 |

| Shorter term | $100,000 | 10% | 36 months | $3,226.72 | $16,162 |

| Longer term | $100,000 | 10% | 84 months | $1,660.13 | $39,450 |

| Higher rate | $100,000 | 14% | 60 months | $2,326.83 | $39,610 |

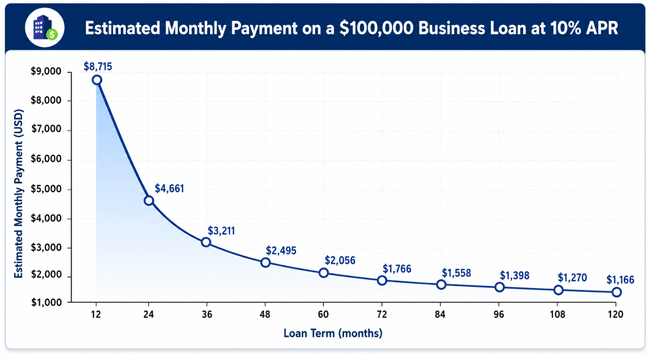

This example shows the central trade-off: the longer term lowers the monthly payment but increases total interest. The shorter term raises the payment but reduces the total cost. The right answer depends on cash flow, profitability, and the expected return from the loan.

Chart: A longer repayment term reduces the monthly payment on the same loan amount and rate, but it usually increases total interest paid.

7. How Fees Change the Real Cost of a Business Loan

Many borrowers compare only the interest rate and monthly payment. That can be misleading because fees can change the actual cost and net proceeds. For example, a $100,000 loan with a 3% origination fee may provide only $97,000 in usable funds if the fee is deducted upfront, while the borrower may still repay based on the full $100,000 principal.

| Fee Type | How It May Appear | How It Affects Your Calculation |

|---|---|---|

| Origination fee | A percentage of the loan amount or a flat charge. | Raises the real cost and may reduce net proceeds. |

| SBA guarantee fee | A fee on some SBA-guaranteed loans, depending on program and size. | May be paid upfront or financed, affecting payment and total cost. |

| Closing costs | Legal, appraisal, filing, title, or documentation charges. | Important for real estate, equipment, and secured loans. |

| Servicing fee | Monthly or periodic administrative fee. | Adds to the recurring cost beyond the payment. |

| Prepayment penalty | A charge for paying off early. | Can reduce the benefit of refinancing or early payoff. |

| Late fee | A charge for missed or delayed payment. | Can increase cost and damage lender relationship. |

Tip: When comparing offers, ask for the total dollar cost of financing, estimated APR, payment schedule, all fees, and the amount of cash you will actually receive after deductions.

8. Monthly Payment vs Total Cost: Which Matters More?

Both matter, but they answer different questions. Monthly payment tells you whether the loan fits your cash flow. Total cost tells you whether the loan makes financial sense overall. A healthy business loan decision considers both.

| Question | Use Monthly Payment | Use Total Cost |

|---|---|---|

| Can I afford this loan each month? | Yes | Partly |

| Which offer is cheaper overall? | Partly | Yes |

| Will the loan create cash flow stress? | Yes | Partly |

| Does a longer term save money? | No, it may only lower the payment | Yes, total cost shows the trade-off |

| Should I refinance? | Compare new payment | Compare interest, fees, penalties, and savings |

9. Business Loan Calculator by Loan Type

Different financing products require different calculations. Using the wrong calculator can make an expensive product look cheaper than it is.

| Loan Type | Best Calculator Type | What to Watch |

|---|---|---|

| Term loan | Amortization calculator | Rate, term, fees, payment frequency, total interest. |

| SBA 7(a) loan | SBA loan calculator or term loan calculator with fees | SBA maximums, lender rate, guarantee fee, maturity limits. |

| Equipment loan | Equipment financing calculator | Down payment, useful life, collateral value, taxes, fees. |

| Business line of credit | Line of credit interest calculator | Interest on amount drawn, draw fees, maintenance fees, variable rates. |

| Invoice financing | Receivables or invoice factoring calculator | Advance rate, discount fee, time outstanding, recourse obligations. |

| Merchant cash advance | Factor rate calculator | Daily/weekly remittance, holdback percentage, effective APR estimate. |

| Commercial real estate loan | Commercial mortgage calculator | Amortization term, balloon payment, appraisal, closing costs. |

9.1 SBA Loan Calculator Considerations

SBA loans are made by lenders and partially guaranteed by the U.S. Small Business Administration. For SBA 7(a) loans, SBA guidance states that interest rates are negotiated between borrower and lender but are subject to SBA maximums pegged to the prime rate or an optional peg rate. The SBA also lists program terms, maximum loan amounts, guarantees, and maturity rules. Because rules, fees, and rates can change, borrowers should verify current SBA details directly with the SBA and the lender before relying on an estimate.

9.2 Line of Credit Calculator Considerations

A business line of credit does not work like a standard installment loan. You usually pay interest only on the amount drawn, not the full credit limit. A $100,000 credit line with a $30,000 balance should be calculated based on the $30,000 actually used, plus fees. If the rate is variable, recalculate whenever rates change.

9.3 Merchant Cash Advance Calculator Considerations

A merchant cash advance is commonly priced with a factor rate rather than an interest rate. For example, a factor rate of 1.30 on $50,000 means the total payback is $65,000. That does not mean the cost is 30% APR. The effective APR can be much higher depending on how quickly the advance is repaid. Use caution when comparing factor-rate products with traditional loans.

10. How to Build a Simple Business Loan Calculator in a Spreadsheet

A spreadsheet can help you test loan scenarios without relying on a website. For a basic monthly payment estimate, use these inputs: loan amount, annual interest rate, and number of months.

| Spreadsheet Field | Example Value | Purpose |

|---|---|---|

| Loan amount | $100,000 | Principal borrowed. |

| Annual interest rate | 10% | Quoted annual rate or APR assumption. |

| Monthly rate | =Annual rate / 12 | Converts annual rate to monthly rate. |

| Number of payments | 60 | Total monthly payments. |

| Monthly payment | =PMT(monthly rate, number of payments, -loan amount) | Estimates fixed monthly payment. |

| Total repayment | =monthly payment x number of payments | Shows total dollars paid. |

| Total interest | =total repayment - loan amount | Shows borrowing cost before fees. |

In Excel or Google Sheets, the PMT function is commonly used for fixed-payment loans. Make sure the payment period and rate period match. If payments are monthly, use a monthly interest rate and the number of months. If payments are weekly, use a weekly rate and number of weeks.

11. Real-World Scenarios: How Business Owners Use Loan Calculators

11.1 Scenario 1: Buying Equipment

A landscaping company needs a new truck and equipment package costing $85,000. The owner compares a 36-month loan and a 60-month loan. The 36-month payment is higher, but the equipment is expected to create enough revenue quickly. The owner chooses the shorter term because the total interest is lower and the equipment should pay for itself within three seasons.

11.2 Scenario 2: Managing Seasonal Cash Flow

A retailer needs inventory before the holiday season. A calculator shows that a short-term loan can be repaid within six months, but weekly payments would be difficult before sales arrive. The owner asks the lender about a repayment structure aligned with expected revenue and keeps a cash reserve rather than borrowing the maximum available amount.

11.3 Scenario 3: Comparing Two Offers

A cafe receives two loan offers. Offer A has a lower interest rate but a large origination fee. Offer B has a slightly higher rate but lower fees and more flexible prepayment terms. By entering fees and total repayment into a calculator, the owner sees that the lower-rate offer is not automatically the cheaper offer.

11.4 Scenario 4: Refinancing Existing Debt

A business has an expensive short-term loan and considers refinancing into a longer-term loan. The calculator shows a lower monthly payment, improving cash flow. But the owner also checks total interest, prepayment penalties, and closing costs to confirm the refinance creates real savings rather than simply extending debt.

12. Pros and Cons of Using a Business Loan Calculator

| Pros | Cons / Limits |

|---|---|

| Helps estimate payments before applying. | Results are estimates, not final loan offers. |

| Makes it easier to compare loan terms. | May not include every lender fee or condition. |

| Shows how rate and term affect cost. | Can be misleading if used for the wrong loan type. |

| Supports cash flow planning. | May not reflect variable rates or irregular payments. |

| Helps prevent overborrowing. | Does not measure approval odds or business risk by itself. |

13. Expert Tips for More Accurate Loan Payment Estimates

- Use conservative assumptions. Test a higher rate, lower revenue, and slower sales than expected.

- Compare the same loan amount and term across lenders. Changing multiple variables at once can hide the true difference.

- Separate the purchase decision from the financing decision. A good asset can become a bad decision if the debt structure is wrong.

- Calculate net proceeds. If fees are deducted upfront, you may receive less cash than the loan amount shown.

- Check whether the rate is fixed or variable. Variable-rate loans can become more expensive if benchmark rates rise.

- Match repayment term to asset life. Do not finance short-lived inventory with long-term debt unless there is a clear cash flow reason.

- Review the amortization schedule. It shows how quickly principal declines and how much interest is paid over time.

- Ask about prepayment rules. Early payoff can save interest only if penalties or fees do not erase the savings.

- Build a repayment reserve. A calculator does not account for emergencies, delayed receivables, or seasonal dips.

14. Common Mistakes to Avoid

| Mistake | Why It Is a Problem | How to Avoid It |

|---|---|---|

| Focusing only on the monthly payment | A low payment may hide a high total cost. | Review total repayment and total interest. |

| Ignoring fees | Fees can raise the true cost and reduce cash received. | Include all known fees in the calculation. |

| Using the wrong calculator | A term loan calculator may not work for an MCA or line of credit. | Match the calculator to the financing product. |

| Assuming approval terms will match estimates | Final terms depend on credit, revenue, collateral, lender policy, and documentation. | Treat calculator results as planning estimates. |

| Forgetting taxes and operating costs | A payment may look affordable before payroll, rent, taxes, and inventory needs. | Run a full cash flow forecast. |

| Not testing slow months | Seasonal businesses can struggle even if average monthly revenue looks strong. | Use the lowest realistic monthly cash flow. |

| Borrowing the maximum available | More debt can reduce flexibility and increase default risk. | Borrow based on a clear business purpose and repayment plan. |

| Confusing factor rate with APR | Factor-rate products can appear simpler but may be costly. | Calculate total payback and effective APR estimate. |

15. How to Decide Whether the Estimated Payment Is Affordable

A calculator can tell you the payment, but affordability depends on your business cash flow. Before taking a loan, compare the payment with expected net operating cash flow, not just sales revenue. Sales can look strong while profit and available cash remain thin.

Ask these questions before accepting a loan:

- Can the business make the payment during its slowest realistic month?

- Will the loan generate enough revenue, savings, or capacity to justify the cost?

- What happens if sales are delayed by 30, 60, or 90 days?

- Does the payment leave room for taxes, payroll, rent, inventory, and emergencies?

- Are there personal guarantees, collateral requirements, or default consequences?

- Would a smaller loan, longer build-up period, or different financing type reduce risk?

16. Business Loan Calculator Formula Example

Here is a simplified manual calculation for a $50,000 loan at 12% annual interest over 36 months. The monthly interest rate is 1% because 12% divided by 12 equals 1%. The number of payments is 36. Using the amortization formula, the estimated monthly payment is about $1,660.72. Total repayment is about $59,786, and total interest is about $9,786 before fees.

| Loan Amount | Annual Rate | Term | Estimated Monthly Payment | Total Repayment | Total Interest |

|---|---|---|---|---|---|

| $50,000 | 12% | 36 months | $1,660.72 | $59,786 | $9,786 |

17. Comparison: Short-Term vs Long-Term Business Loan Payments

| Feature | Short-Term Loan | Long-Term Loan |

|---|---|---|

| Monthly payment | Usually higher | Usually lower |

| Total interest | Often lower if rate is similar | Often higher because debt lasts longer |

| Cash flow impact | More pressure per payment | Less pressure per payment |

| Best for | Inventory, quick projects, bridge needs, short payback opportunities | Equipment, real estate, expansion, larger projects |

| Main risk | Payment may be too high for uneven cash flow | Borrower may pay interest for too long |

18. What a Business Loan Calculator Cannot Tell You

A calculator is a planning tool, not a full underwriting review. It cannot tell you whether you will be approved, whether the lender will require collateral, whether a personal guarantee is acceptable, how the lender will interpret your tax returns, or whether the loan is strategically wise. It also may not capture variable-rate changes, late fees, covenant requirements, or hidden operational risks.

Use the calculator as a first step. Then review lender disclosures, loan agreements, repayment schedule, fees, collateral terms, default provisions, and prepayment rules before signing.

19. Authoritative Trust Signals and Source Notes

When verifying loan rules and disclosures, use primary or authoritative sources. The U.S. Small Business Administration publishes information about SBA loan programs, including 7(a) terms and maximums. The Consumer Financial Protection Bureau provides education and regulatory information on finance charges and credit disclosures, although many business-purpose loans are treated differently from consumer credit. Lender calculators and accounting tools can be useful for estimates, but final numbers should come from the lender’s written offer and loan agreement.

20. Quick Action Checklist

- Write down the exact business purpose for the loan.

- Estimate the minimum amount needed and a realistic cash cushion.

- Collect lender inputs: loan amount, APR or rate, term, fees, payment frequency, and repayment type.

- Run at least three scenarios: base case, higher-rate case, and slower-revenue case.

- Review monthly payment, total interest, total repayment, and net proceeds after fees.

- Compare offers using the same assumptions.

- Check prepayment penalties, late fees, collateral, and personal guarantee requirements.

- Compare the loan payment against slow-month cash flow, not best-month revenue.

- Ask the lender for a written amortization schedule and full fee breakdown.

- Consult a qualified accountant, lender, or business advisor before signing if the loan is large or complex.

21. Frequently Asked Questions About Business Loan Calculators

21.1 What is a business loan calculator?

A business loan calculator is a tool that estimates payments and borrowing costs based on the loan amount, interest rate, term, fees, and repayment structure. It helps business owners plan before applying or accepting a loan.

21.2 How do I calculate a business loan payment?

For a standard installment loan, use the amortization formula or a PMT function in a spreadsheet. Enter the principal, periodic interest rate, and number of payments. The result is the estimated fixed payment.

21.3 What information do I need to use a business loan calculator?

You usually need the loan amount, interest rate or APR, repayment term, payment frequency, and fees. For nontraditional financing, you may also need factor rate, advance rate, draw amount, or revenue holdback percentage.

21.4 Is the monthly payment estimate guaranteed?

No. Calculator results are estimates. Your final payment depends on lender approval, credit profile, revenue, collateral, fees, rate type, underwriting, and the exact loan agreement.

21.5 Does a lower monthly payment always mean a better loan?

No. A lower monthly payment may come from a longer term, which can increase total interest. Compare both monthly affordability and total repayment cost.

21.6 What is an amortization schedule?

An amortization schedule is a table showing each payment, how much goes to interest, how much reduces principal, and the remaining balance after each payment.

21.7 Should I use interest rate or APR in a business loan calculator?

Use APR when possible for comparison because it may reflect certain fees. If the calculator asks for interest rate only, separately calculate fees and total repayment.

21.8 How do fees affect business loan payments?

Fees can increase the real borrowing cost. If fees are financed into the loan, they may raise the payment. If deducted upfront, they reduce the cash you receive while you may still repay the full loan amount.

21.9 Can I use a business loan calculator for an SBA loan?

Yes, but use SBA-specific assumptions where available, including term, lender rate, and applicable fees. Verify current SBA program terms with the SBA and your lender.

21.10 Can I use the same calculator for a line of credit?

Not always. A line of credit usually charges interest on the amount drawn, not the full credit limit. Use a line-of-credit calculator or calculate based on the outstanding balance.

21.11 How do I calculate a merchant cash advance payment?

For an MCA, multiply the advance amount by the factor rate to estimate total payback. Then review the daily or weekly remittance schedule. Do not confuse a factor rate with APR.

21.12 What is the best loan term for a small business loan?

The best term depends on the loan purpose, cash flow, asset life, and total cost. Shorter terms can reduce interest but increase payment pressure; longer terms can improve cash flow but cost more overall.

21.13 How much business loan can I afford?

You can afford a loan only if the payment fits your realistic cash flow after operating expenses, taxes, payroll, and reserves. Test affordability using slow-month revenue, not just average sales.

21.14 Can a calculator show whether I will be approved?

No. Approval depends on lender criteria such as credit, revenue, time in business, profitability, industry risk, collateral, existing debt, and documentation.

21.15 Should I calculate total interest before applying?

Yes. Total interest helps you understand the long-term cost and compare offers. A loan should support profitable growth or solve a clear business need, not simply provide temporary cash at an unsustainable cost.

22. Conclusion: Use the Calculator Before You Borrow

A business loan calculator is one of the simplest ways to make a smarter financing decision. It helps you estimate monthly payments, total interest, total repayment, and the effect of different rates, terms, and fees. The most important lesson is that affordability is not only about qualifying for a loan. It is about choosing a payment your business can handle while still paying employees, suppliers, taxes, and essential operating costs.

Before you borrow, run multiple scenarios, compare offers on equal terms, review fees carefully, and make sure the loan has a clear business purpose. A well-structured loan can support growth, improve efficiency, and strengthen cash flow. A poorly understood loan can create stress even when the monthly payment seemed manageable at first. Use the calculator as your planning tool, then confirm every detail with the lender before signing.

22.1 Sources Consulted

- U.S. Small Business Administration (SBA) - 7(a) Loans: https://www.sba.gov/funding-programs/loans/7a-loans

- U.S. Small Business Administration (SBA) - 7(a) Terms, Conditions, and Eligibility: https://www.sba.gov/partners/lenders/7a-loan-program/terms-conditions-eligibility

- Consumer Financial Protection Bureau (CFPB) - Finance Charge, Regulation Z Section 1026.4: https://www.consumerfinance.gov/rules-policy/regulations/1026/4

- Business Development Bank of Canada (BDC) - Business Loan Calculator: https://www.bdc.ca/en/articles-tools/entrepreneur-toolkit/financial-tools/business-loan-calculator

- Calculator.net - Business Loan Calculator: https://www.calculator.net/business-loan-calculator.html

Reader Advice: This article is for general educational and informational purposes only and does not constitute individualized financial, legal, tax, accounting, or investment advice. Loan rates, APRs, fees, eligibility, underwriting standards, credit reporting practices, and applicable laws may vary by lender, loan type, borrower profile, location, and current regulations.

Always review the official loan agreement and disclosures, compare offers based on APR, fees, monthly payments, and total repayment cost, and verify current terms with the lender, loan servicer, StudentAid.gov, the SBA, or other relevant official sources when applicable.

If you need advice for your specific situation, especially involving debt disputes, lawsuits, foreclosure, wage garnishment, bankruptcy, or tax matters, consult a qualified financial professional, nonprofit credit counselor, tax adviser, accountant, consumer attorney, or legal aid organization.