Best Personal Loans for Debt Consolidation

Debt consolidation means replacing several debts with one new repayment plan. A personal loan is one of the most common ways to do that because it usually offers a fixed interest rate, a fixed monthly payment, and a clear payoff date. Instead of juggling multiple credit card minimum payments, medical bills, or other unsecured balances, you borrow once, pay those debts off, and repay the new loan over time.

This matters because debt stress is rarely just about the amount owed. It is also about confusion, missed due dates, changing interest charges, and the feeling that minimum payments are not moving the balance down. A well-chosen debt consolidation personal loan can make repayment simpler and may reduce total interest. A poorly chosen loan can do the opposite: stretch the debt out, add fees, and make the borrower feel temporary relief while the overall cost increases.

This guide is for people comparing personal loans for debt consolidation, especially beginners who want plain-English explanations before applying. It is also for anyone worried about high-interest credit card balances, inconsistent cash flow, late-payment risk, or whether taking a new loan to pay old debt is a smart decision. The goal is not to push a product. The goal is to help you decide whether a debt consolidation loan is the right tool, how to compare offers, and when another option may be safer.

1. What Is a Personal Loan for Debt Consolidation?

A personal loan for debt consolidation is an installment loan used to pay off multiple existing debts, leaving you with one loan, one monthly payment, and one repayment timeline.

In most cases, the loan is unsecured, meaning you do not pledge your home, car, or other collateral. The lender approves you based on factors such as credit history, income, existing debts, employment stability, and debt-to-income ratio. Some lenders offer direct payment to creditors, which means the loan funds go straight to the credit cards or accounts being consolidated.

2. How Debt Consolidation Personal Loans Work

- List every debt you want to consolidate, including balance, APR, minimum payment, due date, and fees.

- Check whether your credit profile is strong enough to qualify for a lower APR than your current debts.

- Prequalify with multiple lenders when available. Prequalification generally lets you estimate rates without a hard credit inquiry, but confirm the lender’s process.

- Compare APR, origination fees, repayment term, monthly payment, total repayment cost, and lender restrictions.

- Choose the loan only if it improves your repayment plan, not just because the monthly payment looks smaller.

- Use the loan funds to pay off the selected debts immediately.

- Stop adding new balances to the paid-off credit cards while repaying the consolidation loan.

- Automate payments and track progress until the loan is fully repaid.

3. Best Types of Personal Loans for Debt Consolidation

The “best” debt consolidation loan is not the same for every borrower. It is the loan that gives you the lowest realistic total cost, an affordable payment, trustworthy terms, and a payoff plan you can stick with.

| Best for | Loan type to compare | Why it may fit | Watch out for | Best borrower profile |

|---|---|---|---|---|

| Good or excellent credit | Low-APR unsecured personal loan | May reduce credit card interest and provide a fixed payoff date | Origination fees, longer terms that increase total cost | Stable income, strong credit, low debt-to-income ratio |

| Fair credit | Credit union or online lender personal loan | May offer flexible underwriting and smaller loan amounts | APR may be too close to credit card rates to save money | Borrower improving credit but needing structure |

| Large balances | Personal loan with direct creditor payoff | Reduces temptation to use funds elsewhere and simplifies payoff | May not cover all creditor types | Borrower consolidating several credit cards |

| Weak credit but steady income | Secured personal loan or co-borrower loan | Can improve approval odds or lower APR | Collateral risk or co-borrower responsibility | Borrower who understands the risk and has reliable cash flow |

| Short payoff goal | Short-term personal loan | Usually lowers total interest if payment is affordable | Higher monthly payment | Borrower with room in monthly budget |

| Lower payment need | Longer-term personal loan | Can ease monthly cash-flow pressure | May cost more over time | Borrower avoiding missed payments but committed to extra payments later |

4. What Makes a Debt Consolidation Loan “Best”?

- Lower APR than the weighted average APR of the debts being consolidated.

- No unnecessary fees, or fees that are clearly outweighed by interest savings.

- A monthly payment you can afford without relying on new credit card debt.

- A repayment term that supports a clear payoff date instead of simply lowering the payment by stretching the debt too long.

- Fixed rate and fixed payment, so your budget is predictable.

- Transparent lender disclosures, including APR, origination fee, late fee, prepayment policy, and total repayment amount.

- Direct creditor payment if you want help making sure the funds go toward debt payoff.

- A lender or credit union with clear customer service channels and complaint history you are comfortable with.

5. Why Debt Consolidation Matters

Debt consolidation matters because it changes the structure of your debt. Credit card debt is usually revolving: you can pay it down, charge it back up, and carry a balance indefinitely. A personal loan is usually installment debt: you borrow a fixed amount, make scheduled payments, and reach zero by the end of the term if you pay as agreed.

The CFPB explains that debt consolidation loans can convert many debts into one payment and may offer a lower interest rate than existing debts, but it also warns that lower payments can come from longer repayment terms, which may increase overall cost. The FTC also advises people in debt to consider reputable credit counseling and to get fees and promises in writing before signing agreements. These cautions are important because consolidation is a tool, not a cure for overspending or unaffordable debt.

6. Benefits of Personal Loans for Debt Consolidation

- Simpler repayment: one due date and one payment can reduce confusion.

- Potential interest savings: a lower APR can reduce total interest paid.

- Predictable budget: fixed payments make planning easier.

- Clear payoff date: you know when the loan will end if you pay as agreed.

- Possible credit utilization improvement: paying down revolving credit cards may help your utilization ratio, though new credit inquiries and account changes can also affect scores.

- Less temptation than revolving credit if you avoid reusing paid-off cards.

7. Risks and Drawbacks to Consider

- You may pay more overall if you choose a long term just to lower the monthly payment.

- Origination fees can reduce savings or increase the amount you need to borrow.

- A teaser rate or variable rate can make future payments more expensive.

- You can end up with more debt if you consolidate credit cards and then charge them back up.

- Missed payments can lead to late fees, credit damage, collection activity, or default.

- Secured loans can put collateral at risk.

- Some debt relief companies market “consolidation” in ways that are actually settlement or fee-heavy programs.

8. Costs and Fees to Compare Before You Apply

| Cost or fee | What it means | Why it matters | What to ask |

|---|---|---|---|

| APR | The annual cost of borrowing, including interest and certain required fees | Best single number for comparing most loan offers | What is my final APR after fees? |

| Origination fee | A fee some lenders deduct from loan proceeds or add to the loan | Can reduce the cash available to pay creditors | Is the fee deducted upfront? |

| Late fee | Fee for missing the payment deadline | Can increase cost and signal deeper cash-flow issues | Is there a grace period? |

| Prepayment penalty | Fee for paying the loan early | Can reduce flexibility if you want to accelerate payoff | Can I make extra payments without penalty? |

| Returned payment fee | Fee if a bank payment fails | Can trigger extra costs during tight months | What happens if autopay fails? |

| Credit insurance/add-ons | Optional products sometimes offered with loans | May increase total cost and may not be necessary | Is this optional, and what does it cost? |

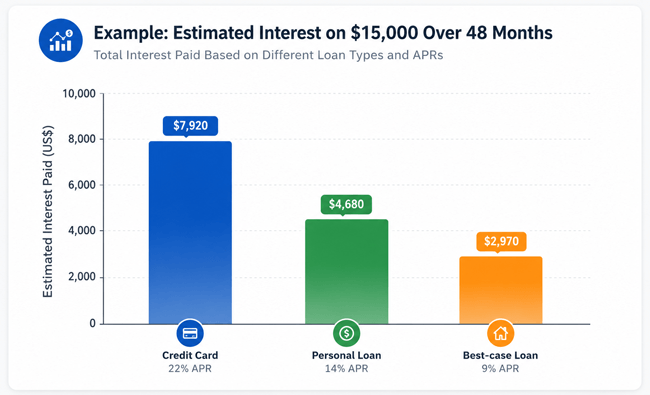

9. Cost Comparison Example: Why APR and Term Matter

The example below is simplified and assumes a $15,000 balance repaid over 48 months with fixed payments. Actual offers vary by lender, credit profile, fees, and repayment term.

| Scenario | APR | Estimated monthly payment | Estimated total interest | Interpretation |

|---|---|---|---|---|

| Credit card 22% APR | 22% | $473 | $7,684 | Lower APR may save money, but only if the borrower avoids new balances and fees do not erase the savings. |

| Personal loan 14% APR | 14% | $410 | $4,675 | Lower APR may save money, but only if the borrower avoids new balances and fees do not erase the savings. |

| Best-case loan 9% APR | 9% | $373 | $2,917 | Lower APR may save money, but only if the borrower avoids new balances and fees do not erase the savings. |

10. Step-by-Step Process to Choose the Best Debt Consolidation Loan

10.1 Step 1: Create a debt inventory

Write down every balance, APR, minimum payment, due date, promotional period, and late fee. Include credit cards, personal loans, medical bills, and other unsecured debts you are considering consolidating.

10.2 Step 2: Calculate your current weighted average APR

Do not compare the new loan only to your highest-rate card. Compare it to the blended cost of all debts being consolidated. A loan may look attractive but still cost more than your current plan if it includes a fee or a longer term.

10.3 Step 3: Decide your real goal

Your goal may be lower interest, fewer due dates, faster payoff, lower monthly payment, or avoiding missed payments. The best loan depends on which goal matters most.

10.4 Step 4: Check your budget before your credit

A loan payment that looks good on paper can fail if your monthly cash flow is already negative. Build a basic budget and include housing, food, utilities, transportation, insurance, minimum savings, and irregular expenses.

10.5 Step 5: Prequalify with several lenders

Compare banks, credit unions, and reputable online lenders. Look for soft-credit prequalification when possible, but read the disclosure because prequalification is not final approval.

10.6 Step 6: Compare APR and total repayment amount

APR helps compare cost, but also look at the dollar amount you will repay over the full term. A lower payment with a longer term can cost more.

10.7 Step 7: Review lender restrictions and funding method

Some lenders pay creditors directly. Some deposit funds into your account. Some restrict the types of debt you can consolidate. Make sure the loan matches your plan.

10.8 Step 8: Read the loan agreement

Confirm rate type, payment due date, fees, prepayment rules, late payment policy, autopay discount terms, and whether optional add-ons are included.

10.9 Step 9: Pay off old debts immediately

Use the proceeds only for the debts listed in your plan. If the lender sends funds to you, pay creditors the same day funds arrive.

10.10 Step 10: Protect the payoff plan

Pause credit card spending, build a small emergency buffer, set up autopay, and track each payment until the loan is gone.

11. Real-World Examples

11.1 Example 1: Good Credit and High-Interest Credit Cards

Maya has three credit cards with high APRs and a steady income. She qualifies for a fixed-rate personal loan with no prepayment penalty and uses direct creditor payoff. Her payment is similar to what she already pays, but more of it goes toward principal. This can be a strong use case because the loan reduces complexity and creates a payoff date.

11.2 Example 2: Fair Credit and a Tempting Lower Payment

Jordan qualifies for a consolidation loan with a lower monthly payment, but the term is much longer and the origination fee is high. The payment feels easier, but the total repayment cost is higher than continuing a disciplined payoff plan. Jordan may be better off negotiating with creditors, using a debt avalanche plan, or speaking with a nonprofit credit counselor before borrowing.

11.3 Example 3: Cash-Flow Trouble and Missed Payments

Ana is already missing payments and cannot afford current minimums. A new loan may not solve the underlying shortfall. A reputable credit counseling organization may help her evaluate budgeting, creditor concessions, or a debt management plan. If the problem is that income is too low for any realistic payment, borrowing more can make the situation worse.

12. Personal Loan vs Other Debt Consolidation Options

| Option | Best use | Main advantage | Main risk | Good fit when |

|---|---|---|---|---|

| Personal loan | Consolidating several unsecured debts | Fixed payment and payoff date | Fees or long term can increase cost | You qualify for a better APR and can stop new card spending |

| Balance transfer card | Short-term credit card payoff | Promotional low or 0% rate | Rate rises after promo period; transfer fees apply | You can repay before the promo ends |

| Debt management plan | Trouble managing unsecured debts | Credit counselor may help organize payments | Requires timely payments and may restrict new credit | You need structured help, not a new loan |

| Home equity loan/HELOC | Large debt and homeowner with equity | Often lower APR than unsecured credit | Home is at risk if you default | You understand collateral risk and repayment is very affordable |

| Debt settlement | Severe hardship and inability to pay full balances | May settle for less than owed | Credit damage, fees, taxes, lawsuits, scam risk | Only after understanding consequences and alternatives |

| Bankruptcy consultation | Debt is unmanageable | Legal pathway for serious debt problems | Long-term credit and legal consequences | You cannot realistically repay debts |

13. Expert Tips for Choosing a Debt Consolidation Personal Loan

- Compare total cost, not only the monthly payment.

- Use the shortest term you can comfortably afford.

- Treat origination fees as real interest savings reducers.

- Avoid loans that require unnecessary add-on products.

- Check whether the lender offers direct creditor payoff.

- Keep old credit cards open only if you can avoid new balances; otherwise, remove them from wallets and online stores.

- Build a small emergency fund so one surprise bill does not restart the credit card cycle.

- Contact creditors early if you are at risk of missing payments.

- Use nonprofit credit counseling before paying a debt relief company.

- Keep copies of loan disclosures, payoff confirmations, and creditor statements.

14. Common Mistakes to Avoid

- Choosing the lowest payment without checking total repayment cost.

- Ignoring origination fees and other charges.

- Consolidating debt without changing the spending pattern that created it.

- Using loan funds for anything other than paying the planned debts.

- Closing all paid-off credit cards immediately without understanding possible credit-score effects.

- Applying with too many lenders that use hard credit inquiries.

- Consolidating federal student loans or secured debts without understanding special protections or collateral risk.

- Confusing debt consolidation with debt settlement.

- Trusting companies that promise guaranteed approval, instant credit repair, or results before reviewing your finances.

- Skipping the written agreement and relying on verbal promises.

15. When a Debt Consolidation Loan Is a Good Idea

- You qualify for a meaningfully lower APR than your existing debts.

- The monthly payment fits your budget without new borrowing.

- You have a plan to stop adding new balances to paid-off cards.

- The total repayment cost is lower or the higher cost is justified by avoiding missed payments and stabilizing cash flow.

- You understand all fees, term length, and consequences of missing payments.

- You prefer a fixed payoff schedule and can commit to it.

16. When a Debt Consolidation Loan May Be a Bad Idea

- Your income does not cover basic expenses and the new payment.

- The new APR is not lower than your current average debt cost.

- The only way the payment is affordable is by extending the term far longer.

- Fees erase most or all savings.

- You are likely to reuse paid-off cards and build new balances.

- You are being pressured by a company that promises unrealistic results.

- You may need legal or credit counseling help because the debt is already unmanageable.

17. Quick Action Checklist

- ☐ List every debt with balance, APR, payment, and due date.

- ☐ Calculate your current total monthly payment and total payoff cost if possible.

- ☐ Check your credit reports for errors before applying.

- ☐ Prequalify with at least three reputable lenders or credit unions when possible.

- ☐ Compare APR, fees, term, payment, and total repayment amount.

- ☐ Reject any loan that only looks good because it stretches repayment too long.

- ☐ Ask whether the lender pays creditors directly.

- ☐ Confirm there is no prepayment penalty if you want flexibility.

- ☐ Create a no-new-card-debt rule before accepting funds.

- ☐ Set up autopay and calendar reminders.

- ☐ Consider nonprofit credit counseling if you cannot afford any realistic loan payment.

18. Frequently Asked Questions

18.1 What is the best personal loan for debt consolidation?

The best personal loan for debt consolidation is the one with the lowest total cost, affordable fixed payment, trustworthy lender terms, and a repayment timeline you can complete. A low APR matters, but fees, term length, and your ability to avoid new debt matter just as much.

18.2 Is debt consolidation the same as debt settlement?

No. Debt consolidation usually means replacing multiple debts with one new loan or payment plan. Debt settlement means trying to pay less than you owe, often after missed payments, and it can damage credit and create collection or tax issues.

18.3 Does a debt consolidation loan hurt your credit?

It can affect your credit in both directions. Applying may create a hard inquiry, and a new account can change your credit profile. Paying down credit cards may help revolving utilization, and on-time loan payments can support your credit over time.

18.4 What credit score do I need for a debt consolidation loan?

Requirements vary by lender. Stronger credit generally improves approval odds and pricing, but some lenders consider fair-credit borrowers, co-borrowers, secured options, income, and debt-to-income ratio.

18.5 Can I consolidate debt with bad credit?

Possibly, but the loan may be expensive. Compare the APR and fees carefully. If the new loan costs as much as or more than your current debt, credit counseling or a hardship plan may be safer.

18.6 Is a lower monthly payment always better?

No. A lower payment can be helpful, but it may come from a longer repayment term. That can increase total interest even if the payment feels easier.

18.7 Should I use a personal loan or a balance transfer card?

A balance transfer card may work if you can repay the balance before the promotional period ends and the transfer fee is reasonable. A personal loan may be better if you need fixed payments, a longer structured payoff period, or want to avoid revolving credit.

18.8 Can I use a personal loan to pay off credit cards?

Yes, many borrowers use personal loans to pay off credit cards. The key is to use the funds for payoff immediately and avoid charging new balances on the cards.

18.9 Are debt consolidation loans secured or unsecured?

Many personal loans for debt consolidation are unsecured. Some lenders also offer secured loans, which may be easier to qualify for but can put collateral at risk if you do not repay.

18.10 What fees should I watch for?

Watch for origination fees, late fees, returned payment fees, prepayment penalties, and optional add-on products. Always compare the APR and total repayment amount.

18.11 Should I close my credit cards after consolidation?

Not automatically. Closing cards can affect credit utilization and credit history. However, if open cards tempt you to overspend, consider removing them from your wallet, lowering limits, or closing selectively after understanding the trade-offs.

18.12 What happens if I miss a consolidation loan payment?

You may face late fees, credit reporting damage, collection activity, or default. Contact the lender early if you are at risk of missing a payment; some lenders offer hardship options.

18.13 Can I pay off a debt consolidation loan early?

Often yes, but check whether the lender charges a prepayment penalty. A loan with no prepayment penalty gives you more flexibility to save interest by paying extra.

18.14 Is a credit union better for debt consolidation?

Credit unions can be a strong option because they may offer competitive rates and member-focused underwriting. Still compare APR, fees, term, and total cost against banks and online lenders.

18.15 When should I talk to a credit counselor?

Talk to a reputable nonprofit credit counselor if you cannot afford current payments, are already missing payments, are unsure whether borrowing more is safe, or need help creating a budget and repayment plan.

19. Conclusion: The Best Loan Is the One That Actually Gets You Out of Debt

The best personal loans for debt consolidation are not simply the loans with the most attractive advertisements or the lowest advertised starting rates. The best loan is the one that lowers your real cost, fits your monthly budget, gives you a clear payoff date, and supports better financial habits.

Debt consolidation can simplify repayment and reduce interest, but it can also hide deeper budget problems if you keep using paid-off credit cards or choose a longer term without understanding the total cost. Compare several offers, read the agreement, avoid pressure, and use trusted consumer resources when you need help. A thoughtful consolidation plan can turn scattered debt into a structured path forward.

Reader Advice: This article is for general educational and informational purposes only and does not constitute individualized financial, legal, tax, accounting, or investment advice. Loan rates, APRs, fees, eligibility, underwriting standards, credit reporting practices, and applicable laws may vary by lender, loan type, borrower profile, location, and current regulations.

Always review the official loan agreement and disclosures, compare offers based on APR, fees, monthly payments, and total repayment cost, and verify current terms with the lender, loan servicer, StudentAid.gov, the SBA, or other relevant official sources when applicable.

If you need advice for your specific situation, especially involving debt disputes, lawsuits, foreclosure, wage garnishment, bankruptcy, or tax matters, consult a qualified financial professional, nonprofit credit counselor, tax adviser, accountant, consumer attorney, or legal aid organization.

Sources Consulted

The guidance in this article is informed by consumer-finance resources from the following organizations. Always review lender disclosures and consider professional advice for your personal situation.

- Consumer Financial Protection Bureau: consolidating credit card debt

- Consumer Financial Protection Bureau: credit counseling

- Consumer Financial Protection Bureau: debt consolidation, settlement, and credit repair differences

- Federal Trade Commission: how to get out of debt

- Federal Reserve: Consumer Credit G.19 interest-rate definitions

- Consumer Financial Protection Bureau: submit a complaint about financial products or services